What can history teach us about Oil Markets?

We don’t have to look too far back. The last ten years have enough twists and turns to keep us engaged.

2008 dramatic rise in crude oil prices and the subsequent crash is recent memory. Prices for West Texas Intermediate (WTI) blend closed at US$145.31 on 3 Jul 2008 per barrel. Less than six months later on 23 Dec 2008 prices closed at US$30.28.

There were multiple reasons for this roller coaster ride. One, increased market liquidity due to interest rates cut cycle launched by Federal reserve lead to re-inflation of commodity prices. Lower interest rates lead to higher liquidity. Cost of borrowing cash became lower. The cost of keeping cash sitting idle in your bank account became higher. Investors look for higher returns outside of bank deposits and bonds. With lower rates and increased liquidity their risk preferences shift.

Two, trading emphasis on peak oil (we have hit maximum liquid fuel production as a civilization). The trading thesis for peak oil is simple. At some point in time we are going to run out of oil to pump. When it becomes apparent to markets, whatever little oil we have left will trade up in prices. Significant uptick in crude consumption figures in China and India and decline in production across oil fields was the fuel peak oil needed to come in vogue. The result: large speculative bets on the direction of oil prices by traders and hedge funds.

Coupled with increased demand, paper oil (deliverable crude oil future contracts trading on exchanges) traded at historical volumes signaling an allocation of investment risk capital to oil. When markets tanked the unwinding of the same paper positions created additional downward pressure on oil prices leading to wild swings within a ten-month window in 2008. Markets love to feed on irrational exuberance and overblown panic. Crude oil saw a mix of both that year.

An uneasy peace prevailed in markets in following years. Oil prices recovered to low seventies within ten months of 2008 oil price crash. They remained range bound between low hundreds and high eighties throughout 2009 to 2014. There was some excitement and a retrenchment in August 2011 when Standard and Poor cut credit rating on US sovereign debt by a notch. The cut was heard around the world and commodity markets fell but recovered.

November 2014 is the month when the floor beneath crude oil prices crumpled again. Unlike 2008 or 2011 where the crash was followed by recovery within a few months, this time the price collapse stuck. There are two theories of what lead to the supply glut that lasted throughout 2015 to 2017.

The first explanation is that the Kingdom of Saudi Arabia declared war on shale oil producers and Iran by ramping up production. The Saudi strategy had two clear objectives. One, push prices down to a point where shale producers are no longer profitable and that segment of the industry is driven off the table. Bloodied, with depleted capital, rigs closed and investors scared off by Saudi might and the ability of the Kingdom to control the markets by setting prices. Two, deny Iran the benefit of high oil prices if or when sanctions on Iran are lifted. Ensure that Iranian stored oil in offshore tankers hits the market at lowest possible prices. Ironically enough despite the pain felt by shale producers and Iran, lower oil prices also served US geopolitical interests as they created immense financial pressure on Russian and Venezuela in addition to Iran in 2015 and 2016.

The second theory contradicts the first one. It views Saudi traders as the sharpest oil traders on the planet with very long memories. They have played the role of a price enforcer for crude for forty-five years. The glut and subsequent crash hurt them much more than it hurt shale producers. At a time when they needed the cash and could have used it. They have also seen how this specific strategy plays out in 1986 when they tried to push beyond their remit and lost both market share and cash. Given their long term view and their institutional memory they also view shale producers as a temporary blip and would be happy to curtail production and conserve reserves than sell at historical market lows. There were also other ways of settling scores with Iran than setting their own house on fire.

It may not have been a Saudi push that lead to the crash in prices. We won’t know since there are no public records, citable sources or credible references that would provide insights into Saudi thinking from those years. Perhaps it was the inherent complexity of oil markets, the interplay between shale and low prices and a combination of conditions that no one had anticipated and the desperation of other oil producers that led to oil price crash of 2015-2016.

