Investors – financial institutions, non-financial institutions, individuals – choose the FX Markets for a number of reasons that include hedging of their FX exposures against adverse currency movements, benefiting from a diversification of investments, earning a more attractive risk adjusted return, speculating and betting on the direction of a given currency based on the current and future political or economic environment, etc. Mis-selling by banks and FX brokers often to achieve higher profit margins, hinder investors from achieving these objectives and may even result in substantial losses for them.

There are a variety of FX products that could meet these requirements, including plain vanilla products such as forward transactions, cross currency swaps and currency options as well as more complex exotics such as target redemption forwards & swaps or target redemption notes (TARNs), dual currency deposits, currency coupon swaps, interest rate collars, caps, Knock in Knock Out options (KIKOs), etc.

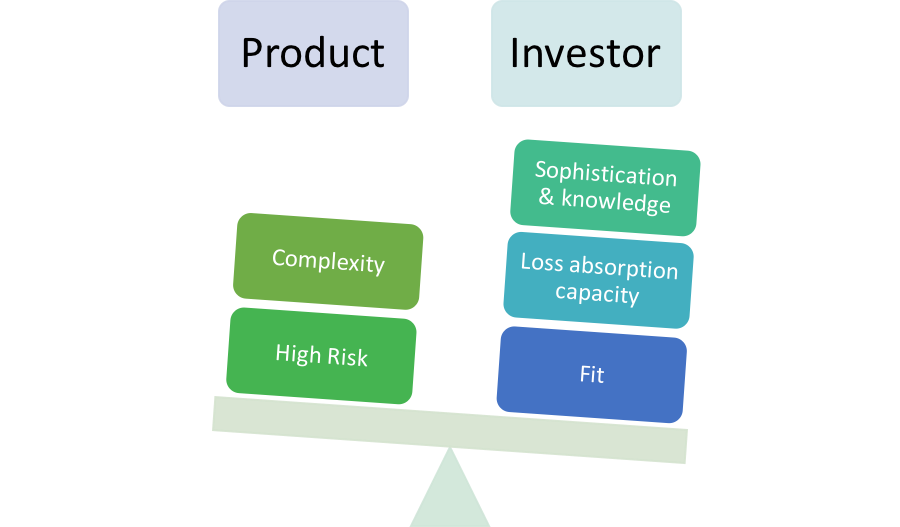

Why would an investor choose a more complex product variant over a simpler more marketable & liquid counterpart? Some of the reasons include:

- The offer of at-the-money options at low or no up-front cost for similar or higher returns compared to certain vanilla products

- A better structured fit (or at least the perception of one) to investors objectives

- Investors have been long standing customers of vanilla contracts from these banks/ FX brokers/financial institutions and now trust and feel obligated to them when offered (sometimes aggressively) more risky products by dedicated sales teams

- The products are not clearly identified as being exotics and appear as vanilla instruments with high risk features not adequately highlighted and explained, or down played given the current environment, by the sales teams.

Ideally taking on complex contracts should be commensurate with the degree of investor sophistication, education, need and risk tolerance. This primarily should be an assessment of whether or not investors:

- Have knowledge or have been sufficiently informed of the risks involved in such investments. Have the financial institutions or brokerage firms or banks clearly detailed investors of all inherent risks in the product? Have they observed their “duty to care”? Is the product disclosure transparent enough outlining all features of the transactions along with their associated risks? Can investors calculate the fair value of the transaction considering all its features and risks?

- Are aware of their loss absorption capacity. If the worst case scenario were to materialize will the potential size of losses wipe them out or will they be able to weather the storm? Has the investor carried out an independent evaluation of the risks and his risk tolerance under various stress and extreme scenarios? Or has he solely relied on the assessment presented by the derivatives sales team?

- Can assess the degree of product fit to their investment objectives. Does the product truly meet their investment objectives? Or have they been swayed by other features highlighted for the product such as low or zero cost structures or higher than expected return opportunities?

Numerous occasions have been documented where financial institutions, banks and brokerages have benefited from the profit opportunities inherent in the exotics by exploiting the lack of sophistication of their investor. They have done this by:

- Mis-selling products that were not appropriate for the investors’ FX requirements. One example was selling exotics as hedges against currency appreciation. The exotics at the initial stage met the IFRS accounting definition of hedges because of their zero initial cost structure. However, the effectiveness of the hedge was limited by the inclusion of features that terminated the contract if appreciation continued beyond a certain exchange rate. Another example was selling exotics as a more appropriate instrument that simple vanilla alternatives for speculating about currency movements. Vanilla options would have suited the purpose without the restrictions to gain and increased downside loss risk exposure that exotics entailed.

- Not adequately explaining or providing information on the features of the products. Without the necessary information investors evaluation of the contract’s fair value is imperfect. The addition of illiquid market unobservable features like caps and knock in/ knock out provisions further complicate the pricing.

