Value at Risk (VaR) for Interest Rate Swap (IRS) & Cross Currency Swap (CCS)

3 mins read This post is a continuation of our earlier post that describes the usage of historical simulation for VaR calculation of

3 mins read This post is a continuation of our earlier post that describes the usage of historical simulation for VaR calculation of

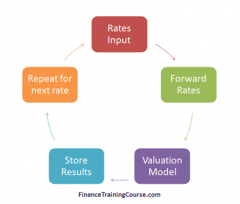

2 mins read Valuing and marking to market over the counter interest rate (IRS) and cross currency swaps (CCS) has always been a