Insurers estimate IBNR reserves as part of their claims reserves estimate for reporting on their financial statements. Claims reserves are estimates of claims that have occurred on or before the financial statement report date but which have yet to be paid. A current liability has to be reported regularly on the insurer’s financial statements even though the actual final settlement cost of the claims may be unknown to the entity on that date. Accuracy of these claims reserves estimates is important to the insurer for a number of reasons. It impacts the insurers:

- Profitability, financial position, and strength which influences how investors and regulators view

- Pricing, underwriting, strategic and financial decisions made by its management

Inaccurate estimates will project an incorrect view of the insurer’s health. It may result in investors and regulators taking actions that may be detrimental to the company. The insurer’s own management may take incorrect and possibly adverse action to correct perceived failings or benefit from perceived wellness that erroneous estimates convey.

1. Claim Reserve & IBNR reserve

Claims reserves comprise of two main portions:

- Outstanding case reserves for claims incurred and reported as of the financial report date

- Incurred but not report (IBNR) claims reserve estimate, as mentioned above, which consists of:

- A pure IBNR reserve estimate i.e. claims that have incurred but which has not yet been reported to the insurer

- Provision for the future development of claims already reported to the insurer

- A provision for claims that will reopen in the future

- Provision for claims that have been reported but which are not yet recorded in the insurer’s books

Outstanding case reserves are determined by the insurer’s claims department or an independent claims adjuster hired by the insurer. The IBNR reserve estimate, on the other hand, is usually determined/advised by an actuary. The focus of this post is on the latter estimate.

2. Unearned Premium Reserve (UPR) & Premium Deficiency Reserve (PDR)

In Pakistan, according to the Insurance Ordinance 2000, a non-life insurer is required to hold an unexpired risk liability. This is valued at not less than the sum of unearned premium reserve and the premium deficiency reserve, where the:

- Unearned premium reserve (UPR) is the unexpired portion of the premium which relates to business in force at the balance sheet date; and

- Premium deficiency reserve (PDR) is the amount if any by which the expected settlement cost, including settlement expenses but after deduction of expected reinsurance recoveries, of claims expected to be incurred after the balance sheet date in respect of policies in force at the balance sheet date, exceeds the unearned premium reserve.

3. Checklist

This post is a summarized to-do list and serves as a broad checklist when estimating IBNR reserve. A couple of points to review for contiguous UPR & PDR reserve estimations are also mentioned. Some practices are generic by nature and may extend beyond the valuations mentioned here. Please note that it does not provide specific details of IBNR, UPR and PDR calculation methodologies. It is simply a list of questions to pose and ponder on and areas to review before, during and after undertaking such an exercise.

