The Federal Reserve published revised capital adequacy rules and regulations in July 2013 that follow the Basel III revisions to capital adequacy rules. In particular there are revised minimum capital & leverage ratios, a capital conservation buffer and more stringent criteria for instruments eligible for consideration as capital as well as revised risk weights and calculation methodologies. All of these aim to improve the bank’s capital position and capacity to absorb losses and continue lending operations during periods of stress.

This post briefly walks through the minimum capital requirement and the credit risk weighted asset under Standardized Approach components of this regulation.

Minimum Capital Requirement

The minimum capital & leverage ratios are given below:

Tier 1 capital = Common Equity Tier 1 capital (CET1) + Additional Tier 1 capital

Total capital = Tier 1 capital + Tier 2 capital

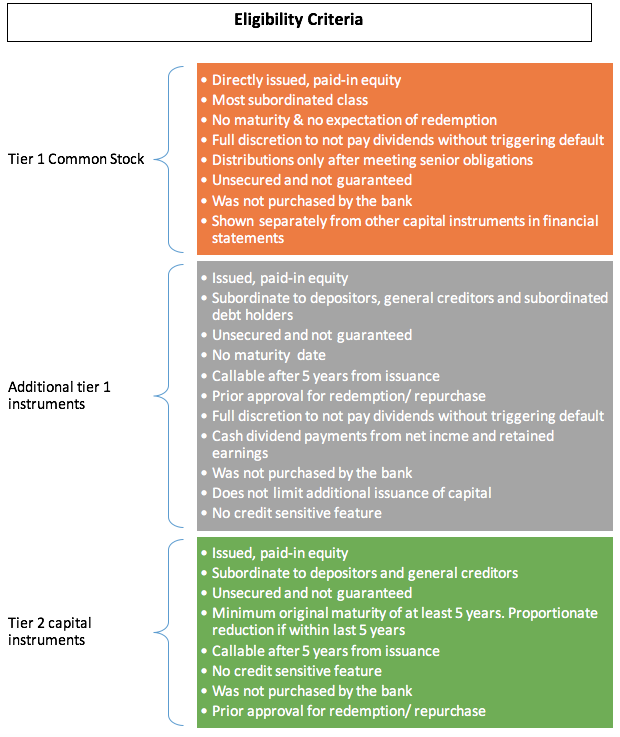

Common equity tier 1 capital consists of:

- Common stock

- Retained earnings

- Accumulated other comprehensive income (AOCI)

- Common stock minority interests, subject to limitations

- Less regulatory deductions and adjustments

Additional Tier 1 equity consists of:

- Non-cumulative preferred stock and related surplus

- Additional tier 1 minority interests, subject to limitations

- Less regulatory deductions and adjustments

Tier 2 capital consists of:

- Certain capital instruments (e.g. subordinated debt & preferred stock)

- Loan and lease losses allowance, subject to limits

- Total capital minority interest not included in tier 1

- Less regulatory deductions and adjustments

Regulatory deductions and adjustments from CET1 capital are as follows:

- Goodwill

- Other intangibles (except mortgage servicing assets (MSA))

- Deferred tax assets from net operating loss and tax credit carry forwards

- Any gain on sale in securitization exposures

- Any defined benefit pension fund assets (if not an insured depository institution)

- Excess of expected credit loss over eligible credit reserves, for advanced approaches

- Identified losses that would have reduced CET1 capital if recorded

- If AOCI opt-out elected then unrealized gains/ losses on available for sale & held to maturity instruments need to be adjusted

Other deductions from regulatory capital are as follows:

- Investments in own capital instruments will be deducted from the relevant regulatory capital component based on own capital investment. For example, own common stock investments will be deducted from CET1 capital.

- Reciprocal cross holdings in the capital of financial institutions, non-significant investments in the capital of unconsolidated financial institutions and significant non-common stock investments will be deducted from the relevant regulatory capital element using the corresponding deduction approach. If the capital component against which the deduction is to be made is insufficient, the remaining amount will be deducted from the next higher regulatory tier.

- Mortgage Servicing Assets (MSA), DTA from timing differences and significant common stock investments in unconsolidated financial institutions in excess of the individual and aggregate limit thresholds of 10% and 15% of CET1 will be deducted from common equity tier 1 capital.

Capital conservation buffer & countercyclical capital buffer

a. Capital conservation buffer

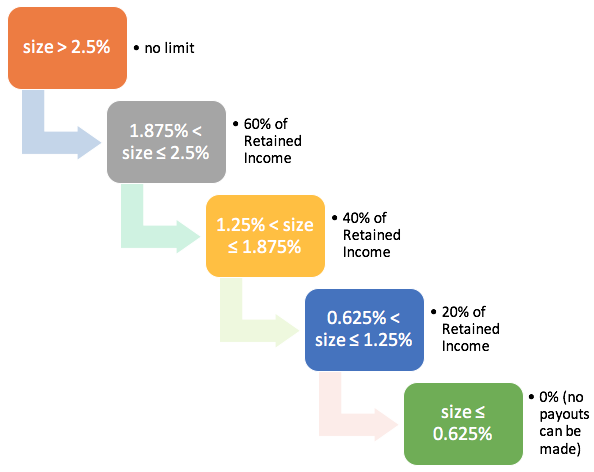

The regulations also introduce a capital conservation buffer of 2.5% (on full implementation) comprising of common equity tier 2 capital. If the capital held by the bank does not satisfy this buffer there are restrictions on distributions (e.g. dividends, share buybacks, discretionary bonuses). The minimum capital conservation buffer is assessed against the result of the following:

Size of Bank’s Capital Conversation Buffer = Minimum of {Bank’s CET1 ratio – 4.5%, Bank’s tier 1 ratio – 6%, Bank’s total capital ratio – 8%) , floored at 0%

The banks ratios are determined as of the last day of the previous calendar quarter.

