Crash Course - Package")

Asset Liability Management (ALM) Crash Course - Package

About the Course

The course consists of two pdf files and 7 EXCEL files.

The course begins with a description of how the revenue generation mechanism of a bank works. Asset liability management (ALM) and associated interest rate and liquidity risks are defined. Duration and convexity are calculated for which accompanying EXCEL examples are also provided.

In order to understand the various yield curve shapes, shifts and outlooks, a review of the historical US yield term structures is conducted. This is followed by a look at various ALM strategies, in view of future expected interest rate outlooks, and their impact on the maturity distributions of assets & liabilities of banks.

Next, the various assumptions used in an ALM model are assessed, followed by an explanation of price and rate gaps with some basic illustrations to understand the concepts of net interest income at risk and market value at risk.

ALM reports profile cash flows by maturity or reset buckets. A methodology for building maturity and liquidity profiles for banks’ advances and deposits portfolios using the Pivot table & chart functionality in EXCEL is discussed.

Step by step methodologies for various ALM measurement tools follow. These include Fall in Market Value of Equity, Earnings at Risk, Cost to Close liquidity gap and Cost to Close interest rate gap for which accompanying EXCEL examples are also provided. An overview of other ALM reports such as rate sensitive gap, duration gap, price sensitive gap, net interest income (NII) and liquidity gap is given. Applications for explaining immunization and portfolio dedication are presented.\

An EXCEL Solver based fixed income portfolio optimization model is discussed and scenarios for minimizing duration and maximizing convexity of the portfolio are presented.

A discussion of liquidity risk management measures including ratios and analyses for measuring liquidity risk, limits for managing the risk, general and specific requirements for developing a contingency funding plan and liquidity enhancement tactics for company specific and systemic crisis. A methodology for stress testing liquidity using a Value at Risk (VaR) based approach for a fixed income portfolio is also discussed.

A case study for assessing why bank regulations fail is presented. This simulation results based study looks at the efficacy of Capital Adequacy Ratio (CAR) as an indicator of bank performance and seeks to identify a more valuable leading indicator or target account for monitoring bank performance and health.

The following Annexures are also included as part of the course:

- Value at Risk

- Bond Risk: Calculating Value at Risk (VaR) for Bonds

- A methodology for summarizing retail and SME data

- Glossary of terms

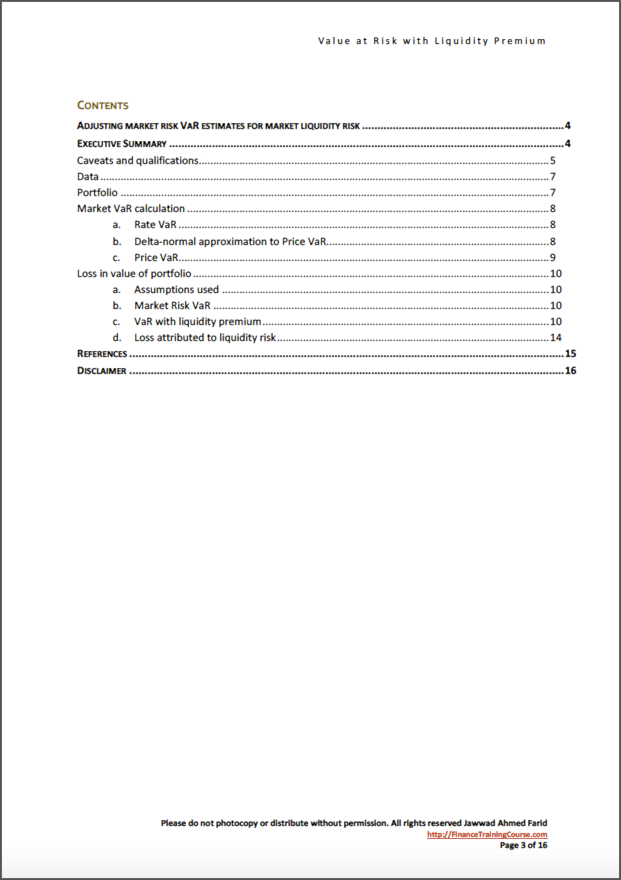

The Value at Risk with Liquidity Premium PDF, presents a VaR based approach for quantifying market liquidity risk with a detailed walkthrough of the accompanying EXCEL example. Market risk measures are calculated for base and stressed scenarios in turn for markets where trading volume is unlimited and where it is constrained. The latter measure produces a metric that is adjusted for market liquidity risk and inclusive of the liquidity premium.

