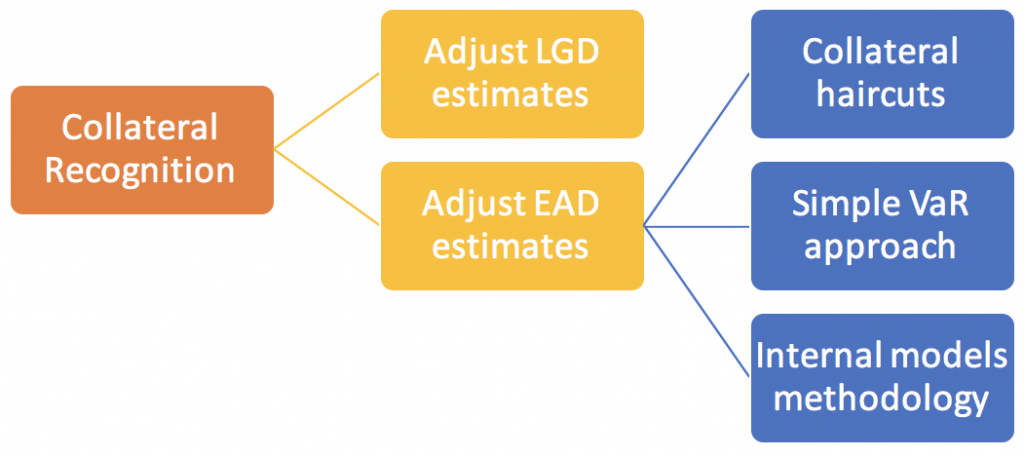

In the previous post we reviewed the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches (AMA). In this post we focus on the various methods to recognize financial collateral in counterparty credit risk calculations. Eligible collateral is used to mitigate counterparty credit risk. Recognition may be made by adjusting the Loss Given Default (LGD) estimates or Exposure at Default (EAD) estimates. We will discuss the methods of adjusting EAD for collateral recognition here.

When calculating counterparty credit risk for repo style transactions, eligible margin loans, over the counter (OTC) derivative contracts or single product netting sets of such transactions, financial collateral may be recognized for mitigating counterparty credit risk.

The impact of collateral is either factored in the calculation when LGD (Loss Given Default) is estimated or alternatively, may be factored into the EAD (Exposure at Default) measure using the following approaches:

- Collateral haircut approach

- Simple VaR approach (for single product netting sets only)

- Internal models methodology

Note that if adjustments are made to EAD, the LGD will be estimated as if it were unsecured by collateral.

1. Margin Loans & Repo Style Transactions

Collateral recognition for eligible margin loans and repo style transactions may be carried out using the collateral haircut approach, the simple VaR methodology or the internal models methodology. The latter approach will be discussed in the OTC derivatives section while the former two approaches are reviewed below.

Collateral haircut approach

Where

ΣE= Value of exposure

ΣC= Value of collateral

Es = Absolute value of net position (net of collateral) in a given instrument or gold

Hs = Haircut for market volatility in the price of a given instrument or gold.

Efx = Absolute value of net position (net of collateral) in a given instrument or cash, in a currency that is different from the settlement currency

Hfx = Haircut for current mismatch between the currency of Efx and the settlement amount to account for volatility in exchange rates.

Haircuts used under the collateral haircut approach may either be the prescribed standard supervisory haircuts given in the rule document or the entities own estimates based on historical data.

Standard supervisory haircuts

Prescribed haircuts for market price volatility range from 0% (for cash collateral) to 25% (for publicly traded equities not list on the main market index) based on the issuer type, rating grade, risk weight residual maturity and instrument type of the net position.

The standard supervisory haircut for foreign exchange rate volatility is 8%.

The standard supervisory haircuts are quoted based on a 10-business day holding period for eligible margin loans. For repo style transactions the haircuts are multiplied by a factor of , i.e. the haircuts are based on a 5-day holding period.

The supervisory haircuts would need to be scaled upwards if holding periods are longer than 10 business days for eligible margin loans and 5 business days for repo style transactions.

A twenty business day holding period will be used for single product netting sets if the number of trades exceed 5,000 or if there are one of more trades with illiquid collateral.

Own estimates for haircuts

Haircuts are based on the institution’s internal estimates of the market price & exchange rate volatilities. The use of these estimates depend on the entity meeting the following criteria:

- The estimates should be derived at the 99th percentile one tailed confidence interval

- Estimates should be determined for a 10-business day holding period for eligible margin loans or a 5-business day holding period for repo style transactions. If estimates can only be derived for other holding periods, they will then need to be scaled to the standard holding basis quote.

- The inputs used in the estimate need to be calibrated to 12 continuous months of historical data. The period selected should be one that represents significant financial stress for the given instrument.