Lower prices pushed other producers to pump more, extending the supply glut for two years. More importantly shale producers refused to die or ride away into the sunset. They didn’t just survive the price crash; they came back as leaner, meaner, hungrier and more efficient versions of the original model. Only the strongest survived, the weaker ones were weeded out. Pushed in the corner by falling prices they found ways to cut costs, focus on tier one fields and make rigs more efficient and profitable.

It took 3 years for the bloodbath in the markets to end. Prices finally climbed over US$ 60 per barrel and managed to stay at that level beginning January 2018. The war in Yemen and the spat between Saudi Arabia, UAE and Qatar in August 2017 increased tensions in the GCC. Press and banking research teams used the crisis to talk up prices. US change in stance on Iranian sanctions further buoyed oil markets. There was broad consensus that removal of Iranian oil from supply side will create gaps that other producers will not be able to fill quickly.

All this was a year ago. Crude oil prices (WTI) touched US$77 on 27th July 2018 but couldn’t break through that level. They started trending lower in October 2018 as it became apparent that a number of large crude customers would get US waivers from Iranian sanctions. Prices hit new lows in the last week of December 2018 with WTI trading at $45 a barrel and Brent heading towards the low 50s. January and July have historically been good months for rebounds. 2019 has been no different. There has been a clear price reversal in January but the question on every one’s mind is will it hold?

How about the future?

What have we learnt so far?

We should continue to see steady increases on supply side. Resolution of oil pipeline capacity issues across fields in US and Canada will bring in more oil at lower prices and lower breakeven points.

Marginal improvements in operating efficiencies across power consumption devices, industrial users and consumers are likely to ease pressure on demand. Given planned emission cuts we see energy efficiency improve for new models of automobiles, trucks, power generators, air-conditioners, pumps, compressors and industrial equipment. The improvements are not much but at the expected two percent a year they are enough to offset growth in energy consumption from emerging and frontier markets.

OPEC will continue to cut production but there is a limit to how much supply they can take off the market. Saudis have learnt their lessons well and are willing to make deep cuts to stabilize prices. They also understand the power of signals and now focus their cuts in markets where data shows up first (US customers). But their cuts must be matched and coordinated by Russia and other large OPEC producers. The chances of that happening are slim. With tepid demand OPEC spare capacity will continue to grow. As it grows its shadow will hang over oil prices and markets.

Iranian sanctions and US stance on them, specially the April 2019 expiry of waivers will derive whether oil markets rebalance by end of year 2019. China and India will continue to slow down in 2019. China significantly more so than India. We have started seeing data and signals that indicate that an economic chill is well underway in China. While trade talks between China and US gain momentum and continue to create optimism, the damage on this year demand and growth forecasts is already done. The problem with a Chinese slowdown is the impact is not just limited to China. There are downstream effects across Asia Pacific, Europe and the US as ripples originating from the middle kingdom are felt across the globe.

While 2019 has started off with a strong rebound for oil prices, it is going to be a difficult year for crude oil. 2020 is going to be even tougher. The alternate thesis picking up pace in trading communities is peak demand for energy generated using liquid fuels rather than peak oil. The theory doesn’t have legs as yet but it holds promise.

That’s near term future. Long term the forecast for liquid fuels is even more depressing. The cost of renewable energy sources (aka renewables) continues to fall. Storage remains a challenge but multiple efforts focused on reducing cost, increasing usage cycles and decreasing footprint have begun to yield results. Energy innovation alongside carbon emissions is the brave new world of impact investing. All major forecast models including the ones run by oil majors show the same trend. New energy generation projects in near and long term future are more likely to come from renewable and clean sources rather than liquid fuel.

