I have known Shahid Mustafa for 15 years now. We met in 2006 when Shahid was looking for credit and risk scoring solutions as the Chief Risk Officer and co-founder at Tameer Bank. We ran a small pilot for him which marked the beginning of our professional relationship. Over the next decade and a half Shahid and I kept in touch, spoke about future of the financial services industry, crypto currencies, smart phone penetration, explore market opportunities, and exchanged podcasts, books and names of underground music bands.

Shahid is a successful capitalist at work, a socialist at heart but deep inside an engineer dying to try out new ideas to rewire society and businesses in Pakistan. He is a UET Lahore / LUMS Alumni, spent years with Citi in Pakistan and Middle East, moved back to co-found Tameer with Nadeem Hussain and Ali Abbas Sikander and is a well respected banker. His primary focus are retail and SME financing but given his wide interests in reading, he can engage you on philosophy, literature, technology, sufism, qawwali, trade finance and industrial economics.

For the IBA Fintech and Financial Innovation Course, Shahid was the first name on my list of speakers. We had been fellow panelists at 021Disrupt, the CFA Society and a number of other forums and I wanted my students to hear Shahid speak on the state of the banking industry in Pakistan and the future of fintech, neo and challenger banks in Pakistan.

This is an edited transcript of Shahid’s session at the Fintech and Financial Innovation course at IBA delivered on 24th February 2021 in Karachi. Some sentences have been edited for clarity and delivery.

Here is a quick summary of the points Shahid made in the Fintech and Financial Innovation lecture.

a) Banking sector scored card in Pakistan gets an F in service quality and comparison with peer countries and regional competitors. Very little competition or industry driven improvements. Most improvements pushed by regulators.

b) Banks operate a walled garden. Given frictions and issues associated with opening a new bank account, most customers stay put. Even if they move, they would just exchange one set of torturers for another.

c) Fintech businesses are mostly Non Banking Financial Companies in Pakistan. The regulatory landscape is changing rapidly for the better with both SECP and SBP making it easier and faster for new businesses in this space to come forward.

d) There are opportunities in multiple areas. Payment is a just a small part of the eco-system and you generally don’t make money in payments. You use payments as a stepping stone for bigger more profitable businesses.

e) Getting the product right in Pakistan is key. Once you get the product idea right, even weak execution will get you traction. If you could mix a great idea with above average execution, you are likely to do well.

Fintech in Pakistan. The banking sector report card.

A bank is a store and provider of value. It is an institution you can trust to keep your money safe, does not manufacture anything, helps in distributing surplus cash flow.

Obviously at some point in time, in history, there was either a barter system or a coin system based on valuable metals. Now the problem with that system is that the amount of money in circulation is the amount of gold that you have. And if somebody starts hoarding the gold, the economy runs out of tradable instruments which are coins. A big innovation of economics is the banking system with a marginal reserve ratio or fractional reserve banking. Which means, if you have a 100 rupees you deposit in the bank, the bank will keep 10 rupees and lend out 90 rupees. The person who receives 90 rupees, the bank will deposit into his account 90 rupees, and keep 9 rupees, lend out 81 rupees and so on and so forth.

With the multiplier effect, today economic growth has to do with freeing economies from limited money supply. While this is a great thing, it has its downsides. Cycles of recession and mismanagement.

The banking sector does not create any real goods. They are a necessary intermediary between all other commercial entities. If there were no banks, there would be no way to import, no way to export, no way to save, or very difficult to save, very difficult to borrow, and the whole economy would grind to a halt. In 2008, after the financial crisis, banks stopped lending and the US economy ground to a halt.

Post Covid the US economy has not gone into a depression is because they kept printing money. Now one could say the money circulation as a percentage total GDP will lead to inflation, but it has kept the US out of a serious depression. There was a brief recession but they are out of it now. Whether that was the right thing to do or not, only time will tell.

What are non-banking financial companies? Fintech by definition is mostly non-banking businesses.

Insurance companies are financial companies. Micro-finance, leasing companies, payment service operators, payment service providers, asset managers, investment banks or specialized non-banks, SECP regulated, brokerages, modarbas. They all provide services which are not in real goods. They are in financial goods and form a very important part of any economy.

It is a traditionally run sector, which means it is highly regulated. Which means there is not a lot of room for innovation because innovation is not really encouraged. Whereas, in developed markets we see that they have started to loosen up, and by loosen I do not mean increasing risk, I mean looking at things in a different way.

They are allowing, essentially, a breaking down of entire value chain of a finance company into little pieces where specialized players can come in and do something better than incumbent players. Increasing efficiency and improving customer service.