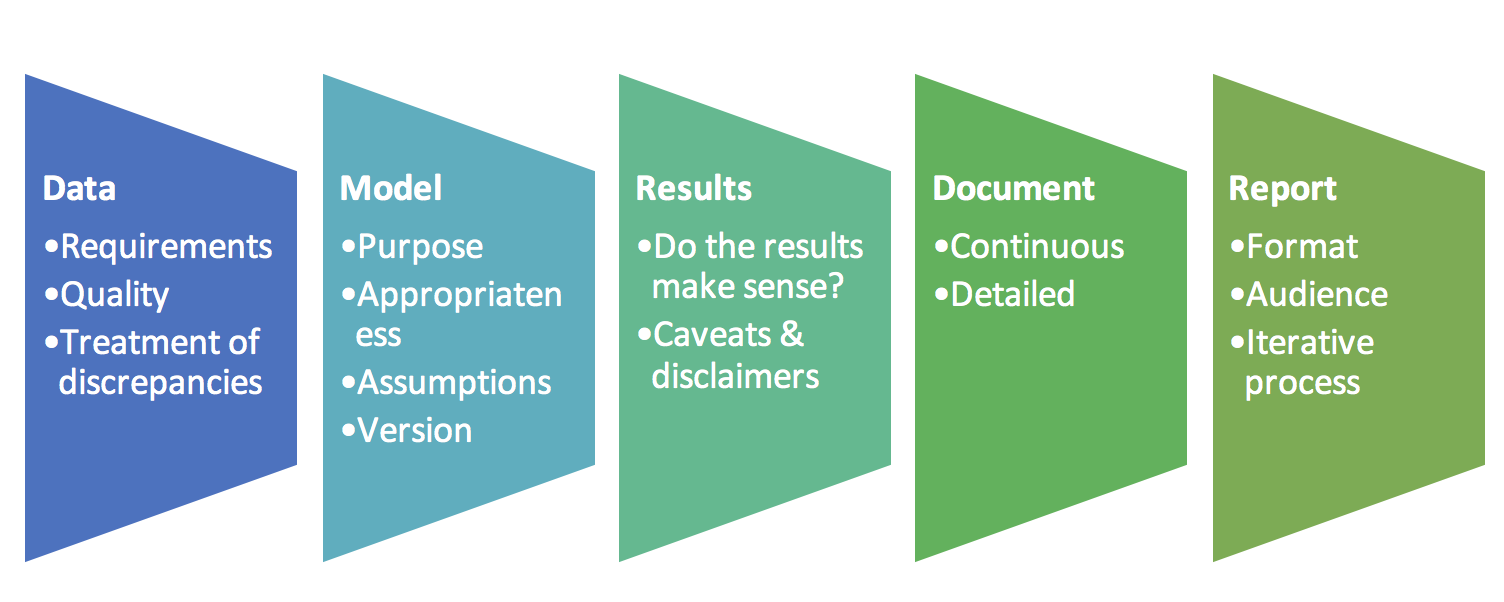

a. Data Requirements

For IBNR estimation at a minimum the data obtained from the client should contain the following:

- Class of business

- Product type

- To date of the policy

- From date of the policy

- Policy number

- Claim number

- Claim amount

- Loss date

- Intimation date

- Claim paid dates

- Claim settlement expense

- Reinsurance paid – reinsurer’s share of the claim amount

- Reinsurance paid – reinsurer’s share of claim settlement expenses

In addition, for a UPR & PDR reserve estimation exercise the data should consist of:

- Written, earned & unearned premium by line of business

- Financial statements – claim, premium, expense, income statements

b. Data Quality Checks

Data quality is an important factor for the IBNR reserve estimation process as it directly impacts results obtained. Controls should be in place at the company to ensure that all required data is being accurately captured using designated parameters and constraints where applicable.

The data fields should be consistent across the years of claims data. Apply any changes to headings and labels or parameter fields consistently to all years’ data. Ideally, a legend should be provided so that fields captured are clearly understood by users of the data.

Reconcile the current year’s data with the past years’ data and movements in the claims data over the year. If more than one source of data is available, the information should be reconciled across sources. Explain and address reconciliation differences.

Basic checks include:

- Subtotals & Totals should be verified and crossed checked against other sources like the accounts, financial statements, internal MIS, etc.

- Consistency should exist between loss, intimation & claim paid dates for a particular claim (e.g. loss dates falling after claim paid dates should raise a flag), amounts retained and reinsured (e.g. the sum of amounts cannot exceed the total claim amount), etc.

c. Treatment for data problems

While it is ideal to have all data discrepancies and inconsistencies addressed prior to the disclosure and regulatory submission of IBNR reserve estimation results, it may not always be possible given time constraints. To handle data that may be incomplete or incorrect, treatment is assigned and results are qualified accordingly with necessary caveats.

If there are multiple sources of data and one source is treated as the primary data source, missing data may be gleaned from other sources.