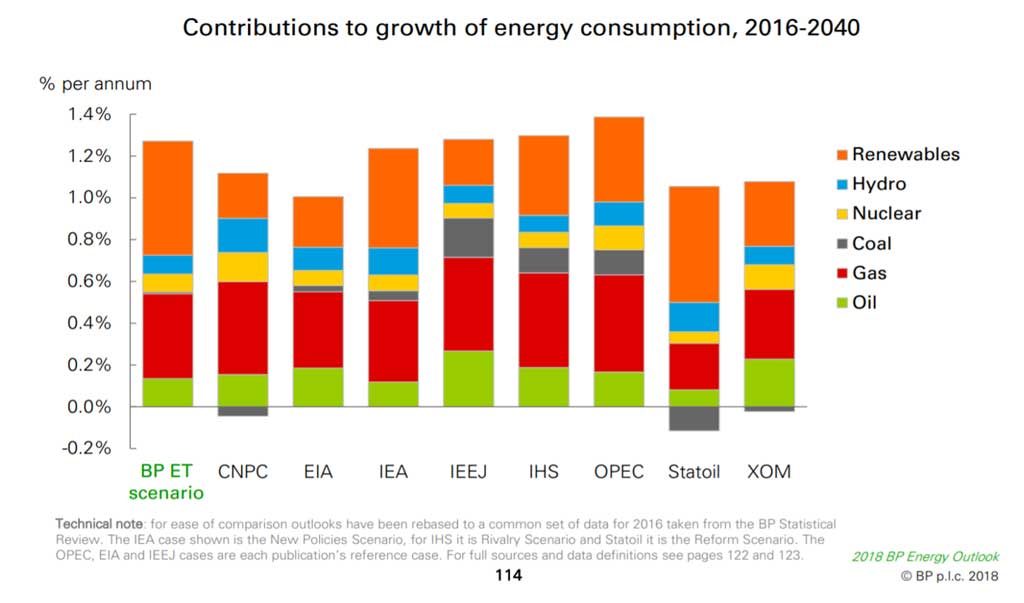

Figure 15. Incremental generation capacity and growth by energy source outlook. 2016-2040. Source BP

Really long term, long term. Despite the positive news renewable still have challenges to work through. We are still a long way off from the brave new world of clean energy. Which is the reason why really bad news for crude oil comes from the realm of science fiction, startups and MIT. A small scale commercial modular fusion reactor demonstration model as early as 2025. A large scale commercial deployment of the same technology by 2035. The names to look out for: Commonwealth Fusion Systems, SPARC, ARC, PSFC (MIT) and Dennis Whyte. Why is this bad news for crude oil? It doesn’t change the energy equation, it rewrites it completely. Net energy gain by harnessing the power of fusion on earth in a reactor bottled up in an ultra-powerful magnetic fields held together by commercially available superconducting materials. Sounds like science fiction, it no longer is. Fusion has long been held as the promised fuel of the future. Contrary to expectations the future appears to be a lot closer than originally estimated.

This is in addition to Terra Power the Bill Gates funded nuclear power plant design that uses depleted uranium rather than its enriched cousin for power generation. A nuclear power plant that runs on the trash produced by conventional nuclear power plants. An initial attempt to put up a functional plant based on the TerraPower design in China by 2022 has run into trade war headwinds but the team is likely to find an alternate site in a more politically acceptable location.

Put it all together and the future for cheaper cleaner energy is closer than we think. We are not there yet and it is too early to celebrate but we do have a clear path in front of us. There is uncertainty about time lines and our eventual arrival. But some of us will get there sooner than others. When they do, they will create a stronger incentive for the world to follow in their footsteps. It is much more than what we had just a decade ago.

Clean energy is not necessarily bad news for crude oil. Liquid fuels have applications and usage outside conventional power generation and transportation. But it certainly is going to cast a shadow on prices when the world figures it out. If you are big oil this creates an interesting dilemma. If you buy into the future vision proposed by CFS and Terra Power, into the theory of peak demand what do you do?

Do you wait for the future to arrive or do you pump and dump now? Depending on who you speak to we are still twenty to thirty years away from the point of absolute certainty. Where some version of our promised future will be realized. However, probabilities will start converging to one within the next 3 to 5 years. That is not a lot of time to get out of way of a hundred years’ worth of momentum.