In the recorded instances of mis-selling in emerging markets following the aftermath of the 2007-2008 financial crisis investors were often enticed by the lower cost and/or the better than expected rates of return on these products. In general, the exotics offered long at-the-money series of option positions in the local currency. A zero cost product was made possible by having investors simultaneously sell a series of options to the broker/ bank/ financial institution. Payments were on a monthly basis for a period of one or two years. Margin calls to put up additional collateral were required to cover potential losses. The product could not be terminated by the investor prior to maturity unless at a high break cost. The structures additionally contained features such as knock out barriers that limited gains to the investors and knock-in provisions that created the potential for unlimited downside losses for them. Downside losses was exacerbated by asymmetrical gearing i.e. where the short positions were structured to have notional values that were greater than those for long options. This left investors vulnerable to escalating and substantial losses when the foreign exchange rate moved in the wrong direction from that expected.

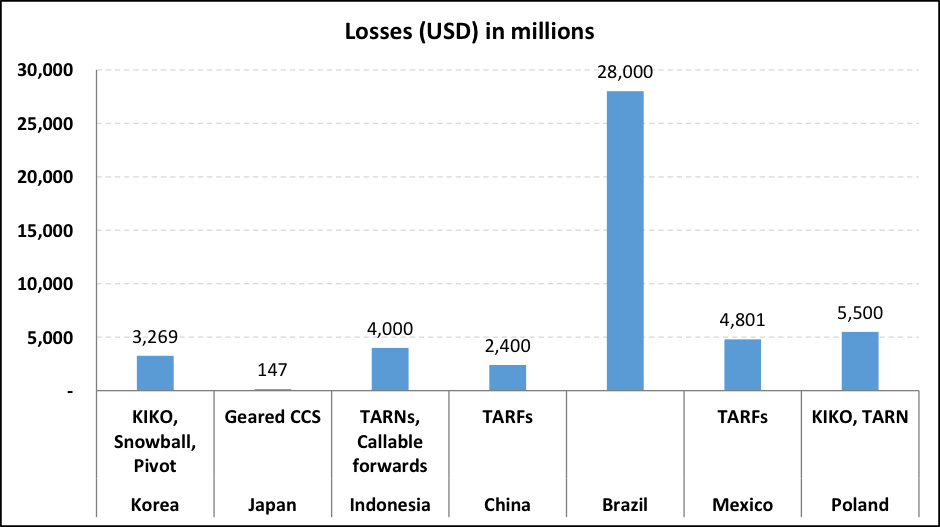

The graph below illustrates the losses suffered by non-financial companies in emerging markets from investing in various exotic FX derivatives. The source of this data is the IMF white paper mentioned below. Note that the loss amounts are only for the examples provided in the paper for which a numerical value has been provided. They do not include the losses from firms that were said to have been bankrupted by these products nor those who suffered a decrease in their capital bases or those forced to sell off assets. As details for losses listed in the paper were neither consistent for the countries mentioned nor complete, the losses do not necessarily represent the total losses that may have resulted for the named country. They, however, give a general idea of the inherent riskiness and extent of downside exposure of these products.

Some of the reasons cited for this proliferation in mis-selling in FX markets are listed below. They include:

- The need by small and medium enterprises for structured FX alternatives in light of traditional financial institutions such as banks curtailing the sale of such products to them

- Unlicensed, unregulated or lesser regulated sectors, such as FX brokers entering the market to fill the void left by the traditional banking institutions

- Greater profit margin opportunities in exotics compared to declining profit margins for vanilla products such as spot transactions

- FX sales teams rewarded and incentivized to aggressively sell exotics regardless of suitability and appropriateness for the investor

- The degree of unsophistication in non-financial firms needing protection against adverse currency movements compared to the degree of sophistication among derivative dealers offering these products

- Exotic transactions entered on a margin-call basis with cash or securities to be put up by the investor in favour of the brokers or banks when currency movements are in the wrong direction to cover potential losses

- The lack of transparency in product disclosure and pricing

- The ability by dealers to restructure over the period of the contract, simple hedging contracts into more complex and riskier ones

- The absence or insufficiency of regulation or power to enforce investor protection laws

- The absence of formal contract approval policies. These policies regulate either positive or negative lists of instruments that a dealer may or may not offer their customers

- Ineffective market surveillance and reporting policies

References:

- Playing with Fire – Randall Dodd – June 2009

- Exotic Derivatives Losses in Emerging Markets: Questions of Suitability, Concerns for Stability – Randall Dodd – IMF White Paper – July 2009

- Consultants fear mis-selling as forex brokers discover new options – Fiona Maxwell – Oct 2014

- Brexit volatility fuels FX mis-selling claims – Farah Khalique – Euromoney – August 2016

- Banks, brokers face post-Brexit mis-selling claims over FX options – White & Geddie – Reuters – Feb 2017