A 90 page study guide on Economic capital written for practitioners by practitioners is now available in store.

Using two detailed case studies the guide walks intermediate and advance users through implementation discussions around Economic Capital.

The first case study focuses on calculating the difference between unexpected loss and expected loss using BIS guidelines. The BIS guidelines are used to showcase the challenges that we face in terms of incorporating the impact of correlations between and across asset classes and implementing EC models.

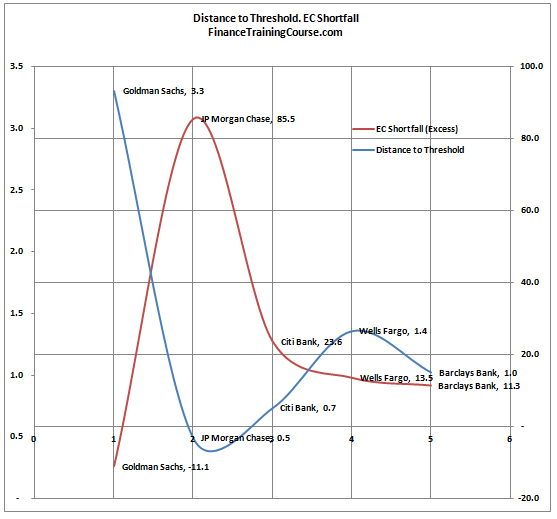

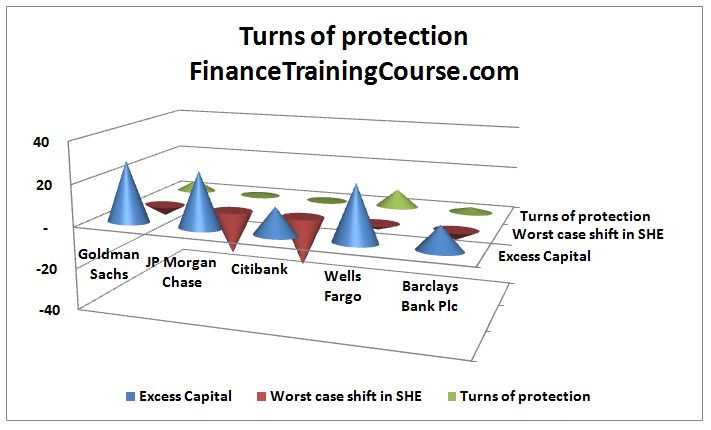

The second case study uses publicly available data set from Goldman, Citi, Wells Fargo, JP Morgan & Barclays. We use the data set to introduce a copula free alternate approach. Rather than use questionable assumptions about relationship the alternate approach only relies on accounting data. Three different variations are presented before we lock down our preferred path. The alternate approach reliance on accounting data makes it implementation simpler and cleaner and simplifies quarter and year end reconciliations.

The accounting data approach does not need a separate correlation model.

For a detailed preview of the alternate approach see the Calculating Economic Capital using accounting data case study. The case study is available for free. The study guide offers a convenient alternate. You can also download the Economic Capital Study Guide – Table of Content.