When we speak of the economic opportunity represented by G-20, MENA, BRICS and Next11 (N-11) countries, fund managers tend to side step Pakistan. The country has had its share of challenges. Political stability, currency devaluations, bad data, security challenges, complex geopolitical hostility on three of its four borders, Pakistan has been an unwilling, quite often an unwitting partner in the great game for 70 years.

Despite these challenges the surprise has been the enormous wealth create by the country’s growing middle class, by three generations of engineering and entrepreneurial talent and the resilience and ease of starting up and doing business in the country. While the official ease of doing business ranking has fluctuated between 89 to 147 depending primarily on the taxation regime in the country, the number of new businesses formally incorporated (private limited companies) with the Security and Exchange commission on a monthly basis have maintained a steady state.

Update: The revised and updated info-graphic with updated middle class figures and other corrections is now available at Pakistan country profile.

The Case for Pakistan – Rising Middle Class

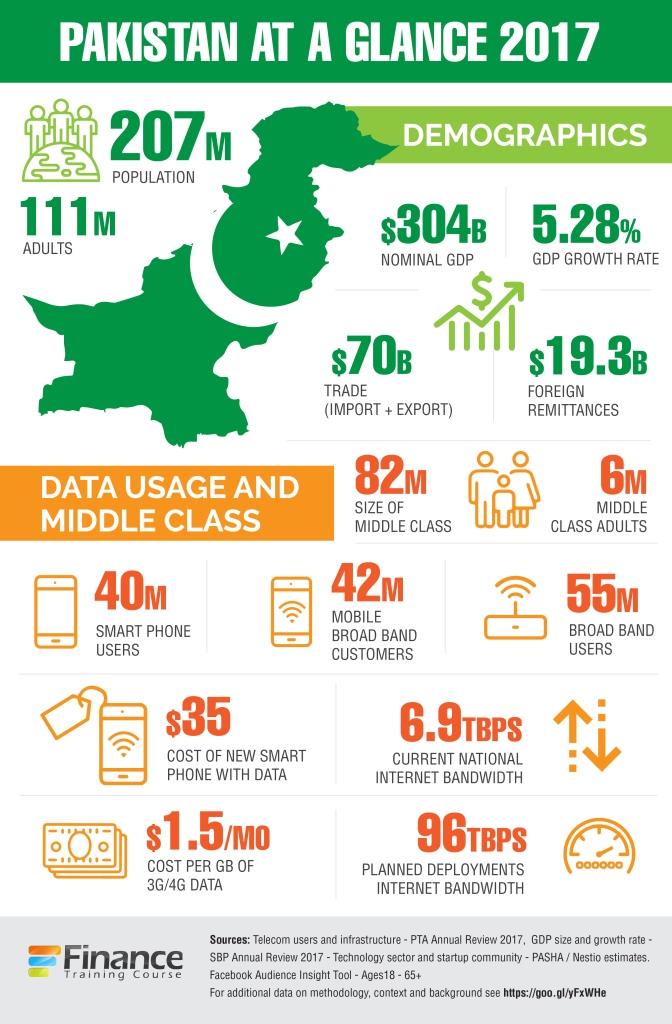

The Pakistan middle class is estimated at 82[1] million (38% of total population) and is the primary driver behind the growth in domestic demand (defined as population segment earning between $4 – $10+ per day per person). Other metrics using house hold appliance and motorcycle ownership, data access and usage trends and income growth place total middle class consumers between 42 – 55 million individuals. The metric is important because it gives a benchmark for size of consumer market and ultimate domestic demand.