Banks in Pakistan operate a walled garden model. Which means they open accounts, they take deposits, and their main purpose is to ensure deposits do not go anywhere. And because it is difficult to open new bank accounts, they are not really pushed about customer service.

State Bank has been trying to use regulatory methods to improve things and they have improved, but there is very little competition-based improvement. That is not the case in other growing markets. In UK today about 60% of salaries are paid not into regular banks, but in neo-banks. Starling is there, revolute is there, there are many others.

The banking sector legacy players are local, commercial banks, international banks and Islamic banks.

Legacy players II are the DFIs, used to be IDBP, Pak Oman, Pak Kuwait, etc. Specialized banks like SME bank, microfinance banks like Khushali, Telenor, and others.

How do we compare with our peers?

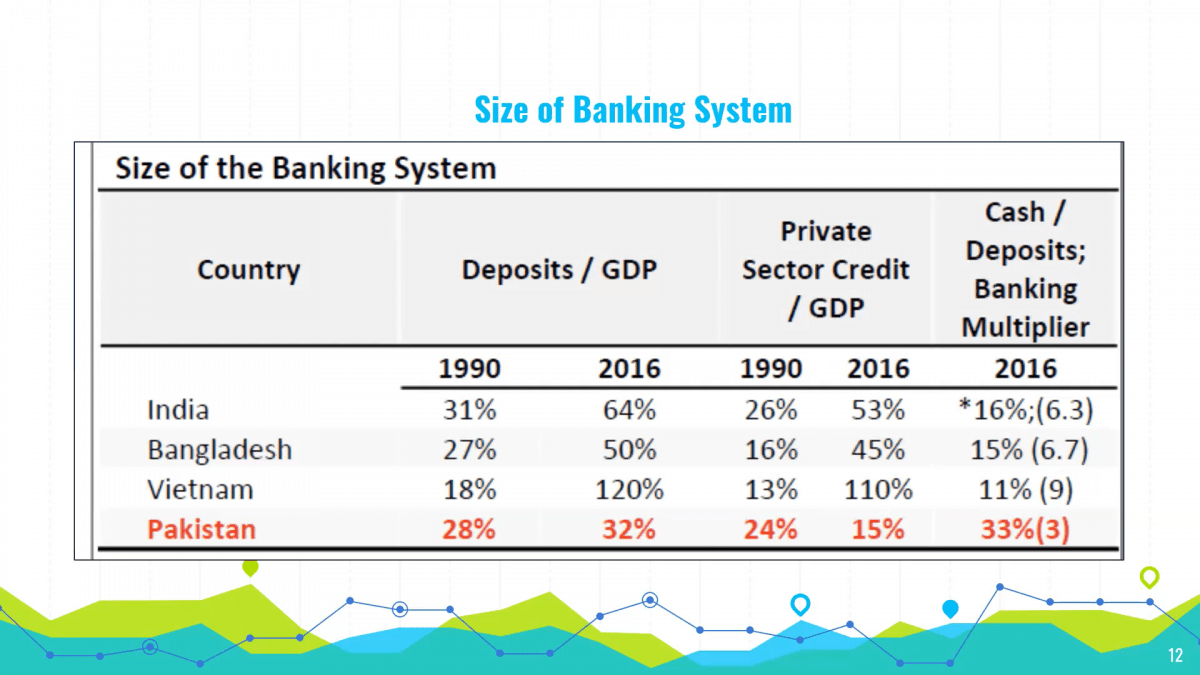

We see our investment over GDP and our domestic saving over GDP are the worst in the region. Our domestic saving, (2016 figures) were 8% of GDP. Compared to India at 30%, Bangladesh at 22%, Vietnam at 29%.

What that means is that, saving deposits are not in the formal economy. They are somewhere else. They are under the mattress, or they are in neighborhood committees.

Similarly, investment over GDP. Once again we are one of the lowest. We are lower than all of our regional partners. We are lower than world average, we are lower than middle income. What that is pointing to is that this system is now working well. It is a broken system.

Deposits over GDP in Pakistan, in 1990 were 28%. This is not savings, this is deposit. These are different things. In 2016, this number was 32%.

You would be well placed to express some pleasure that it has grown in 16 years. But then you look at India which has more than doubled. Bangladesh which has doubled. Vietnam which has grown by a factor of about 8. We can clearly see that Pakistan is behind. We did not ride the wave these countries did.

Another measure is private sector credit/GDP. How much of the GDP is given to the private sector as credit?

India has gone from 26 to 53, Vietnam from 13 to 110. We went from 24% to 15%.

This is because the government is the largest borrower of the banking sector. And it crowds out private borrowing. Government borrows through T-Bills, it borrows through PIBs, and it borrows through other State-owned entities.

