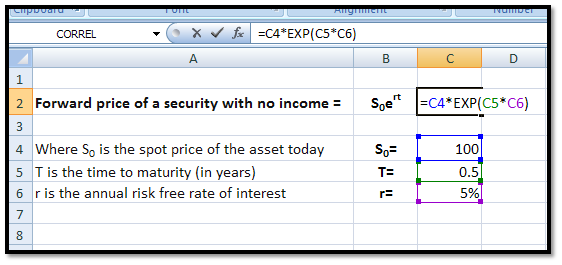

a. Forward Price of a security with no income

Forward Price of a security with no income is given by the formula S0ert.

For example, if S0 , the spot price, of the asset is 100. The time to delivery in the forward contract is 6 months (or 0.5 years) and the annual risk free rate is 5%, then the forward price of the security will be:

100 × e0.05 ×0.5 = 102.53

You may calculate this in EXCEL in the following manner:

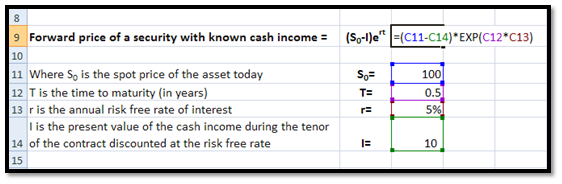

b. Forward Price of a security with known cash income

Forward Price of a security with known cash income is given by the formula (S0-I) ert.

For example, a security with spot price of 100, pays a dividend whose present value as of today (time 0) is 10. The risk free rate and tenor of the forward contract are as mentioned earlier, i.e. 5% and 0.5 years respectively. The forward price will be:

(100-10) × e0.05 ×0.5 = 92.28

You may calculate this in EXCEL in the following manner:

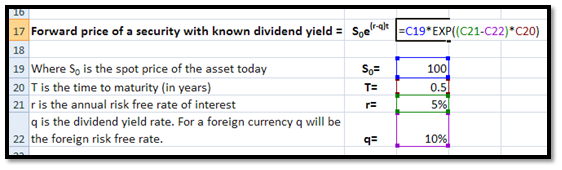

c. Forward Price of a security with known dividend yield

Forward Price of a security with known dividend yield is given by the formula S0e(r-q)t.

For example, a security with spot price of 100, pays a 10% annual dividend. The risk free rate and tenor of the forward contract are as mentioned earlier, i.e. 5% and 0.5 years respectively. The forward price will be:

100 × e(0.05-0.1) ×0.5 = 97.53

You may calculate this in EXCEL in the following manner:

Comments are closed.