Each discrepancy identified should have a corresponding treatment implemented and documented. All such treatments have an impact on results to either a lesser or greater extent. Each treatment adds a layer of uncertainty to the IBNR reserve estimate. Therefore, the client must be made aware of this. Concrete steps need to be put in place to address data quality issues.

d. IBNR Model Selection

Choose a model chosen that ties in with the purpose of the estimation exercise.

i. Regulatory Submission

If the purpose is regulatory submission, entities follow the rules and methods prescribed by the supervisory authority. Regulators may require insurance companies to periodically estimate their IBNR reserves to assess adequacy. A method is usually prescribed to ensure a degree of uniformity in practice, comparability across entities and a minimum standard or benchmark for the industry. For example, the Securities and Exchange Commission of Pakistan prescribes the Chain Ladder approach for IBNR estimation. Its illustrative example using the volume weighted technique for calculating lag factors using the yearly development of claims.

ii. Internal reporting

If the purpose is internal reporting, you may use one or more methods to obtain estimation results, such as chain ladder, expected claims, Bornhuetter-Ferguson, Frequency-Severity Techniques, etc. Methods selected may be based on the regulator’s prescribed method or may take into account the nature of claims of a given business line.

Internal reporting would likely be on a more frequent basis (e.g. monthly) than regulatory reporting. It should ideally be linked to decision making, risk management & capital planning.

Internal IBNR reserve calculators can serve as audits or cross checks against results opined by external independent auditors and actuaries. A significant deviation could be sources of discussion and further investigations between concerned parties.

iii. Other factors

Does the business line experience low frequency/ high severity claims? Or high frequency/ low severity claims? Also, consider the years of credible historical experience available. Is the business line a new line or for a new target audience or territory? Or is it an established line with years of claims data behind it? Apply methods consistently across successive periods so that we may evaluate emerging trends.

Development tables may be built independently or incorporated within the entity’s business intelligence (BI) system. They should allow the user to vary parameter selections such as granularity (combinations of business lines and/ or product types), full development year, lag factor calculation approach, etc. Calculate development factors from these development tables but they should be editable to consider or exclude data anomalies, reinsurance impact, downward development, stability & smooth progression across development periods, tail factor, etc. Determine cumulative claims development factors, ultimate claims & IBNR reserve estimates from the selected claims development factors.

e. Appropriateness of the IBNR & UPR models

Deviations from the regulator’s prescribed methodology may be allowed but will usually need to be supported with sound reasoning. For IBNR reserve estimation for a new line of business, the chain ladder approach may not be appropriate as sufficient data is not available to get credible results. An Expected Claims Technique may be used by the entity instead based on the experience of a similar line with sufficient claims history or the Bornhuetter-Ferguson approach may be used to credibility weigh results from both actual claims data and estimated expected claims data.

In the case of UPR, for example, it may not always be appropriate to use the twenty fourths method commonly prescribed and used to calculate the reserve. The underlying assumption for the twenty fourths method is that the majority of policies have tenors of one year with issue dates that are more or less uniformly spread out over the year. The twenty fourths method would not be appropriate for policies covering seasonal products such as some forms of agricultural insurance with tenors of 6 months or less. Insurance regulations recommend a proportion of gross premium approach based on the ratio of the unexpired period of the policy and the total period, both measured to the nearest day in such instances. Data constraints or data quality issues that relate to policy period dates may play a role in deciding whether to apply this exact alternate approach or an approximate method.

f. Model assumptions

Model results will vary based on the data and assumptions used for the estimation exercise such as:

- Paid claims or reported claims data used

- Link factor calculation approach – simple, volume weighted, medial average, geometric average

- Full development year

- Development factors selected

- Loss ratios

- Credibility factors

- Include the impact of reinsurance or not

g. Versioning & version history

Label each model developed with version and date. The version ultimately implemented or used for determining results for regulatory submission should clearly be labeled FINAL.

Ideally, each revision should contain a version history documenting the changes since the prior version, why and by whom. If peer review is conducted, then the date of review and name of the reviewer may also be recorded.

h. Results – Do they make sense?

i. Reconcile current year results with prior year results.

- What are the expected changes?

- How have premiums grown since the last results?

- What is the growth in incurred claims since the last results?

- How do you explain unexpected changes?

- Are there any anomalies in the claims development patterns? What are the reasons for these anomalies? Are they due to systematic changes or idiosyncratic one-off events?

- What are the changes in methodology and assumptions?

- Have there been any changes in underwriting practices since the last valuation?

- Have there been any changes in claims administration procedures since the last valuation?

- Has the method for estimating outstanding claims reserves changed over the preceding years?