Banks lend to agricultural sector, government projects, government programs of buying wheat, sugar, and other intervention programs. Essentially, the state has been using banking sector as its little financier, which is not the case around the world.

The banking sector is mostly used to support industrial or commercial sectors, both government and private, but mostly private. Not used for budget support. In Pakistan the government has been doing this for the most part of the last twenty five years. Everyone has been guilty because this is the easy way out. You don’t increase taxes; you don’t collect taxes and you just go borrow and balance your budget.

Cash/deposits is a multiplier. The higher the cash compared to deposits, the more inefficient the economy is.

India is 16%, it went to below 10% when they demonetized. Bangladesh is 15%, Vietnam is 11%, Pakistan is 33%. So our multiplier is 3. What does the multiplier mean? A multiplier means the lower the cash/deposits, the greater the multiplier, the greater the amount of money available to the banking balance sheet to lend. And if you have a very low multiplier banks don’t have enough money to lend.

Fintech in Pakistan. Trends

What are the trends that we see in the sector?

We see a high level of connectivity. 3G, 4G connections have increased 400% over three years. There is a youth bulge, and 2/3rds of our population is under 30. We are seeing far reaching changes in regulations and opening door for innovation. We see EMI regulation, the PSO PSP regulation, we have now Raast, the small payment gateway. Digital banking license are in the works. We see regulation is trying to catch up to what the world has been doing for the last 5 to 7 years.

By the way for Dawn classifieds was one of the big revenue earners. It’s now gone. It’s finished. Pakwheels completely decimated ads for cars in the newspaper. Zameen.com has destroyed all the ads for housing. Rozee finished the ads for employment. So what I’m trying to tell you here is there is a digital revolution. It is not coming; it is already here. It has affected everything.

But it seems to not have affected banking. Up until now. Now why would that be? Anybody have an idea why we do not see a lot of disruption in banking? We have EasyPaisa, we have JazzCash. They have actually disrupted a lot. But rather than disrupting, they have made a new business model which did not exist. Domestic remittance was completely informal sector which is now finished. It’s all done now on Easypaisa and Jazzcash. But they have not disrupted core banking. Anyone have any idea why?

What you are saying is broadly correct. The word is not restrictions. The word is regulations.

Regulations are designed to protect banks. If banks are protected, they feel no reason to change, because they know regulations are such, there are going to be no new competitors out there to challenge them, to challenge their quality of service. Yes, Easypaisa and Jazzcash cannot send out remittances, but they can receive incoming remittances. The big restrictions on them are because of Mobile wallet (M wallet) structure which is a bank account with limited features and limited throughput. Why is a M wallet a limited bank account less than a regular bank account?

Because it has a very simple KYC (know your customer).

Because it has a simple KYC, it is designed only for small transactions. So you cannot buy a house for 50 million rupees and pay through Easypaisa because Easypaisa accounts, the due diligence was very simple. You have to go to a regular bank which will do the due diligence, ask you for your source of income, and then ensure the payment you’re making is a legitimate payment. Obviously that did not work either as we know that many ‘be-naami’ accounts came up which were supposedly owned by big critical players. So even in regular bank accounts it doesn’t work but where you don’t even have to go to a branch, where you can just use your phone, the chances of misuse are very high. And they were misused a lot until the regulations tightened and new controls came in.

The reason we have not seen a lot of disruption, is because of walled gardens. Nobody is allowed to come in. So they can be as inefficient and as bad at customer service and service quality as they like. The customer do not have an option to go from one bank to another bank. You just change your set of torturers. That’s the way it works. Really poor service.

How big is the market and how is it changing?

Forty banks, 15000 branches, 15000 ATMs, 40 million bank accounts. But 25 million bank customers.

If the population 220 million, that means that customers are less than 10% of the total population. If you say adults are only 150-160 million, 15%, 17-18% adult population has bank accounts.

Compare that with Telecom sector. There are 4 Telcos, 160 million SIMS, 100 million customers, 4 times as large customer base compared to banks. 50 million smartphone users, 50 million feature phone users. Looking at payments, 2 million retail merchants, 200 billion in payments, 35,000 POS devices, 20 million debit cards. But 99% payments are in cash.

This btw is 2019 data set thanks to Omar Moeen Malick at Easy Paisa.

I strongly recommend you go out and download Easypaisa and Jazzcash. Go to an outlet and do your biometric, and try paying on Easypaisa and Jazzcash. Buy airtime, pay your bills. My regular feature is I pay Edhi and Saylani on them because it is the easiest thing to do. The entire time it takes me to pay Edhi is 5 seconds, once you get used to it.

I recently opened a Habib bank account. Habib bank also has an M wallet. I don’t remember what it’s called. Habib has 2 apps. One is their banking app, one is their M wallet app. I wanted to activate my M wallet app, and I downloaded the app and it said please dial this number and we will activate it for you.

