In October 2014, a close friend asked me to look at Bitcoin and share an informal opinion on the price data set. That look led to a series of articles that culminated in https://financetrainingcourse.com/education/2014/10/short-visual-history-bitcoin-bubbles/

Yesterday I got a similar ping from a different close friend. What is your Bitcoin outlook for 2021?

You must be a true social hamlet to ignore the meteoric rise in the value of Bitcoin in the last few months and specially the last few weeks. I had not run any numbers recently or taken a deeper look, but my timeline has been overrun by posts indicating that I have missed the trade of a lifetime. To be fair I had been busy with work as well as life goals and hung up my trading shoes in 2012. I have missed trades of a lifetime every year since 2012.

Still, it was about time that I did peek. Here is what I dug up.

Before we go any further, please note that I am an outsider who peeks every few years at Bitcoin out of curiosity. This is not an investment opinion, advise or recommendation to buy or sell an instrument or security. Please do your own diligence and consult approved and licensed investment professionals taking into consideration your financial profile, risk tolerances and investment objectives.

The case for Bitcoin – 2021

What has changed in the last 7 years?

In 2014 when we spoke to my banking and regulator friends, Bitcoin was viewed as an underground tool of anarchy. They did not think regulatory framework would ever accommodate or accept it as a payment or investment standard. The mindset was that if it ever went mainstream, the regulators would step in and shut it down.

2021 perception has changed. Regulation has taken an accommodating stance, though the recent SEC ruling against XRP and Ripple Labs indicates friction that should be expected when the crypto world meets regulatory guidelines.

From the fringes of technology community, Bitcoin has also become significantly more accessible. It has become easier to buy and hold Bitcoin compared to hoops one had to jump through to purchase and transact in earlier years.

But accessibility is a double edge sword. As a wider group of the world population takes ownership of Bitcoin as an asset, regulators are likely to take notice to ensure that the financial interests of their nationals are protected and secured. That can only happen with more regulation, reporting and an increasing burden of compliance.

Bitcoin goes mainstream. The primary case for Bitcoin in 2020 is that the instrument is finally going mainstream. Not just with retail investors. Bitcoin’s hold as a speculative asset class is firmly established and there has been serious flow of institutional funds in recent years into cryptocurrency markets. The instrument has become a credible, respectable, yet risky asset class to hold in small amounts within a portfolio mix. With the increase in central bank balance sheets and the flood of cheap money printed in our first year with Covid-19, increase in Bitcoin prices has served as an interesting and alternate hedge to inflationary pressures.

That is reason number one. Speculative class and alternate inflation hedge. Even if a small percentage of institutional funds finds its way to this market the spiking demand would drive markets crazy. With institutional investors also comes market credibility and a veneer of respect that was clearly missing in 2014.

Counter argument. Institutional money is terribly fickle. It comes and goes with shifts in tides. Remember crude oil in 2008 and then again in 2011-12? While a spike in demand would certainly serve Bitcoin well, an outflow of institutional funds would hurt Bitcoin much more than oil. Oil still had industrial and commercial uses at its price bottom. What would you do with your Bitcoin when cheap money and liquidity driving asset prices up ultimately disappears?

You would hold them as you have held them over the last decade and across prior down cycles. But institutional investors will not. They will book a loss or move on. And if a scandal becomes the basis of a system wide contagion, they will beat each other to the exits to remove the hint of a stain on their balance sheets.

While there has been inflow of funds the big assumption underlying institutional investment is that that flow will grow over time. There are a few reasons why that may not necessarily occur.

The role of the US Government in the last 4 years. The second argument has been the conflict driven stance of the US government in 2019 and 2020 with its trading partners. We received a massive shock to accepted and established norms of trade and engagements under President Trump. Specifically, around trade, intellectual property rights, immigration and diplomatic relations.

President Trump and Covid-19 have been great boosters for Bitcoin. So have chaos and uncertainty unleashed by the combination of the two. Any efforts to undermine the role of the US dollar as the global reserve currency or devalue feed the trend for cryptocurrencies. In that context the wave of global quantitative easing has been the biggest marketing campaign for Bitcoin. Unlike reserve and trade currencies, this asset class has risen higher as national currencies have sunk lower.

Counter argument. The question is if the trend reverses when we take away the drivers.

If the US Presidential transition happens smoothly on 21st January, we expect to see a dip or correction in Bitcoin prices. If they can resolve the ongoing US-China trade dispute or reduce the rhetoric being exchanged, we would expect a further correction. We are not sure how long it takes for the new administration to restore confidence in their ability to act as a market maker of global stability, but it is likely that they will prevail over the next four years. Finally, as the world economy gets back in shape and inflationary pressures raise their head, easing measures by central bank will be replaced by a gradual tightening. Reduction in liquidity should result in reallocation of capital away from speculative asset classes including Bitcoin.