Take away and conclusions.

We started this discourse with a list of questions. Do we have any answers?

The 20,000 dollars the policy wonks owe me and my father are not coming back. Given the data in front of them, they did the best they could. Their model held together for 10 years. Then the world changed. Given how badly civil servants are rated, they did quite well.

Could we have done anything different as a family? We couldn’t shift or change the national energy mix but we could have taken a second look at our consumption which we did. We could have done more.

You want big oil to pay and suffer as a consumer or an activist, look at energy conservation, efficiency improvements and reducing wastage. Cut down your energy foot print. Run air-conditioning at 27 degrees Celsius, heating at 68 Fahrenheit, share a ride, walk to your next appointment, car pool, recycle your trash and turn down the extra lights.

Forecasting oil prices and energy is difficult. It is difficult to get right whether you do it for a year or for a decade. It is not just supply and demand. Model error grows as you extend your forecast horizon. Not by percentages but by orders of magnitude.

Whatever predictions we have made above are going to be off within the next quarter. That is the typical shelf life. Not just ours. EIA has had to update its prediction of 2019 US production for liquid fuel and natural gas every quarter. If the EIA can’t get US domestic production outlook right, what hope does anyone else has in getting their oil models to behave.

Opinions and outlooks are a function of your baggage and positions. Investment banks and their research team are not going to get it right. They can’t. If you want to understand oil you have to go back to source data, build your own model and do your homework. There are no short cuts. Stop listening to politicians, analysts and breaking news.

Catch up on the debate on carbon emissions. Between developing world and the developed world there is a new line in the sand. If you want to model energy, you have to understand how emissions control is going to shape and change energy consumption in future. Read up on emissions.

Renewables sources as they stand now don’t have all the answers. But they have hope on their side. Storage, cleaner, safer nuclear designs, batteries and fusion are all showing potential. Some of these ideas will start yielding dividends within the next 3 years. Others may take decades. Do we have enough fuel to survive till better alternates are in place? We believe the answer is a qualified yes. We will know for sure within the next 5 years.

Should you be worried? No. Is it worth your while to stay current on energy markets as a consumer? Yes. Shifts in consumption and energy sources in the next decade are going to change the world. Being prepared to meet those changes head on is the smartest thing you can do today for yourself. It may even help you save the 20,000 dollars we missed out on.

References: News articles and commentary

- https://www.reuters.com/article/us-usa-oil-record-markets/texas-shale-challenges-north-sea-crude-as-world-oil-benchmark-idUSKBN1FM0IG

- https://www.theguardian.com/business/2019/jan/05/china-economy-slowdown-us-tariffs-trade-war

- https://www.wsj.com/articles/robotics-company-fuels-concerns-about-china-slowdown-11547230603

- https://medium.com/s/2069/finally-fusion-power-is-about-to-become-a-reality-c6b8b5915cf5

- https://qz.com/1402282/in-search-of-clean-energy-investments-in-nuclear-fusion-startups-are-heating-up/

- https://www.popularmechanics.com/science/energy/a25728221/terrapower-china-bill-gates-trump/

- https://www.forbes.com/sites/judeclemente/2019/01/13/u-s-shale-oil-and-natural-gas-underestimated-its-whole-life/#41f3487d4b59

- https://www.plattsinsight.com/insight/wti-whats-in-a-name/

- https://www.aljazeera.com/news/2018/11/iraq-baghdad-kurds-strike-deal-resume-kirkuk-oil-exports-181116170010040.html

- https://www.cnbc.com/2019/01/07/oil-prices-goldman-sachs-slashes-2019-forecast-amid-oversupply-fears.html

- https://www.cnbc.com/2019/01/13/saudi-energy-minister-on-work-with-oil-producers-to-balance-market.html

Videos

- MIT Breakthrough Energy Technologies, January 2018

- Bill Gates at the Energy Investment Dialogue, Stanford University, December 2018