Trends, milestones and future outlook of the Pakistan Technology Industry

TL;DR; Habib University hosts Jawwad Farid and his talk on the history of Pakistan’s Technology Industry and its future outlook. Jawwad walks through 50 years of events, trends and milestones in less than 78 minutes. Delivered on 26th October 2018 at Tariq Rafi Hall as part of the Habib DSSE Public Lecture series to a mix audience of 250 people in Karachi.

When I first asked Dr. Waqar Saleem for an opportunity to speak to his class of freshman computer science students I thought we would have a group of 20, 30 students. Dr. Waqar Saleem though had other ideas. He suggested that rather than come speak to his class, we should move the talk to the Habib University public lecture series hosted by Dr. Moiz and open it up to a broader audience.

I am not sure what I was thinking but I agreed. My original reaction was that hardly anyone is going to show up to listen to me. The 20, 30 students I was originally planning on would at max become a mixed audience of 50, 60. As Habib University is in the other corner of the city and a 6 pm start on a Friday evening wouldn’t actually lead to a sellout crowd. So you can imagine my surprise when I found out that we had over 300 registration and 250 of them actually showed up on the evening of the talk.

Pakistan’s Tech Industry – 2005 – 2018 review

My game plan was simple. Together with my friends, colleagues and peers from the community of computer scientists we have seen three generational shifts in our space here in Pakistan. The technology industry has changed shape and evolved from the late 1980’s when we first started playing with personal computers as programmers to 2018 where we are really not sure how the next few years are going to surprise us. I just wanted to talk to the next generation of CS students to give them a heads up on some of the lessons we have learnt and some insights. With the hope that they won’t end up making the same mistakes we did. Even if they did, they would do so with their eyes wide open. In the process if we could come up with a framework or two, that would be a welcome bonus. That framework became the Geno-type of tech company founders and the skill set required to work with them.

Without further ado, here is the talk with a short supporting visual commentary and highlights to go with it

The Pakistan Tech Industry: Past, Present and Future from Habib University on Vimeo.

We started off with a list of core questions that we wanted to address.

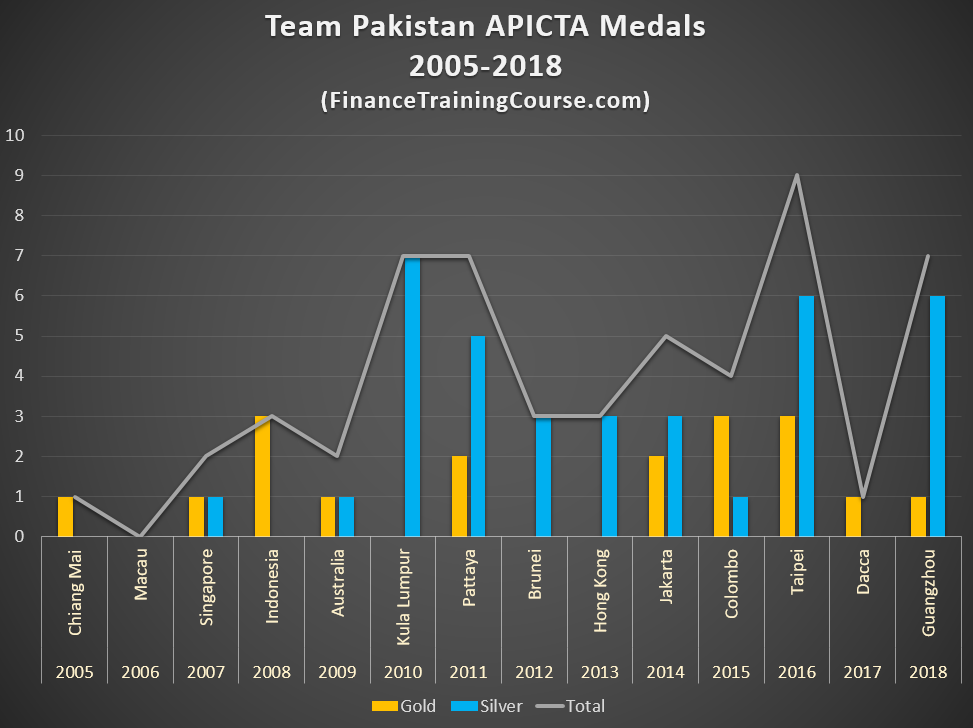

The biggest question and the first one on our mind was do we have what it takes? Is there something in our water that would allow us to excel? Where is the evidence? This is an old debate that gets revisited every time when we compare IT exports figures across the region. Maybe one of the reason why we haven’t done so well is because we don’t have the right talent. In its simplest form it poses the question do we have the talent to make this work?