Trader lore: Buy on rumor sell on news. The news is out on 21st of January 2021.

The new speculative class. There is no counter argument against this. Bitcoin clearly represents a new speculative asset class. Of interest to people who would like to make a bet on stability or instability of existing financial instruments. One’s view of Bitcoin should tie in with one’s view of global stability. However just because an instrument is an acceptable speculative asset class, it does not guarantee value or even a floor for that value. You have value if speculators have an interest in trading the class. If that interest disappears or declines, value will also decline. We have seen this again and again with commodities. Oil, silver and gold.

All the above on one side, the fundamental questions around Bitcoin remain unanswered.

Price and value are not necessarily the same thing. Just because something has a price markets are willing to pay for does not mean it also have value.

Trader Lore.

A manufactured asset class reliant on technology infrastructure that represents no real value or use. One could make the same for Gold, an asset class Bitcoin is often compared to.

An asset class that is not tagged, linked or pegged to a real asset in the real world. One can also think of the US dollar in similar fashion but the US dollar has the economic might of the US economy standing behind it. Bitcoin doesn’t.

An artificial limit on supply does not make an asset more valuable. Demand does. While demand has been rising will it continue to rise when a significant correction occurs? And when it does, how bad is the correction likely to be? What kind of an impact would a serious correction have on overall Bitcoin demand and price?

What would be our high-level gut reaction and summary?

There are four primary drivers that have fed the shift in the price of Bitcoin.

- President Trump and stance of his administration in last two years.

- Global instability (Covid-19, Economic downturn, Quantitative easing).

- Speculative Interest, and

- Wider acceptance as a credible asset class.

With the likely reduction in two of the four factors (US elections, some semblance of order restored post arrival and administration of vaccine for Covid-19), we should ideally expect a price correction.

The third factor (speculative interest) is a function of liquidity and money supply. That may begin to get roped in by the time we get to the 4th quarter of 2021. When that happens, the cost of speculative positions will increase, and we will most likely see another correction cycle.

The fourth, wide acceptability is here to stay but demand would primarily be driven by price action in Bitcoin. If the instrument heads towards a sustained decline, we are likely to see a shift in broader holding trends of both retail and institutional investors.

Signals in data. Bitcoin price volatility and trends.

What do historical price trends tell us about what to expect in 2021 with Bitcoin?

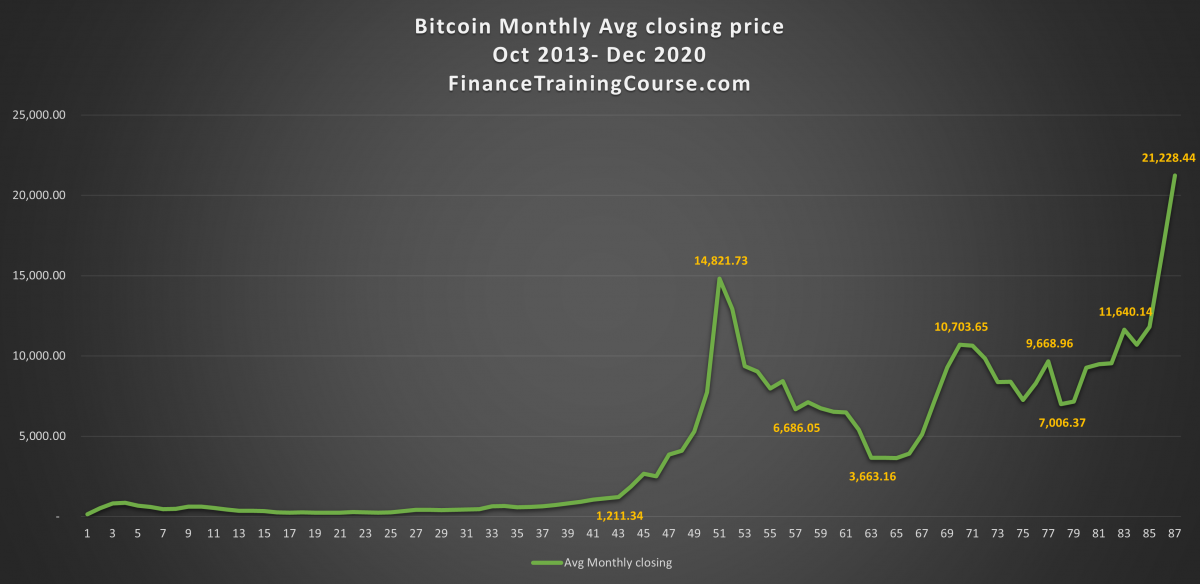

The chart below plots a monthly average of daily closing prices from October 2013 to December 2020. We used a monthly average to dampen down the impact of daily price volatility. The average also helps identify trends that moved up and down across the monthly average rather than daily.