- Policies and procedures for determining the financial stress period used must be documented and followed. Empirical evidence of the financial stress period must be made available, if required by the supervisor.

- The supervisory authority may require the entity use a different financial stress period from the one it has used to derive its estimates

- Revisions to dataset and haircut estimates should be made at least once every quarter, or earlier if there are material changes in market conditions

Simple VaR methodology

This approach is used for single product netting sets.

Where

ΣE= Value of exposure

ΣC= Value of collateral

PFE = Potential future exposure = Best estimate of the increase in the value of for a 99th percentile one tailed confidence interval. A 10-business day holding period is used for eligible margin loans & 5-business day holding period is used for repo style transactions.

The VaR model should use at least one-year of empirical data and should be back tested on a regular basis.

2. OTC Derivatives

The collateral haircut approach may be used to recognize collateral for OTC derivatives. Alternatively, an internal models methodology may be used.

Collateral haircut approach

The collateral haircut approach as discussed above will be used for collateralized OTC derivative contracts. Haircuts are quoted based on a 10-business day holding period. For OTC derivatives that cannot be easily replaced, the haircut will be adjusted for a 20-business day holding period.

The exposure in the EAD formula, i.e. ∑E, will be calculated using the current exposure method discussed below.

Current Exposure Method

OTC derivatives with no qualifying master netting agreement

The EAD (before considering collateral) for OTC Derivatives not subject to a qualifying master netting agreement, will be assessed as single OTC derivative contracts where EAD will be determined as:

EAD = Current Credit Exposure + PFE

Where

Current Credit Exposure = Max (0, Mark to fair value of the contract)

PFE = Effective (rather than stated) Notional Principal Amount of the contract × Conversion factor

The conversion factors, prescribed in the rule document vary by type of contract and remaining time to maturity/ reset.

OTC derivatives with qualifying master netting agreement

The EAD for multiple OTC Derivatives subject to a qualifying master netting agreement will be assessed as follows:

EAD = ∑ Net Current Credit Exposure + Adjusted sum of PFE

Where

∑ Net Current Credit Exposure = Max (0, Net sum of all positive and negative fair values of the contracts)

Adjusted sum of PFE, Anet = 0.4 × Agross + 0.6 × NGR × Agross

Agross = Gross PFE for each contract in the master netting agreement = Effective (rather than stated) Notional Principal Amount of the contract × Conversion factor, where the conversion factors, prescribed in the rule document vary by type of contract and remaining time to maturity/ reset.

NGR = Net to Gross Ratio = Net Current Credit Exposure / Gross Current Credit Exposure, where

Gross Current Credit Exposure = ∑ positive fair values

Internal Models Methodology

The internal models methodology may be used to determine the EAD for counterparty credit risk for collateralized as well as uncollateralized OTC derivative contracts, eligible margin loans and repo style transactions and single product netting sets of these transactions.

The supervisory authority needs to give prior approval for use of this method. Approval is subject to a number of criteria related to the model’s measurement capabilities, the entity’s ability to measure, monitor and control counterparty exposures, wrong way risk, collateral and margin amounts, the use of historical data in current and stressed scenarios, model validation & review, and the entity’s stress testing program. If approval is given to use internal models methodology for a given transaction type, it must be used consistently for all transactions that fall in that category.

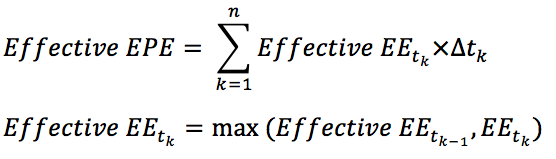

The process for determining EAD using the internal models methodology is illustrated below:

Both EE & EAD are determined for unstressed and stressed scenarios. Unstressed scenarios use recent data for the calculation of EE & EAD while stressed scenarios are based on data from a historical period which contains a period of stress to the credit default swaps of the entity’s counterparties.

EE is based on the probability distribution of changes in fair values. It may include financial collateral in its calculation.

EAD is calculated as follows:

EAD = Max (0, α × Effective EPE – CVA)

Where,

CVA = credit value adjustment of any OTC derivative netting set recognized on the entity’s balance sheet

tk = kth future time period in the model

α= 1.4

With approval from the supervisory authority EAD may reflect the impact of collateral agreements when additional collateral is received on account of an increase in counterparty exposure but not when additional collateral is received to compensate for a decline in the counterparty’s credit quality. The rule document specifies two alternative approaches how collateral agreements may reflected in EAD.

The maturity, M of the exposures will be calculated as follows:

- If the remaining maturity of the exposure or longest date contract in the netting set is greater than 1 year; M = min (5 years, M(EPE))

- If the remaining maturity of the exposure or longest date contract in the netting set is less than or equal to 1 year; M = 1

Where

dfk is the risk free discount factor for future time period tk.