Accounting Crash Course: Small Business Accounting: Cash Book Example

Let’s see everything in action in an example.

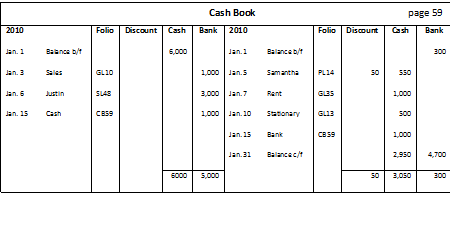

Following are the cash transactions of Alan’s business:

Balances brought forward from last month; cash: $6000 and bank: $300 (credit)

Jan. 3 Cash sales of $1000 paid by cheque.

Jan. 5 Paid $550 cash to Samantha for the inventory bought on credit from her. Samantha allowed a discount of $50.

Jan. 6 Received a cheque from Justin of $3000 for the balance outstanding in his account.

Jan. 7 Paid rent of $1000 in cash.

Jan. 10 Bought office stationary for $500 cash.

Jan. 15 Deposited $1000 cash into bank account.

Let us record these transactions in the cashbook.

Cash Book

Notice we had a bank overdraft at the start of the month. Another important point to note is that we do not record cash sales or cash purchases in the sales and purchases journal, instead we record it in the cashbook and in the relevant account in the general ledger.

For all of these accounts the other part of the entry will be made in the relevant T-accounts that can be found in the relevant books that are indicated by the folio number.

Comments are closed.