First of all, if I have to dial a number to activate my app, it has already failed. I dialed the number, I waited for 20 minutes, nobody picked the phone, and I never went back.

In the digital world, you do not want people dialing a number to fix things. How many times have we called Whatsapp, called their helpline to fix something? Or Facebook, or Twitter? Does it work like that? Nobody is going to pick the phone and wait for 20 minutes for somebody to come and fix something.

Herein lies the apathy of our banking sector.

State Bank of Pakistan introduced the microfinancing license about 15-16 years ago. Before that there were only MFls. Banks and microfinance institutions between them have 8 million borrowers. The entire banking sector of Pakistan other than microfinance has less than one million individual borrowers. The MF sector has 7 million. They are 7 to 8 times the size of all banks put together. And they got here in less than 15 years, while the banking sector has been around since our independence.

Innovative regulations are brought in and have impact. There was a PSO PSP licence which helps payment service operators to come and do their business in an organized manner. There is a new electronic money license which allows essentially whatever Easypaisa does to be done by company without taking a banking license.

There are some caveats, some limitations but it can be done.

Both SECP and state bank introduced sandbox methodology which means there is no regulation for what you want to do you go and they will allow you to do it on a small scale in a sandbox to see how it works and if it makes sense to them then they will make the regulation and allow you to do it.

SECP has reduced capital requirements for non-banking financial companies and non-banking microfinance companies. There is a simplification of process. They have created a secure transaction registry which means that if you are lending to an individual where you cannot register a charge. A charge can only be registered against a company. If you are lending to an individual, you can take a pledge of their house or other assets, but you cannot register charge.

With creation of secure transaction registry, you can have a charge against an individual as well. There is a creation of warehouse and collateral regulations, so we see over the last 5 or 6 years a lot of development in terms of new regulations and it is only when you have new regulations, new ideas can be experimented on and you can try new things.

What is the fintech space? This is the Pakistan fintech space. A big thanks to Planet N for their permission to use this slide. There is a lot on the face of it but the sad part is take all of this and put it on one side and put Easy paisa and Jazz cash on one side they will be 10 times bigger than everybody else put together.

We have fintech but heavily skewed in favor of 2 giant players, these are the 2 gorillas in the room. Until other players come up with models which can scale up it does not bode well for the financial sector.

Both Easypaisa and Jazz cash went to see State Bank to protest about the micro payment gateway, Raast, and said this would destroy our business model and State bank told them, we gave you 10 years of head start, you had 10 years of exclusivity if you have not made a business model that can survive, it is not our fault, it is your fault.

Fintech in Pakistan. The startup ecosystem.