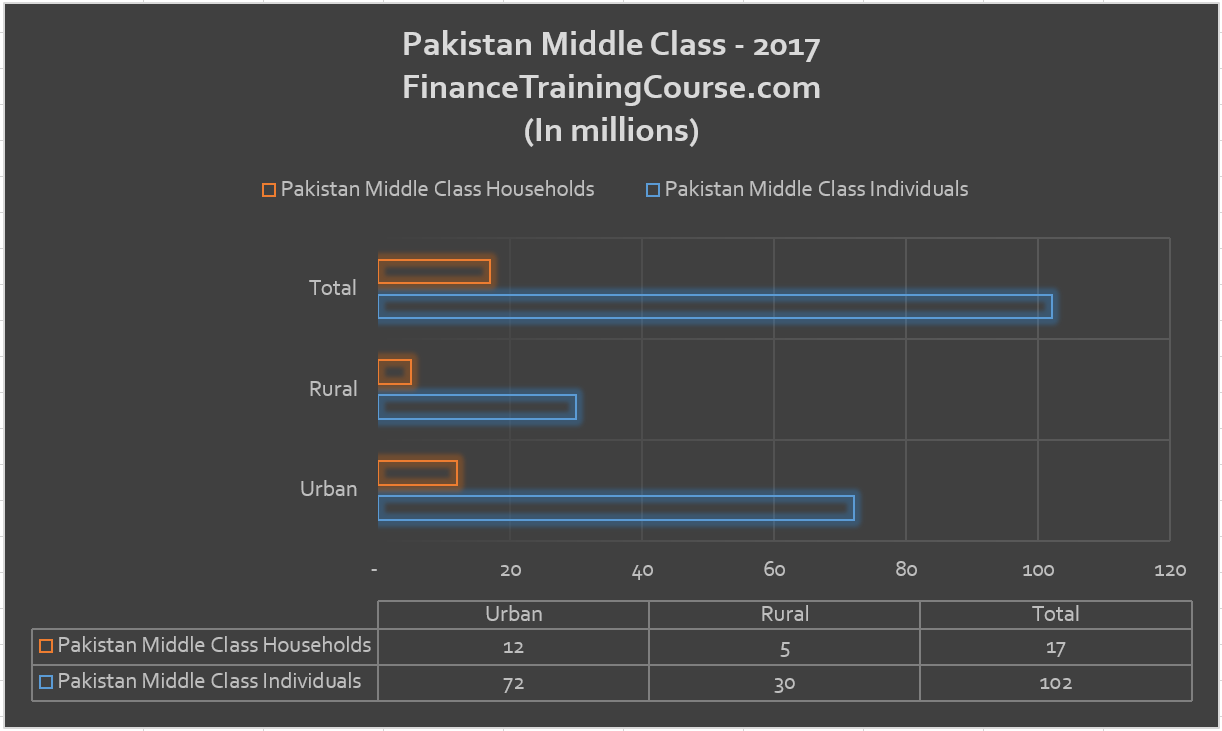

Update: Post the discussion on the original write up, the Middle Class estimates have been reworked using the 2017 census. Please take a look at Pakistan Middle Class estimation challenge for the updated analysis, sources and methods write up. The summary figures are presented below for reference and comparison with the original write up.

Comprising of 7 million households, the middle class of Pakistan represents the 18th largest middle class in the world. Ranked as one of the fastest growing segments as access to technology, education, urbanization and job creation pull more families out of poverty.

To put this in context Pakistan’s middle class represents 6% of the total adult population compared to 3% in India and 1.1% in Bangladesh. From an upward mobility and wealth distribution point of view despite our challenges we have apparently done a better job than two benchmark economies we are often compared with. With a current nominal GDP of USD 304 billion expected to cross USD 400 billion within the next 5 years middle class prosperity, wealth and disposable income is only going to rise in coming years.

To this mix add access to education, connectivity, a responsive ecosystem comfortable with technology, no longer willing to accept transaction or market based frictional costs, returning expats with ideas and capital and families and communities married to the entrepreneurial life style. From logistics to supply chain, from consumer health care to education, from banking and insurance to telecom infrastructure and fashion we are seeing ideas come forth that are side stepping conventional gate keepers and reshaping the local landscape in the image of driven founders and investors.

Pakistani engineers are well known for their creativity, for their healthy disrespect for authority and old school ideas and their tendency to explore and discover workarounds. When you combine this ingenuity with capital and market based products you are really just asking for trouble. There are certainly instances where status quo stakeholders have tried to push back. Refreshingly in every single instance the new kids on the block have resoundingly out played them. In most instances the transition, the push back and the final win happened within a short 12-18 month cycle.