Within the last four years we can identify four major increasing trends followed by a correction. The current rise in prices in December 2020 is the fifth such trend. Will it be followed by a correction? History certainly seems to suggest so.

At the same time in the last 44 months, we can see the monthly average price rise 20 times from US$ 1,211 to US$ 21,228. While corrections are par for the course, the long-term trend across the last four years is clearly upwards and positive.

A natural question is should you buy now or wait for the next dip? Will there be a next dip?

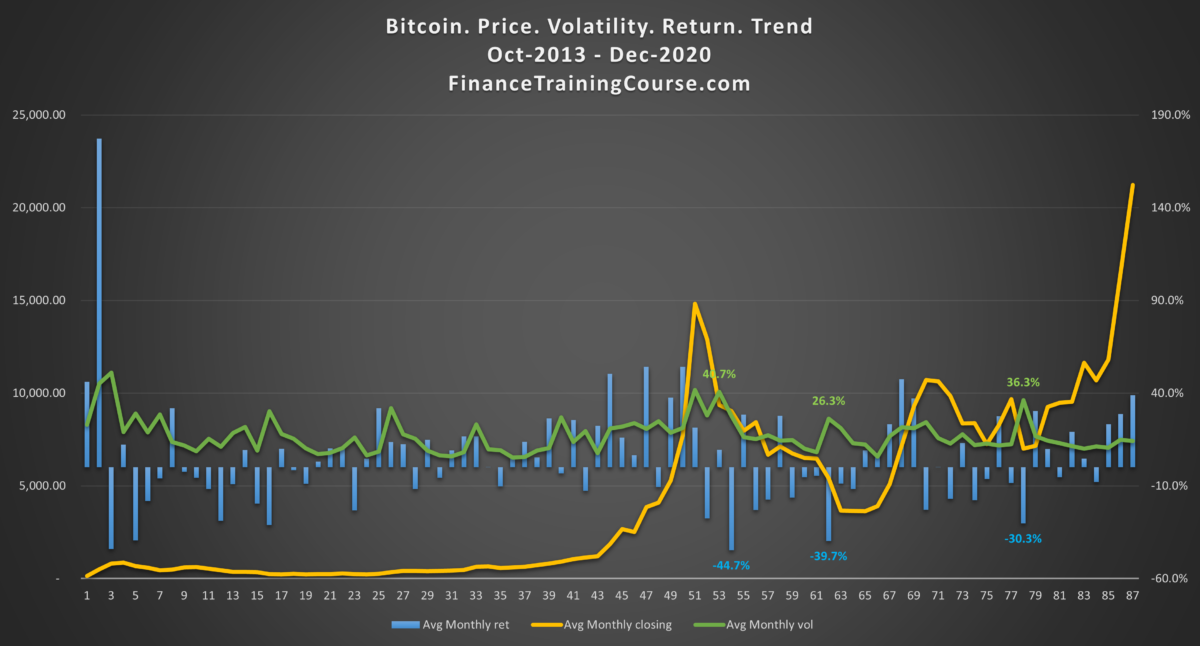

Price volatility or rather the trend in price volatility may help us answer this question. Let us take a quick look. The graph below plots the monthly rolling volatility series (green) against monthly returns (blue bars) versus the price trend line (yellow).

Historically speaking spike in monthly volatility tie in with monthly negative returns. Remember we are dealing with monthly averages to dampen down the impact of daily price movements. Is there an academic framework that supports such a trend? While simulating markets and trends we often observe that assets with higher volatility may generate wider price ranges but often trends downwards.

In the chart above we have marked three such recent instances. If you plot the trend of volatility spike, the spikes occur within 8 to 10 months of each other. The next one is due and may happen within the next one to three months. From a cyclical perspective we know a dip and a correction is coming. We do not know when exactly and how much? An educated guess is within the next 30 to 90 days.

To be sure you could vary the lens and see if the same trend existing in the first 40 months of our data series and you will see that other than one of two exceptions that trend has been consistent over the last 7 years.