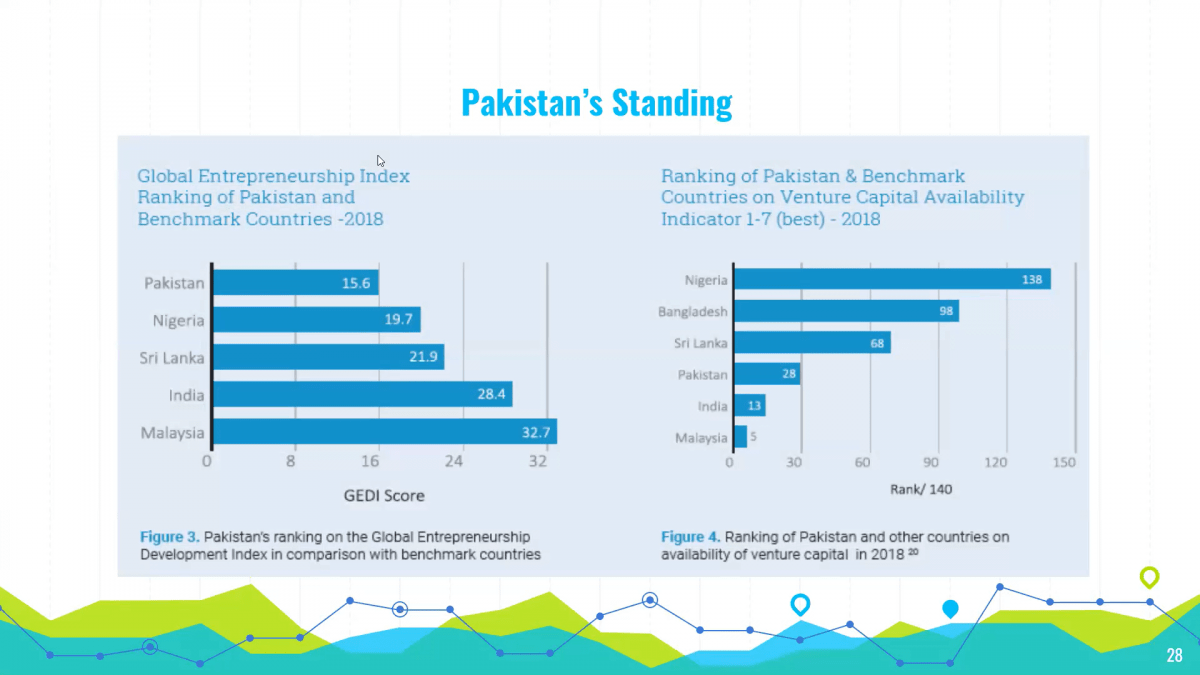

So startups. What are Pakistanis doing in startups. Pakistan is I think one of the most unimpressive start up market in the world today. Now what I am showing here on the left is the global entrepreneurship index. Pakistan is much lower than even Nigeria. We make fun of Nigeria and the corruption there but it’s easier to do business and have a start up in Nigeria, Sri Lanka, India, Malaysia than in Pakistan. Venture capital availability, we see that Pakistan is again low. We rank 28th out of 140.

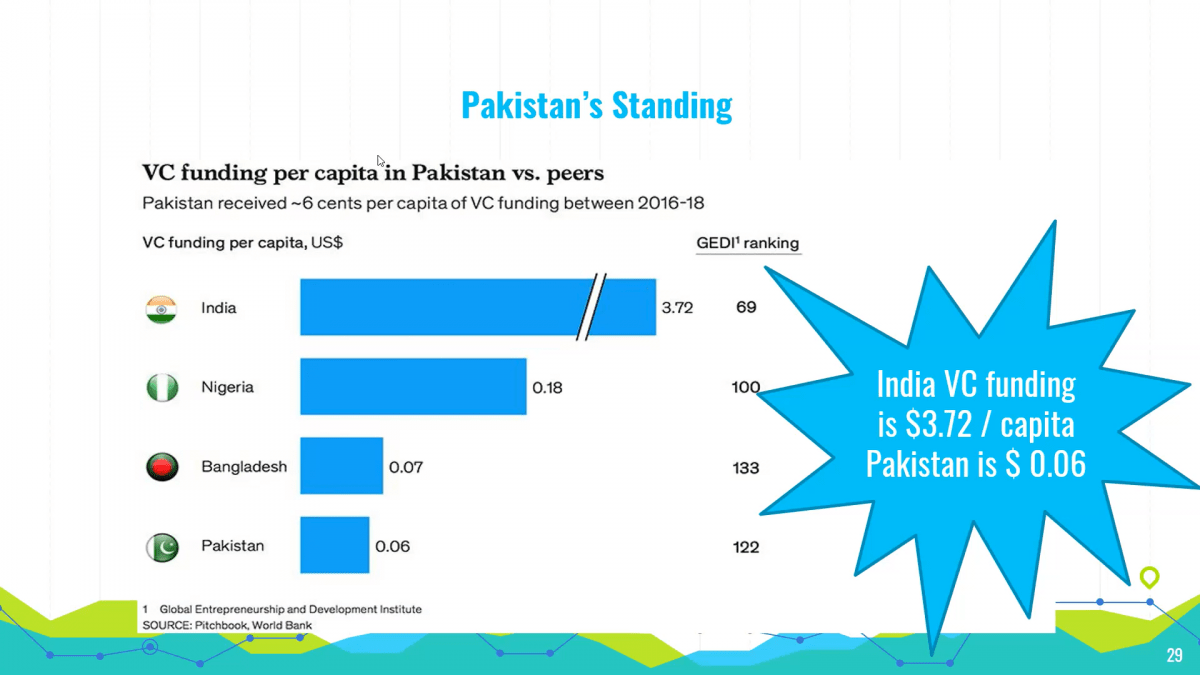

Let’s look at Pakistan standing in terms of venture capital. India raises $3.72 per capita in venture capital. This is I think 2016 to 2018 numbers. In that period, Pakistan raised $0.06, 6 cents per individual.

This is a great place to do business because nobody is doing anything. Whoever does something will be successful.

The 2020 numbers have changed so the numbers have moved significantly. In both cases 16-17-18 were tough years for us. There’s been a lot of movement, a lot of growth, there’s been a lot of uptake especially in 2020 despite the fact that 2020 was a tough year.

I think 2020 was the transformative year and it was transformative because everything was closed nobody could go anywhere and otherwise people just flew to India and gave their money to whoever walked in through the door. India was closed, people had to meet their budgets and a lot of that money came to Pakistan. And the people who came to Pakistan or gave money to Pakistan were very surprised at what they saw here, so in a way covid has been good to Pakistan. Our economy did not shake as much, our exports are all time high, the number of deaths was much lower than India, we did a much better job of handling it so all that is good.