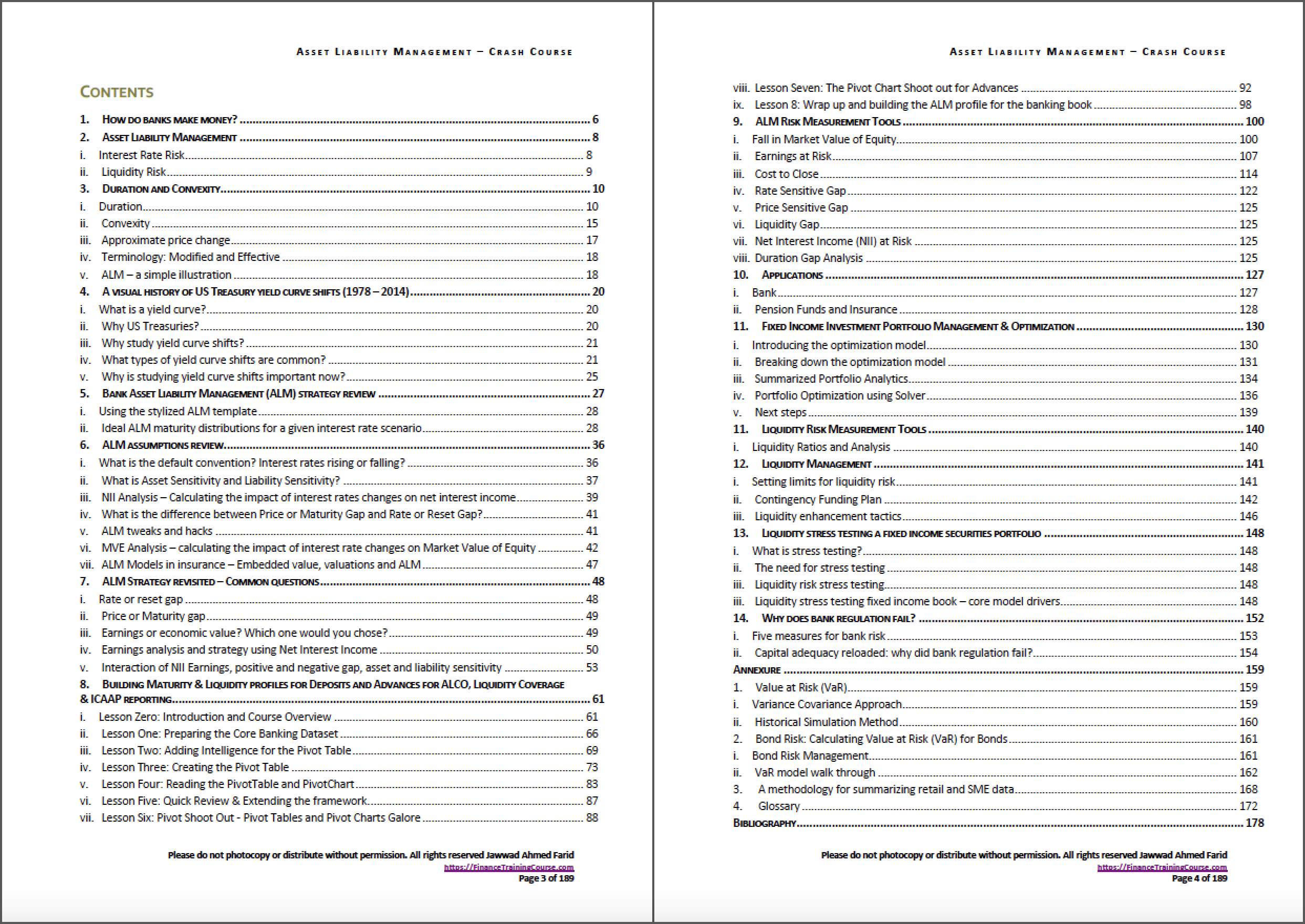

Below is the table of contents from the course PDFs.

Learning Objectives

After taking this course you will be able to:

- Explain the revenue generation mechanism of a bank

- Define Asset Liability management (ALM) and the various risks associated with ALM

- Calculate duration and convexity

- Define some important terminology, concepts and assumptions related to ALM

- Evaluate the various shapes and shifts of the interest rate term structure

- Describe ALM strategies for interest rate outlooks & their impact on asset/liability portfolios

- Build maturity profiles of assets and liabilities in EXCEL for various data dimensions

- Compute the fall in market value of equity due to non-parallel VaR based interest rate shocks

- Evaluate earnings at risk due to non-parallel VaR based interest rate shocks

- Calculate the impact on net interest revenues of adverse movements in interest rates

- Calculate the cost of closing positive gaps indicative of a deficiency of funds by borrowing from the market.

- Calculate a number of other ALM measurement tools and reports rate sensitive, price sensitive, liquidity and duration gaps, & net interest income (NII) report

- Demonstrate some examples of ALM risk and applications of management and measurement tools

- Build a fixed income optimization model in EXCEL

- List liquidity ratios used for measuring and managing liquidity risk

- Describe various limits used to manage liquidity risk

- Discuss the requirements for setting up a contingency funding plan

- State some liquidity enhancement tactics to manage a liquidity crisis situation

- Stress test liquidity for a fixed income portfolio

- Identify a more effective leading indicator for evaluating a bank’s performance & health

- Summarize how to calculate Value at Risk

- Distinguish between Price VaR and Rate VaR

- Pool retail and SME data

- Build a model for stressing market risk for a bond portfolio using various VaR approaches

- Explain an approach for determining the loss attributable to market liquidity risk

- Calculate market liquidity risk under base and stressed market risk scenarios

Prerequisites

The candidate should have familiarity with the calculation of Value-at-Risk (VaR), local markets, portfolio management and the Basel II/III framework. They should also be comfortable with basic mathematics, statistics, probability and EXCEL.

Target Audience

The course is aimed primarily at banking professionals and individuals responsible for asset liability management and risk management within banks, insurance companies and mutual funds who need to review or refresh their understanding of ALM and Capital Adequacy regulations for work, professional review, audit or personal development.