Review Option Greeks Primer – Sign up deadline this weekend

Option Greeks Primer will be published by Palgrave Macmillan in Q3 of 2014.

The book is aimed at bridging the gap that exists in Greeks coverage in academic and practitioner literature.

Twenty years ago when I went looking for material on convexity most books on Fixed Income Portfolio management would devote a page to a paragraph. In early 2011 when I started teaching an Executive MBA course on derivative pricing, I had a similar challenge with Option Greeks. The best on offer was a few pages. The worst was a passing mention. Essentially the book came out of the teaching notes from that course and later workshops that would help audiences get comfortable with Greeks.

Please drop me a private message if you are interested in reading/reviewing a copy of the book. I only need your gmail/hotmail/yahoo address since the PDF file is about 18 MB.

At this point I am very interested in feedback on your assessment of:

a) Does the book work?

b) How could the book be used by academic programs as well as training teams in breaking in new interns, analysts and associates at trading desks?

c) How would you improve presentation and the material?

I am about to send the first draft of my manuscript to Palgrave this weekend. If you agree, the book should be in your mailbox sometime this weekend.

It would be great if you could share initial impressions in the next ten days. You will have much more time to write a more detailed review.

The deadline for signups is this weekend (Sunday 11:59 pm)

Here is what the book covers.

The book is organized in five parts.

The first part consists of two chapters (chapter zero and one) that serve as background and refresher of basics and can easily be skipped by the more experienced readers. They cover basic themes, a few relationships and numerical examples to reinforce calculation and usage conventions of Greeks.

The second part begins with a simple Delta hedging simulation for a vanilla call option. The simulation is used to examine the components of hedging P&L. We extend the model to vanilla put options. We use the P&L model to build a better understanding of the behaviour of Delta and two minor Greeks.

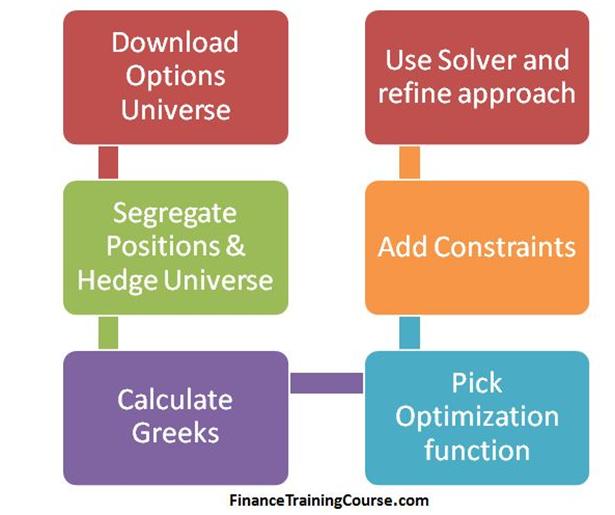

The third part is dedicated to volatility. My personal demons as a student in the field were volatility surfaces and hedging higher order Greeks. Volatility, Vega and Gamma surfaces, therefore, make an extended appearance. So does the topic of hedging higher order Greeks using EXCEL Solver.

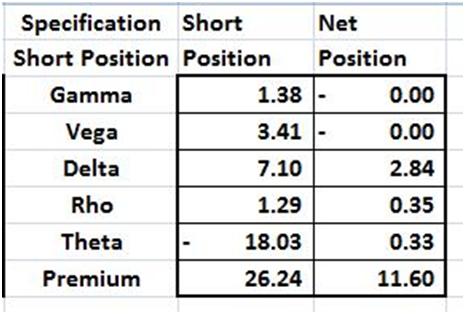

We begin with hedging a single position with deep out of money options and then graduate to a portfolio of short positions and more sophisticated Solver models. Solver is used to illustrate multiple scenarios, objective functions and hedging perspectives for Gamma and Vega neutral hedging models.

The fourth and fifth parts tie up a few loose ends by reviewing two application questions, spending some additional time on Theta and Rho and closing up with related annexures.