The idea here is not to dwell on the numbers. The idea is to look at the trends. If we had not done anything, then there is a lot to do.

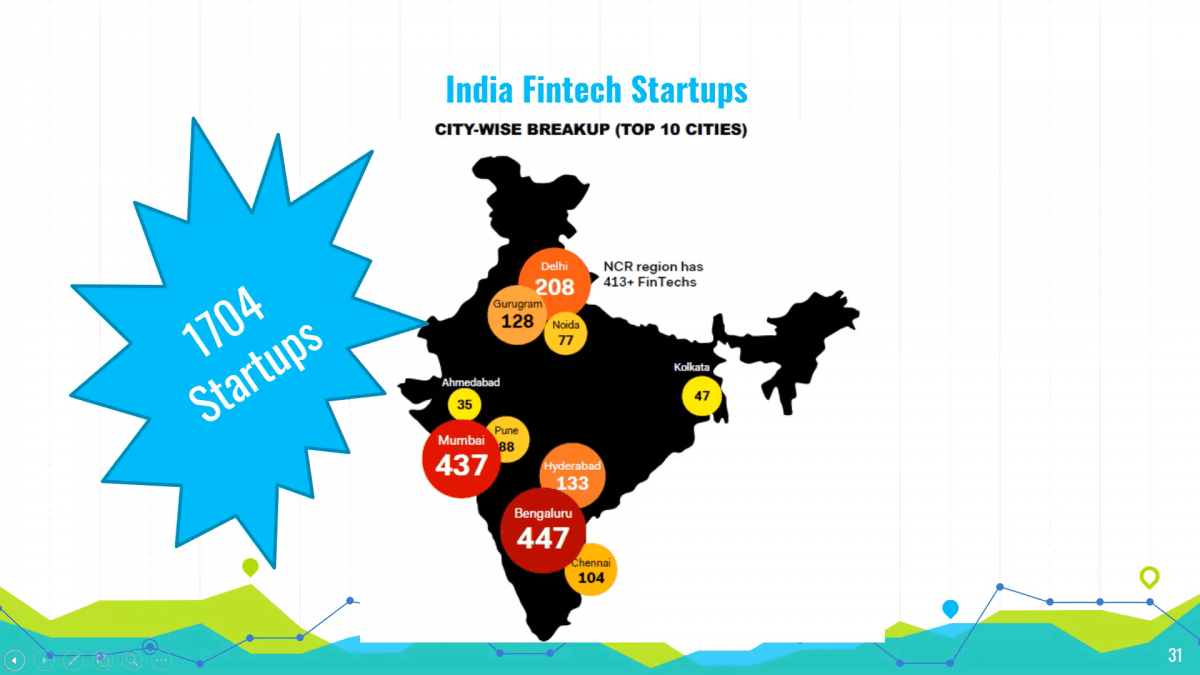

This is India’s fintech start up city wise breakup. Again, I think this is 2018. In 2018, 1704 startups were in India. I think Pakistan you could count them on the fingers of one hand.

The regulator is open to ideas, new regulations are in, much easier to go down the SECP route, even the central bank route is now much easier. There is the sandbox, there is investment available. What is missing is the mindset.

Three broad factors are creating start up conducive business environment. The economy is growing at a rapid pace and a bigger middle class is emerging with more spending. High level of connectivity 3G and 4G. And youth bulge.

A friend of mine, A Norwegian gentleman lived in India for a year and before that he lived in Pakistan for 4 years. When he came back from India, I ask him what what’s the difference. He said in India, the top universities, we cannot hire anybody because nobody wants to work at a job. Everybody want to set up his own start up. In Pakistan we can find the best talent at less than half the price of what we would have to pay in India.

Second, we have a copycat mindset. That’s rather harsh but I would say we have tendencies to have a copycat mindset. Now, copycat is not bad really. Somebody can say, oh by the way easypaisa was a copy of m paisa. And to some degree they will be right because once mpesa has started something that doesn’t mean nobody else can in the world can do that, but anybody who would take the time to look at m paisa and easypaisa in a lot more detail would see that easypaisa when we designed it used a lot of technology and a lot of systems which were not there when mpaisa was made. It was a much more sophisticated platform, and that’s why it has done very well and today easypaisa is more of a inspiration around the world than m paisa is because it built on mpaisa and made a better system.

Unfair investment terms. Unfair investment terms. Many investors who come in and try to work with entrepreneurs try to give them terms which are unfair. This is a deep subject we can talk about off line if anyone to talk about it.

