Value at Risk is a risk measure that conveniently expresses as a single number the answer to the question “What is your worst case loss, over a certain period of time and given a certain level of probability?” There are a number of methodologies used for calculating the measure such as the Variance Covariance approach, the Historical Simulation approach and the Monte Carlo simulation approach.

What are the prerequisites?

Prior to gaining an understanding of the Value at Risk Concept a useful introduction to understanding risk is our online course:

What topics are covered?

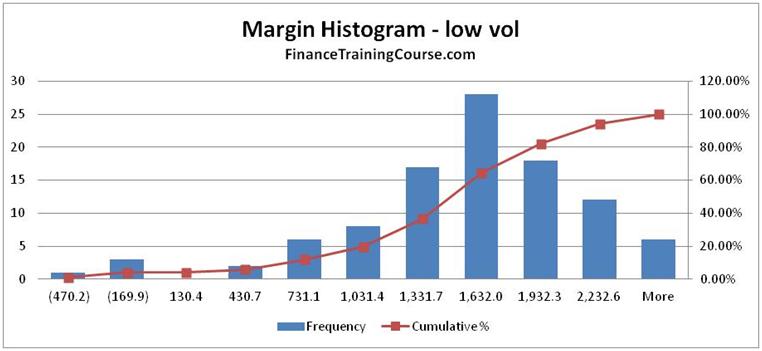

Proceeding from this introduction the following courses review the calculation methodology of Value at risk (VaR) and provide an example of its use as a risk measurement tool via a case study on margin requirements determination for the Oil and Petrochemical Industry:

What are the additional topics I can read up on?

Other applications of the VaR measure are:

- Its incorporation within various Asset Liability Management tools such as in determining the fall in Market Value of Equity,

- In setting market risk and counterparty (PSR) Limits,

- In calibrating Stop Loss Limits, etc.

These are discussed in the following courses:

- The ALM Crash course and survival guide

- Setting Counterparty Limits, Market Risk Limits & Liquidity and Interest Rate Risk Limits

Premium Content

- Calculating Value at Risk (VaR) – Package

- Calculating VaR – Includes case study

- Calculating VaR – EXCEL Example

- Calculating VaR for Futures and Options – EXCEL Example

- Collateral Valuation in Credit Risk Management

- Comparing Value at Risk – Model, Methods and Metrics – EXCEL

- Portfolio Risk Metrics – EXCEL Example

- Portfolio VaR – EXCEL Example

- Setting Counterparty Limits

- Setting Limits – EXCEL Example

- Setting Counterparty Limits – Package

- Sample Counterparty Limit Proposal

- Value at Risk Example for Fixed For Floating Interest Rate Swaps – EXCEL

- Value at Risk with Liquidity Premium

- Value at Risk using the Monte Carlo simulation with Historical Returns approach