If the result exceeds 2.5% then there is no restriction on the pay out that can be made. However, if the size is less than or equal to 2.5% the maximum pay out that can be made is limited as follows:

Note: The pay-out is assessed as a percentage of eligible retained income where the retained income is the net income from the four calendar quarters preceding the current calendar quarter less any distributions and discretionary bonus payments made and related tax effects. If the eligible retained income is negative, there will be no distributions made.

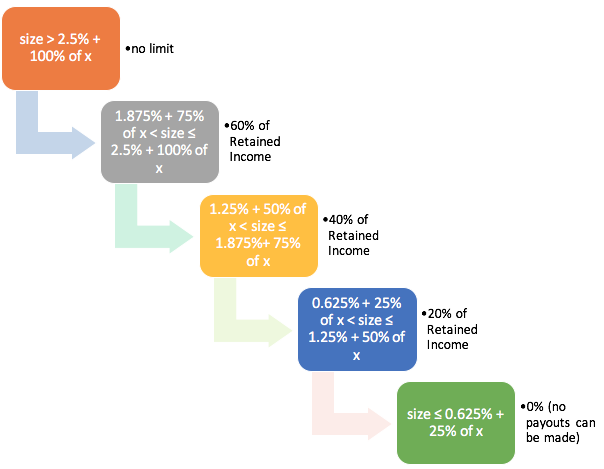

b. Countercyclical capital buffer

In addition for those banks approved for the advanced approaches, the capital conservation buffer used to determine the maximum payment out for distributions and discretionary bonus payments is increased by a countercyclical capital buffer amount (let’s call it x) as follows:

The countercyclical capital buffer amount, expressed as a percentage of risk weighted assets, is a weighted average of the countercyclical capital buffer amounts for the national jurisdictions where the bank has its private sector credit exposures.

Standardized Approach – Risk Weighted Assets – Credit Risk

Under the standardized approach, prescribed risk weights based on counterparty, type of loan/ property, etc. are applied to the exposure amounts to determine risk weighted assets. For off-balance sheet items including derivatives, on-balance sheet equivalent exposures are first calculated before the risk weights are applied.

a. Risk weights for general credit risk

| Exposure | Risk Weight |

| US government – directly & unconditionally guaranteed | 0% |

| US government – conditionally guaranteed | 20% |

| Other Sovereign | Based on Country Risk Classifications (CRC) applicable to the sovereign

OR Country OECD membership if CRC is not applicable:

OR Sovereign default (current or within the past 5 years) > 150% |

| US Pubic Sector Entities (PSE) | General obligation exposure >20%

Revenue obligation exposure > 50% |

| Foreign PSE | General obligation exposure:

Based on Country Risk Classifications (CRC) applicable to the bank’s home country

OR Country OECD membership if CRC is not applicable:

OR Sovereign default (current or within the past 5 years) > 150% Revenue obligation exposure: Based on Country Risk Classifications (CRC) applicable to the bank’s home country

OR Country OECD membership if CRC is not applicable:

OR Sovereign default (current or within the past 5 years) > 150% |

| Corporate | 100% |

| Residential mortgages | First lien meeting the following criteria >50%

Other >100% |

| Pre-sold construction loans |

|

| Statutory multifamily mortgage | 50% |

| High voltage commercial real estate (HVCRE) | 150% |

| Past due exposures |

|

| Other assets |

|

| Securitization exposure

Carrying value -/+ net unrealized gain or loss (if AOCI opt-out elected) |

1250% risk weight if the entity cannot demonstrate a thorough understanding of the structural features, the underlying loans and market & performance data of the securitization exposure.

In other cases, risk weights may be assessed using either the simplified supervisory formula approach or the gross-up approach. |

| Equity exposures | Equity exposures to investment funds > one of three look through approaches (full, simple modified, alternative modified)

Equity exposures that are not equity exposures to investment funds > simple risk weight approach 0% – 600% risk weights based on counterparty, type of investment, size of investment |

b. Off balance sheet exposures

Credit conversion factors are applied to off balance sheet items to determine the on-balance sheet equivalent exposure amount. Risks weights based on counterparty, etc. are then applied to the exposure amounts in a similar manner as is done for on balance sheet exposures to determine the credit risk weighted asset amount.

| Off balance sheet item | Credit conversion factor (CCF) |

| Undrawn unconditionally cancellable commitment | 0% |

| Not unconditionally cancellable commitments with original maturity of less than or equal to 1 year

Self-liquidating trade related contingent items with original maturity of less than or equal to 1 year Conditional equity commitments with original maturity of less than or equal to 1 year |

20% |

| Not unconditionally cancellable commitments with original maturity of greater than 1 year

Conditional equity commitments with original maturity of greater than 1 year Transaction related contingent items |

50% |

|

100% |

c. Derivatives

The exposure for the derivative contracts is sum of the current credit exposure and the potential future exposure.

The current credit exposure is based on the mark-to-fair value of the contract. The potential future exposure is the notional principal amount adjusted for credit conversion factors based on the contract’s time to maturity (≤ 1 year, 1 – 5 years, > 5 years) and type (interest, foreign exchange rate & gold, credit, equity, precious metals, other).

Risks weights based on counterparty, etc. are then applied to the on balance equivalent exposure amounts in a similar manner as is done for on-balance sheet exposures to determine the credit risk weighted asset amount.

In this post we have looked at the US implementation of Basel III capital ratios and the risk weights for credit risk under the standardized approach. In the next post we will look at the IRB approach