Grit or lack of. If you go to the Bikea guys and Careem guys, they will tell you that there was no 9 to 5. There was 9 to whenever they couldn’t keep their eyes open. Regularly people used to work 7 days a week 12 hours a day.

Another thing, as a nation we have a renter mindset. For those who don’t understand renter mindset is, renter mindset says I have privilege, I need to be paid for my privilege. If anybody has that mindset, they would not be wanting to put their effort they want to be paid for the privilege only and that again does not bode well for whatever venture there working on

And the final one is that sometimes as a nation we are happier at the failure of others than at our own success. If you focus on your own success, I think you will do better in life.

Questions and Answer session with Shahid Mustafa

Jawwad Farid: What is the value of a bank account for the unbanked? Why is there such an emphasis placed on access to banking services for the unbanked?

Number one is safety. In Kenya, 95% of the population have an M paisa account. A daily wage earner would insist to be paid on his M wallet because he is afraid if he takes cash, he may be robbed on the way home. For Eid, there are Muslims in Kenya, when you try to go and buy an animal to sacrifice, nobody will accept cash from you. They all want money to be transferred to their M paisa account. Why? They don’t want to get robbed. Number one, your money is safe.

Two, you are part of formal economy which means that your money earning and usage behavior is recorded which means I can score you and give you credit. When you need money because your mother is ill, or you need to buy a house, the fact that you are a bank account holder means that your entire record of transactions is there and around the world that is what is used to ascertain whether you’re a good credit risk or not. An account helps you save money, allows you to borrow money when you need it. These are the 2 big advantages

Jawwad Farid: When you think in terms of microfinance the 2 big questions that come up in our mind are, you get payment access, you get safety come you get profile, you get scores, you get access to financial services. But what is the cost of that? If lending happens at 25, 30, 35% for that sector, can you really create value with that high cost of financing?

If there was no value, 7 million people would not be borrowing. Why is there value? There are two ways of looking at why there is value.

Number one, what is the alternative? The alternative is the money lender. What rates are money lenders charging? On 120% per annum. So if I’m charging 36% vs charging 120%, obviously this is much better.

Two, this is a formalized sector so unlike the money lender, I will not come after you and break your legs. That is a big advantage.

Three which business gives you a 36% return? Why should somebody borrow when the borrower pays 36% return on capital he or she has borrowed?

Four, people don’t have capital. Because they don’t have capital, all their business models are designed to be high turnover and high margin. So if you go to a corner grocery store (Parchone, Karyana stores), the average margin they earns every time they sell you something, average comes out to about 10%. On certain things like biscuits, confectionery, cosmetics or cleaning products, soaps, shampoo, he’s earning 15, 16, 17%. Milk, bread, eggs he is earning 5 to 7%. Averages out 10%. An average store turns over their inventory twice a month. Earning approximately 20% a month on the amount he has invested. That’s 240% annualized.

Why do you think there is a store on every corner in every city in Pakistan? Because it is an insanely profitable business. It is very difficult to scale up. But on a small scale, it is insanely profitable. And that is why if he is borrowing at 36%, he is still laughing all the way to the bank.

I’ve been involved with microfinance for 12 years. I can tell you that nobody borrows at 36% if they cannot make money, more money than what they have to pay for it.

Jawwad Farid: You have spoken about financial services sector, you’ve spoken about the changing dynamics, you’ve spoken about the shift in mindset as far as regulators are concerned, if you are interested, specifically looking at the banking sector, if you’re setting up a new bank or a challenger bank, right, even microfinancing for that matter, where would you focus? Where is the opportunity? People say that payment ship has sailed in the sense that a lot of players have entered the market and between Jazzcash and Easypaisa who own and dominate that market, so if you want to play the game, what game would you like to play?

