Simulation tools. Variance reduction techniques for option pricing models

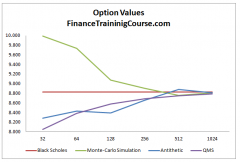

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

4 mins read Variance Reduction tools for Monte Carlo Simulation. Monte Carlo simulation techniques are a useful tool in finance for pricing options

2 mins read Here is the second course on Advance Interest Rate Products. The perquisite for this course is the first course on

3 mins read This road maps focuses on bootstrapping the zero curve and using the zero curve to calculate implied forward interest rates (forward curve). We then used the projected forward rates to price the swap rate for fixed to floating interest rate swap. A separate series of posts build on this material and extend its reach to pricing interest rate caps, interest rate floors, range accrual notes, commodity and equity linked notes.

2 mins read Pricing Interest Rate Swaps (IRS) Here is the first course on pricing interest rate swaps and cross currency swaps divided

2 mins read This course focuses on an alternative method of implementing a two-dimensional binomial tree compared to the traditional method of building

2 mins read Basic Options Trading Strategies The training session covers introductory spreads, straddles, strangles, butterflies and ratio spreads primarily used in option