- Was the IBNR estimate in prior years for a given business line adequate based on the actual claim development of that line to date?

ii. Consistency

- Simple cross checks such as claim ratios and ratios of IBNR reserve to claims incurred of similar business; or applying the development of the latest fully developed accident year to recent accident years’ data to get a crude IBNR estimate, etc. may give some insight or a broad picture view of result appropriateness.

- Consistency between results with and without the impact of reinsurance

- Development factors for the net and gross claims should have a reasonable relationship

- Caps may be set so that net IBNR reserves in each accident month/year are not in excess of gross IBNR reserves.

iii. Treatment for unexpected changes

- Discuss development pattern anomalies with the client and understand their impact. Should we exclude claims that contribute to these anomalous patterns and treat them as outliers? Or should we consider them in the calculations as they may be indicative of a new normal?

- Should calculations go more granular versus less granular in terms of estimation by business line/ subline/ product? The degree of granularity impacts results and needs to be considered carefully:

- More granular. One impact, particularly in the case of PDR is that increased granularity leads to increased PDR especially for less mature lines with sparse data. Consider the following when reviewing granularity:

- Is there sufficient data to go more granular?

- Is there a need to revise IBNR reserve estimation methodologies for certain sublines (from the prescribed method)?

- Less granular – combining certain product types or sublines (presumably with similar characteristics) for IBNR estimation may

- lead to a distortion of overall results or

- mask important trends or risk in certain sublines or

- lead to cross subsidization of loss bearing/ risky business sublines with profitable sublines

- More granular. One impact, particularly in the case of PDR is that increased granularity leads to increased PDR especially for less mature lines with sparse data. Consider the following when reviewing granularity:

i. Caveats & disclaimers

Add caveats, disclaimers, and qualifications along with the results if:

- there are deviations in methodologies from prescribed regulations and standards or

- if the data was subject to simplifying treatment because of unresolved data discrepancies,

Include a further analysis, a sensitivity study of sorts, to show how results would change if we revise the data & assumptions.

j. Document – Continuous & Detailed

Documentation is a vital and continuous process. It begins on assignment confirmation to the time of the FINAL report’s submission and approval. It should be of sufficient detail to allow for replicability, understanding, and review by an independent peer reviewer or auditor.

Documentation consists of:

- Emails received and sent

- Data – characteristics, discrepancies & treatments. This will be particularly useful and allow for easy review and revision to the dataset if the entity addresses discrepancies in a timely manner prior to report submission

- Methodologies considered and implemented

- Queries and concerns raised & subsequent responses

- Minutes / key points from internal meetings and meetings with clients

- The final report submitted (see the section below)

k. IBNR Report

The report formally documents and discloses for the intended audience, the process followed and the IBNR reserve results obtained. The process must be of sufficient detail to allow another actuary to replicate the results. Highlight any recommendations and concerns.

i. Standard format & audience

In general, the report should follow the standard order listed below. The audience of the report dictates which section receives greater focus and weight.

- Executive Summary

- Scope & introduction

- Data

- Methodology & Assumptions

- Results

- Recommendations & conclusion

- Annexures (including EXCEL annexures)

Reports to senior management should focus on results, concerns, and recommendations. Relegate items that could potentially detract from this focus to a separate communication or include them as an annexure to the report. These include items such as details as data discrepancies and their treatment.

ii. An iterative process

Allow time for review and challenges of the results by the client. This keeps the process transparent and foster buy in of numbers and results. Such a review could reveal reasons for development pattern anomalies, internal company practices and policy characteristics that could lead to a review of methodologies, assumptions, data and results. Maintain versioning and version history to keep a track of drafts and final submissions. The list above is by no means comprehensive but is a basic go-to for us. What would you add to the mix?

References:

- Estimating Unpaid Claims Using Basic Techniques – Jacqueline Friedland – Version 3, July 2010

- Basic Ratemaking – Geoff Werner, Claudine Modlin – Fifth Edition, May 2016

- Considerations in the calculation of Premium Deficiency Reserves (under US Accounting Rules) – Ralph S. Blanchard