The lens we choose to answer this question was Team Pakistan performance at the Asia Pacific ICT Awards aka the APICTA awards from 2005 to 2018. That is a thirteen year window to gauge our performance using our performance in an independent, isolated, external sector. The awards are scheduled every year. In 2018, they were held in Guangzhou, China and will be held in and around Hanoi, Vietnam in 2019. This year the delegates to the awards included 376+ entries, 270+ teams, 22 economies, 23 award categories and 80+ judges. Our performance within this competition over the years should be able to answer the talent question and how we rank in the region.

The biggest wins we scored were in Kula Lumpur (Malaysia) in 2010, Pattaya (Thailand) in 2011, Taipei (Chinese Taipei) in 2016 and Guangzhou (China) in 2018. Our winning trend across the years showed that we didn’t just have talent and ambition, we also consistently had great products, good stories, significant depth and knew how to deliver our sales pitches in an effective and impactful manner to judges who did not always came from Pakistan. In our good years (Taipei and China) we have ranked as high as 3rd and 5th across 22 economies. While being judged by a diverse group of qualified judges from the same 22 economies.

Within the APICTA performance we then highlighted 9 teenage winners of the school project category. The youngest of our team members and representative of the shape of things to come. Kids who over four different years between 2009 and 2018 convinced us that there is something in the water, that we do have what it takes.

Starting off with Zayd Enam who made it to UC Berkley and Stanford and dropped out of his PhD program to make it to the Forbes 30 under 30 list and co-found Cresta and finishing off with Nazar and Sofia Khan who at the age of 13 and 11 years wrote their own OCR and engineered true type fonts for word using hand writing samples, citing research papers as teenagers that PhD students have difficulty understanding and decoding.

The next big question was how big we are? More importantly how have we grown relative to the other industries that we compete with on the attention spectrum in Pakistan.

Some context before we answer the question. Pakistan total exports (Goods + Services, all sectors and segments) grew from USD 20 billion a year in 2005 to USD 29.9 billion a year in 2018. So by a third in 12 years. Of this services exports grew from USD 3.7 billion a year in 2005 to USD 5.18 billion a year in 2018. Once again by a third in the same 12 years.

It’s growth but its not phenomenal growth. Within this time frame we went through the financial crisis, a shortage of water and power crisis, two major political crisis, the invasion of Afghanistan and the war on terror by Allied Nato forces and a devastating domestic wave of terrorism that put the country on several travel advisory lists. So not the best of times for growth and certainly no walk in the park.

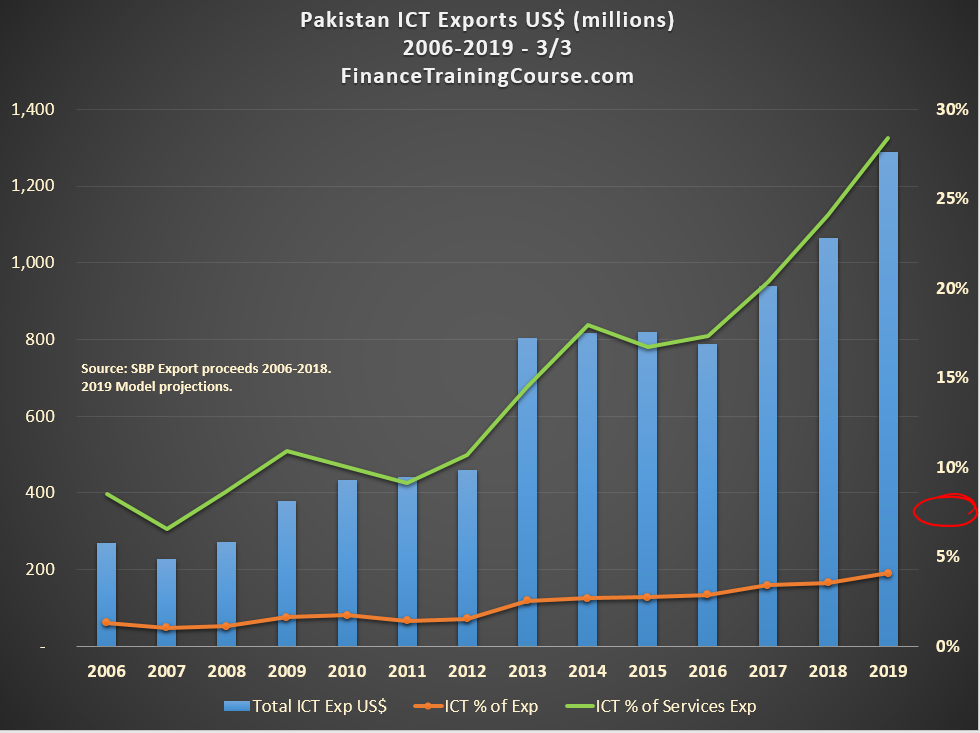

The fact that exports grew at all despite the chaos is a testament to our resilience. From an ICT perspective though the picture is even more encouraging. The big takeaway during the talk and the graphs presented was that ICT Exports have grown from 1% of total exports in 2005 to 4.25% of total exports in 2019. Not by a third but by three times. This is using the official SBP figures for export proceeds generated, billed and remitted by the technology industry back into Pakistan.

