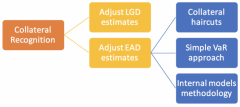

Collateral Recognition and Counterparty Credit Risk

6 mins read In the previous post we reviewed the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches

6 mins read In the previous post we reviewed the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches

5 mins read In our second instalment on capital adequacy regulations for US financial institutions, we look at the credit risk requirements under

6 mins read The Federal Reserve published revised capital adequacy rules and regulations in July 2013 that follow the Basel III revisions to

4 mins read CCAR The Comprehensive Capital Analysis and Review or CCAR process is a US Federal Reserve supervisory program. It targets large

6 mins read Brexit reference for dummies. European Union – a brief history The European Union, previously known as the European Commission and

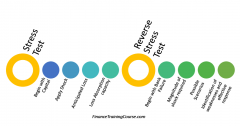

9 mins read A typical stress test creates a scenario and evaluates how a bank would fare under it. In comparison to reverse