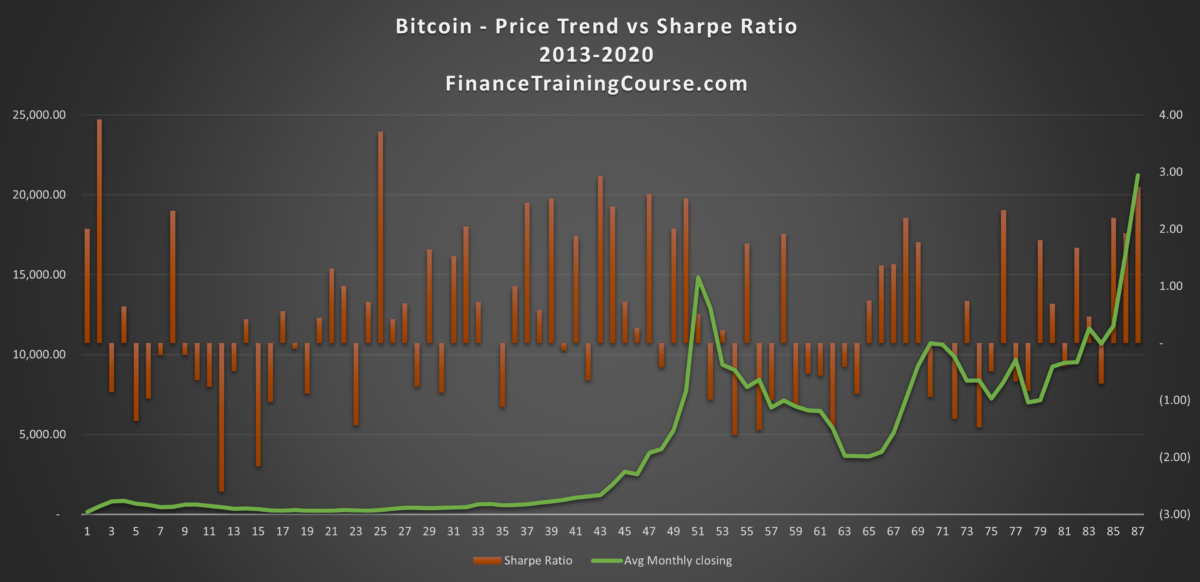

The final signal is the often referenced Sharpe Ratio. Hedge funds chase Sharpe Ratios since they are one input in allocating risk capital and measuring return per unit of risk.

Unlike popular narrative, Hedge funds are fair weather friends. They are in the business to trade on positions, on opportunities to arbitrage and to take positions in alignment with their views. When the views turn out to be not true or are not realized, hedge funds are the first to liquidate their positions. They are neither married to a given asset class or a position. And they are certainly not buy and hold investors. The same holds true for algorithmic trading. The algorithm trades the signal, when the signal turns, the algorithm also turns.

Four years ago Bitcoin Sharpe Ratios were more attractive and consistent than they are are today. But as Sharpe ratios turned negative, open interest, traded value and prices all took a tumble. Like volatility Sharpe Ratios are also cyclical.

Bitcoin outlook – 2021

Ignoring the debate around legitimacy of Bitcoin claim as a valid asset class, what does context and price data analysis tells us?

A correction is likely and is supported by data as well as the context behind the current rise in prices. Outlook indicates timing should be within the next ninety days extending historical trends to the next quarter. I am no longer a betting man but if I had to take a bet I would bet on January 2021.

Should you buy the dip when it occurs? That is a really interesting question. The answer is a function of your view of the world, your risk preference and appetite and your capital base.

Would I? At this stage no. I don’t have capital to spare or allocate. I am more of a hard asset person and prefer to invest in areas where underlying instruments retain value when there is a rush for exits. Remember price and value are not the same. Just because something has a price does not mean it also has value.

Please do remember my upfront pres-qualification. I am an outsider who dabbles with data every now and then. I no longer trade and do not have any exposure to crypto assets. I have just applied traditional risk frameworks from our risk practice to Bitcoin prices and shared the output for discussion. Please feel free to shoot all of it down. But I would love to hear your take on my take whenever you get a chance.

References

- https://www.thewealthadvisor.com/article/dalios-case-against-bitcoin

- https://www.bloomberg.com/features/bitcoin-bulls-bears/

- https://www.forbes.com/sites/ericervin/2020/05/07/the-case-for-cryptocurrency-why-even-the-most-cynical-bitcoin-bear-should-consider-investing-and-how-to-get-started/?sh=18e4cf4f3801

- https://s3.eu-west-2.amazonaws.com/john-pfeffer/An+Investor’s+Take+on+Cryptoassets+v6.pdf