Like every new idea whose time has come, the new entrant domination cycle is reducing with every cycle. Careem, the mobile ride hailing application went from zero to 1.5 million (estimated – see note below) active users in less than 18 months brushing aside challenges by incumbent transport mafia, city administration, municipal transportation codes and competition. If you can consistently create and deliver value, the local market will respond.

The opportunity can be summarized very simply. A US$ 400 billion nation state sized economy will be reshaped by technology in the next 5 – 7 years. The old guard will lose market share, customers and mind share. Technology backed ideas will play a major role in this re-slicing of the economic pie. You can watch from the sidelines or participate and play a role in this great re-slicing exercise.

You can’t ignore 207 million souls nor a market driven by 55 million connected, technology driven consumers across the demographic pyramid.

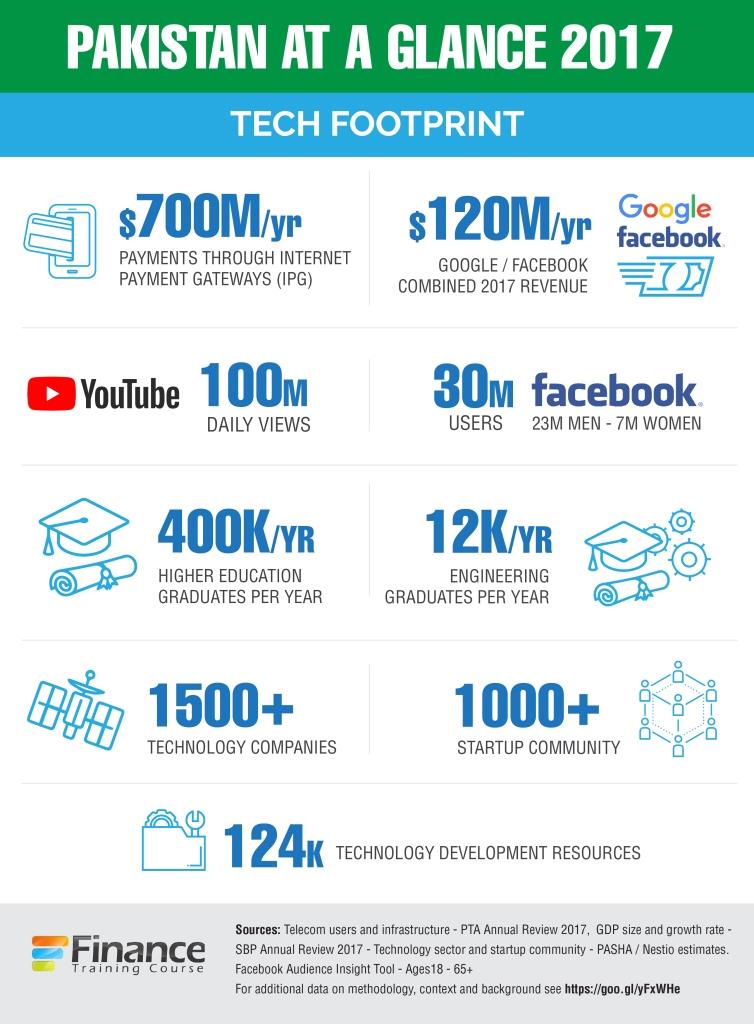

What could the possible upside look like? Here is a recent example. Total gross payments processed through e-commerce platforms (Internet Payment Gateways) in Pakistan are estimated at US$700[2] million for calendar 2017. The estimated figure for 2022, 5 years later is US$ 15 billion. A twenty times increase in volume in 5 years for one facet of the market. Imagine being a player that is already on the ground and participates in that growth spike.

Given the baggage associated with Pakistan risk, it is difficult to trade on this opportunity from the side lines. There are no listed or publicly traded Pakistan tech funds. There is limited interest in bringing such funds to the market. The current traded and listed technology players of Pakistani origin on local and international exchanges are focused on knowledge process outsourcing (kpo), enterprise software (primarily financial services) or call center operations. The only way to trade on this specific opportunity is through partners and fellow investors with local presence, who are comfortable with Pakistan risk, who understand local context and have a history and a track record of identifying, building and scaling up local technology focused businesses.