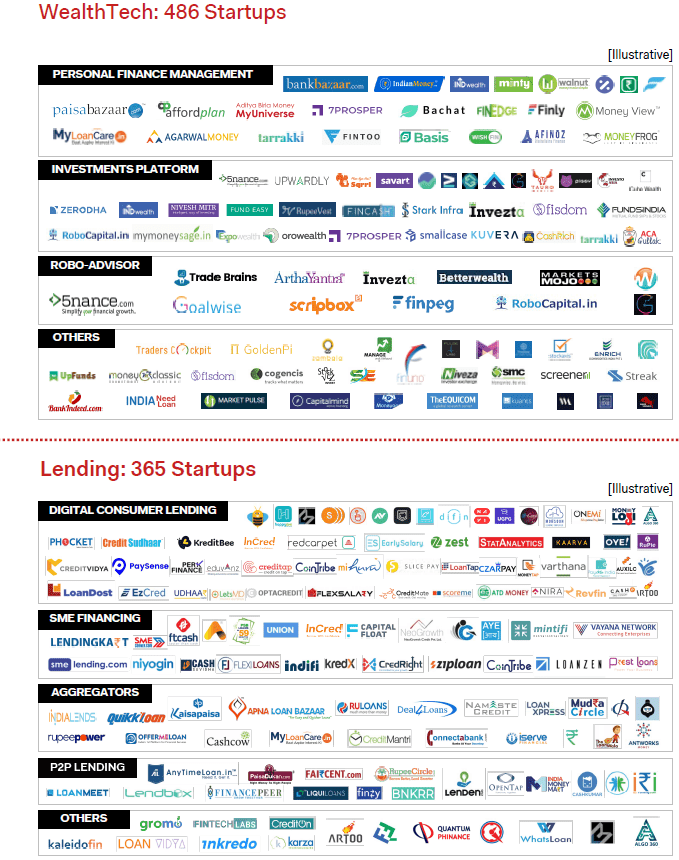

Let me load the India fintech report and I want to share it with all the people here just to show them how big a fintech sector India has and what are they covering.

Payments is a very competitive space, everywhere in the world. Nowhere in the world do payments make money. Payments is always a door opener for something else.

This is a market landscape of India.

486 wealth-tech startups in India. We have personal finance management, we have investment platform, we have robo advisers, we have others, we have digital consumer lending, we have SME financing, we have aggregators, we have P2P lending, and again we have others.

Insure-Tech, 111 startups. Aggregators/policy management, software/white label/infrastructure API’s and others.

Payment is a very small part, a very important part but a very small part of the overall ecosystem. Digital payments. Payment gate ways, bill payments and direct money transfer software/white table/API’s, POS/mobile POS, mobile digital wallets, P2P payments.

Compare this to the Pakistan one, names actually claim to be in this space but there not really doing anything. So there is a lot that can be done. I think insurance is wide open, I think digital lending is wide open. I think robo-advisers, aggregators SME lending, memo lending, all wide open. In a country of 220 million, there is nothing there. It is a desert waiting to bloom.

Jawwad Farid: A question on Easypaisa. Telenor came into the picture and spent a lot of money on promotions, advertising, and you had access to their network, but without that network, without that capital, without that investment in marketing and advertising and brand building, do you think easypaisa would have taken off? If Telenor was not in the picture, would the chapter be written differently?

It would have taken longer for sure. How many of you know of an app called Easyshare? In 2019, there were 70 million active users in Pakistan.

Easy share was an app designed for people who wanted to download something and share it with their friends without using the band way. So in all the little paan shops and cigarette shops in the small cities and villages of the country, content on WhatsApp or whatever would be downloaded by the guy. He would, over Bluetooth, share it with other people for a fee of 5 rupees. So everybody would get their fix of all the memes for 5 rupees. For a long time that was the entertainment hub for the villages in the small towns.

What I am trying to tell you is people find a way when they see an advantage. We had a very difficult time getting the app adopted. But I assure you with domestic remittance over the counter we didn’t have to do anything. It flew off the shelf like it was on fire. And the volume and the growth was just crazy because people wanted to get off the hundi, hawala, bus. This was faster, cheaper, better. So the question is not if you have a lot of money to burn. The question is what is, how good is your idea? How good is your execution? How good is your customer journey? If you do these things well, it will take off. It may not take off in 3 months, it will take 6 months maybe a year but it will take off.

Everything that I’ve seen including easypaisa has had lousy design, lousy customer service, lousy customer experience and still have done well because there is so much demand. The beauty is to do it well. To make the customer experience, I just told you about HBL Konnect, I have never gone back after that first attempt. They lost a customer for life.

Yes, the money helped. But the idea was very strong. The idea would have flown on its own. It may have taken a longer time. Actually I can tell you categorically, and this is categorical. If your idea is weak, if your execution is weak. Our idea was not weak but our execution was very weak. We spent a lot of money and 95% of that money was wasted because our execution was bad and our customer journey was bad.

95% of all the money we spent, every penny, ads, promotions, free giveaways has been a waste. It has not done anything for us. And the reason is that our execution was poor, our design was poor. The idea was strong, but our customer journey was poor, and that is because we were not innovative enough.

Jawwad Farid: So what you’re saying essentially is that, even though the market is dominated by first movers who have a lot of benefits and advantages on their side, if you come up with something that works better, executes well and has a better customer journey, than you will see users shift to that model?

SM: I mean, you had BBM the BlackBerry messenger. It was the de facto message tool. Everybody was on it. Today it is gone. Finished. I can tell you that Easypaisa that is not stronger than BBM, or Kodak or Nokia. Where you come from is not that important to where you’re going. What you do is more important to where you’re going.