The move from under US$ 270 million a year to US$ 1.28 billion a year (projected 2019) is a big one but is over shadowed by the shift that becomes visible when we move to a slightly different lens. IT exports are part of the services export component of our economy. It is not fair to compare them with goods and services. When we move to services exports and use that as a benchmark, we have grown from 7% to 24% of total services exports in the last 12 years. Essentially replacing the bulge that was initially created by the Coalition Support Fund (CSF) payments between 2003-2012 and the subsequent gap when the same CSF payments were put on hold in 2016-2018.

As we mention in my chat shifts like these take decades, we have managed to achieve them in less than 13 years. In the same economic environment in which the rest of the economy was growing at 3% a year, we grew ICT exports proceeds at a much much faster clip. Takeaway for the community, for the government, for the policy hacks; feed your winners.

We closed this discussion by taking a stab at the the size of the industry. Actual versus reported figures. SBP estimates versus industry benchmarks. This is a sensitive area and the answer vary depending on your perspective and point of view and the benchmark you use to size the industry.

We then moved on to taking a look at the underlying business model and the rate structure the technology industry has used to charge clients for the last two decades. Some of the things we have to improve and fix and as well things we have already done to increase these rates. The rate structure was also the right time to discuss the history of the industry and how we have gotten to where we are today. The multiple generations we have jumped to get to the current environment. Starting from the initial accounting, payroll and EDP services businesses to dedicated, focused, niche domain heavy product plays that generate more than 40 million dollars a year for their founders.

We also discussed why the underlying industry business case needs a revamp. A revamp that would only be possible if we make a serious effort to moving from a services only model to a product oriented model. The case is simple the services rate is still stuck at the 8 to 12 dollars an hour range. It has been stuck there for close to twenty five years. There is not a lot of room for growth here and its not going anywhere. Other than adding raw talent or the mix, the only way to grow the average rate is to move up in sophistication and complexity of services. The more we move up the ladder the closer we get to a point where a shift to products is viable. That shift doesn’t just represent a shift in rates, it represents a focus on creating long term intellectual property for the industry and community that would make it possible for us to jump again from the current 1.2 billion dollars a year to the 3 – 7 billion dollars a year notch on the exports front.

There is a lot to be said about true profitability of the industry but it boils down essentially to a link between specialization, expertise and chargeable rates. We looked at ten of the leading names and players and found that the common thread across all of them was focus and specialization. So as a young computer science graduate the smartest thing you could do right now is to specialize in a given segment and pick a product based business as your employer rather than opt for the thankless and ultimately dead end services play. To be fair there is a risk in specializing too early and locking yourself down in a dead end but you must always remember that the way through most profitability barriers is through specialization.

The closing twenty minutes of the talk focused on some of the things we need to do to be successful as aspiring technology founders. It used the Geno-type of founders and companies to segregate the underlying required to run a specific type of a company as well as opportunities available in the local market for aspiring founders and startups. We spoke about the required skill set and the missing magic ingredient that we need to incorporate in our work ethic if we are to rise from our current level.

In conclusion, over the 2005-2018 period the industry has done well despite the many challenges we have faced together as a nation. At the current paths in our evolution we have two choices. We can walk the old way, the safe and easy path, and be locked in mediocre and declining profits for the next three decades. Or we can pick the odd choice, the difficult options and hew a new path from the rough and awkward undergrowth of shaping and crafting new products to a new land of opportunity. That choice will not be made by industry elders. It is a choice that the next generation of computer science graduates will make by opting for running their own shows versus accepting offers on team, ideas and businesses that are already irrelevant and outdated.

The impact of these decisions will become visible in the next ten years. But there are leading indicators already in place that show that this silent revolution of choice is well underway. Where we had one thirty million dollar local business 15 years ago, we now have ten. Where home grown product focused companies could be counted on the fingers of one hand, we now have fifty plus promising ideas doing well. Where fresh graduates would opt for safe names and jobs with guaranteed pay, we are increasingly seeing more startups sprout across the land. The industry is cognizant of the fact that good talent is now difficult to convert and acquire and requires a very different conversation compared to the one we had when we first started off as computer scientists 25 years years ago. Some have bought into the idea and are changing. Some have difficulty accepting the new environment and will fade out and disappear as they get left behind by a group focused on breaking old chains and moving forward.