If you like demographic bets, if you are comfortable with allocating long term capital for hyper growth startups that operate in winner takes all markets, if you describe your style of investing as contrarian value based and if you like the sound of Pakistan risk, please read on. There is much more to this story. There are certainly challenges and speed bumps. But that is what the Pakistan risk premium is for.

In a telling marker that risk premium is also declining. On 29th November Pakistan priced its 5 and 10 year Sukuk bonds at 449 and 352 bps over US treasuries. The dollar denominated US$ 2.5 billion Eurobonds were sold to investors at rates of 5.625% and 6.875% despite recent political turmoil in the Federal capital.

Sources and References – Pakistan Risk

[1]2015-2016-2017 estimates – http://www.riazhaq.com/2015/10/wealth-report-pakistan-middle-class.html

[2] Multiple estimates place this figure between US$ 400 – US$ 900 million. The game of assumptions, Nov 2017 – http://blog.chinookstrategy.com/the-game-of-assumptions-road-to-pakistans-gmv/

3. Middle class debate continued – http://www.riazhaq.com/2017/05/comparing-ownership-of-appliances-and.html

3a. Middle class debate – additional sources – i) https://www.dawn.com/news/1140783 ii) https://www.brecorder.com/2017/10/18/375466/analysing-the-middle-class/ and iii) https://tribune.com.pk/story/1398602/pakistans-middle-class-continues-grow-rapid-pace/

4. Mobile broad band devices include 3G and 4G dongles that are SIM based but are not smart phones.

Pakistan Tech Scene

The Pakistan technology ecosystem is ready for bigger things. There is a steady supply of young teams, founders and ideas. Multiple credible incubators and accelerators are helping ideas get to the next stage in Karachi, Lahore, Islamabad and Peshawar. They do this by helping with initial filtering, idea and market validation, creating a community of support and fast tracking minimum viable products or proof of concepts by incubated teams.

The bandwidth and access to bandwidth problem has been partly resolved by roll out of 4G networks by all major telecom players. There are still issues with connectivity in rural areas but they are over shadowed by 43 million 3G/4G [1]users in the country who now have access to data on the go on their smart phones. They are comfortable using phones to order food, shop for items on a cash on delivery basis, look up directions, book a ride, buy airline tickets, engage on social media and chat.

Founders are now tackling problems and challenges that have both large local markets as well as international applications. The local market is ready for both transformation and disruption. There is a steady flow of ideas, teams and products seeking funding and customers across logistics, food, health, security, appliances, education, entertainment and improving quality of life.

The missing elements are risk capital, expertise in scaling up and going international. There are feet on the ground helping out with all three but they are not enough. We need more.

While some seed capital is available and multiple seed rounds ranging from US$50,000 to US$250,000 have been raised most startups run into a wall by the time they reach series A. There are angel funds focused on seed rounds and there are private equity funds with bite size of US$5M – US$15M but there is nothing in between the US$250k – US$5M bucket. That bucket is the sweet spot for technology funds evaluating Pakistan as a destination for risk capital.

Sources and References – Pakistan Tech Scene

[1] Source Pakistan Telecommunication Authority, July 2017. http://www.pta.gov.pk/index.php?Itemid=599

2. Careem active user estimate – Estimated Pakistan market user base.15% of 10 million android application downloads on Google play store. Discounts and exlcudes iphone users and ios downloads so the actually number may be higher.

3. Pakistani Technology startup list – a data collection project – https://www.startuplist.pk/ . In addition to the startup list, the Nestio receives between 100 – 150 applications for each incubation cycle. That is just one incubator in the city of Karachi. At last count there are at least five active incubators soliciting applications in the same city.

The Nestio is currently receiving applications for 7th batch. That is roughly 700 – 900 applications assuming zero overlap in a single incubator in a single city. When we add Lahore and Islamabad to the mix with similarly active startup ecosystems and startup footprint the actual numbers are likely to be significantly higher than the conservative 1000+ startup estimate. Please note that the definition of startup includes every stage in the startup cycle – not just post revenue.

4. Size of the Pakistani middle class and the outlook on technology community by Yusuf Hussain at IGNITE – https://www.wamda.com/2016/02/pakistans-return-as-the-california-of-asia

5. Google Facebook Pakistan spend estimates – Please see http://blog.chinookstrategy.com/if-only-google-and-facebook-knew-trust-me-they-know-already-the-question-is-do-you-know-what-they-know/. In addition to Faizan’s original post dated May 2017, publicly disclosed, published data available under investor relation sections, central bank statistics and market and industry based metrics can be used to estimate and extrapolate gross spend by both technology giants in the region. There are some educated guesses involved so the actual numbers may be different. Range of error is likely to be plus/minus 10%.

6. YouTube views. Based on marketing, advertising and digital agency pitches to advertising customers in Pakistan to switch from print, television and bill board advertising to digital campaigns. There are some educated guesses involved so the actual numbers may be different. Range of error is likely to be plus/minus 10%. A common regional benchmark for digital properties, media and marketing is Indonesia – YouTube Indonesia daily views estimates in 2012 were 200M views per day. See – https://goo.gl/Aq1Vgm. They are likely to be higher now. For a market with roughly half the digital population, similar demographic footprint and tastes, a number ranging between 90 – 140 million daily views on YouTube is likely. As the size of the pipe and network quality improves, the numbers are likely to increase substantially.

7. Internet bandwidth upgrades – http://www.technologyreview.pk/pakistani-internet-bandwidth-increase-24tbps/ – the 4x upgrade as well as other upgrades in the pipeline – https://timesofislamabad.com/pakistan-internet-system-connected-with-worlds-largest-and-faster-submarine-cable-system/2017/06/29/ – Total capacity as at Nov 2016 adds up to roughly 6.9 tbps. The first upgrade is 24 tbps which increases 2016 bandwidth by 4 times as at Dec 2016. There is 64 tbps in the pipeline scheduled and planned for in the near future. Future is bright for data – not so bright for data prices. But cheap data leads to more usage, more applications, more traction.

Context for startups

We put this together as part of a pitch deck for a Pakistan focused technology investment fund last week. The pitch deck is out there and being presented this week in MENA and Europe. If you would like to be part of that conversation please drop me or Faizan Siddiqi a note.

A number of my friends including the irrepressible Faizan Siddiqi helped put the deck together. The Pakistan Country Profile infographic was put together in less than a few hours by the always amazing, dependable and creative Rumaisa Mughal (website | linkedin | blog ) as a rush request. She is not happy with it but it will have to do given the publishing deadline on this post. If you need someone committed on your team to do dependable rush jobs, Rumaisa is the person for you.

Please feel free to use, cut and past any or all of these information/snapshots as part of your slide deck, your pitches and your presentations. If you could cite the source or give credit that would be appreciated, if you don’t that is also fine.

There is a great deal of interest in the oopportunity that is Pakistan. There is also a perceived shortage of usable, citeable data and we thought we would at least get the conversation started. Much more important that credit is to get the conversation started. If you can contribute to it with data, with opinion pieces, with numbers or even your experience, please do join the debate around the future of the technology community in Pakistan. If you need the high resolution jpegs or PDF for print jobs, please drop me a note, will be happy to email you the zipped files.

For the record, just in case the message didn’t come through clearly in the post above, we are exceedingly bullish on the future – news coverage, anchor opinions and media confusion aside. We have been consistently bullish on the community for over two decades. If anything our wildest estimates have always proved to be significant underestimates when our projected future finally came to be. It’s not just Pakistan’s critic who under estimate this country’s true potential, even its biggest fans tend to miss the mark.

The bottom line, the message is simple. 207 million cannot be dumped in the Arabian sea or the Indian Ocean for that matter. They cannot be ignored or brushed aside. They need to eat, drink, consume, read, learn, entertain, educate and contribute. It all adds up. It has been adding up for the last seven decades.

You may have baggage, biases, blindsides or issues but that should not cloud the commercial opportunity represented by this country and its rising middle class.