In the previous posts we looked at Assets and Liabilities on the Balance Sheet. Finally we complete our balance sheet review by looking at Equity. We then move on to the second financial statement, the Income Statement.

Concept Title: Equity in the Balance Sheet

Description: This concept takes a look on equity and identifies the different equity types

Equity

When you subtract what the firm owes from what the firm owns, something should remain for the original owners of the firm.

We call this net amount equity. This is the portion of the firm that belongs to the original investors / owners of the firm. In other words, if we sold off everything and paid off everything owed to all the creditors, the equity in the firm would go back to the original owners.

A firm’s balance sheet may list equity across a number of headings.

i. Shares

A share is a unit of ownership in a business. It is a claim against future income and net assets. Shares normally have a face value or par value, which may range from pennies all the way to a single dollar.

ii. Authorized Shares

Number of shares a firm is allowed to issue

iii. Issued Shares

Number of shares a firm has already issued

iv. Treasury Shares

Shares that the firm purchased on the open market and kept for its own use on its books. The firm does this for a number of reasons that range from boosting sagging stock price, rewarding investors & purchasing shares for employee stock options

v. Preferred Shares

Preferred shareholders have higher rights over common shareholders. If the first distributes any income, it will first distribute it to preferred shareholders and if anything is left it will distribute the remainder to common shareholders.

vi. Common Stock

Plain equity! There may be different classes of stock that have different voting rights & profit sharing percentages

vii. Retained Earning

Firms generally do not distribute everything they earn to their shareholders as dividends. Instead, the amount remaining from income for a specific year after it pays dividends is reinvested in the business. Every year this amount accumulates and is referred to as retained earnings.

Bankruptcy

When you subtract total liabilities from total assets and if nothing is left or, even worse, if not enough is available to pay off the business’s obligations, the firm is bankrupt. Bankruptcy refers to a state in which the firm cannot cover its obligations by assets on its books.

Concept Title: Income Statement

Description: Examples and explanation of the various titles of accounts present in the income statement

Explanation

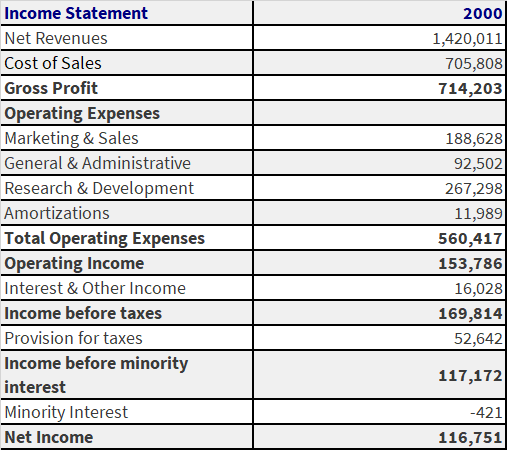

A sample income statement is provided below followed by an explanation of the items present there:

An explanation of the items stated above are provided below:

- Net revenue: The company made 1,420,011 in sales this year.

- Cost of goods: It cost the company 705,808 to make the products that they sold.

- Gross profit: The amount the company made after deducting the cost of goods from the net revenue.

- Operating Expenses: cost of staying in business

- Marketing and sales: the expenses incurred while conducting marketing and sales activities

- General and administration: every company incurs certain expenses in the administrations and day to day running of the business.

- Research and Development: the company spent 267,298 in the research and development of present and future products.

- Amortization: a charge to decrease the value of the company’s assets by a certain realistic amount to distribute costs evenly over the life of the asset

- Total Operating Expense: sum of the individual operating expenses identified

- Operating income: income of company after we deduct total operating expenses from gross profit.

- Income before taxes: Operating income inclusive of interest and other income on which the taxes have not been charged

- Provision for taxes: Amount of income that the firm pays as taxes.

- Income before minority interest: Income after taxes are taken out and before minority interest is paid off.

- Minority interest: the amount payable to the ownership interest that controls less than 50 percent of the company’s stock.

- Net income: income after paying off minority interest. Actual earnings of the company after deduction of all expenses.

Test Problem

1) After dividing part of the profits between the investors, the firm reinvests the remainder into Plucky, Inc. What is the term for this reinvestment?

- Equity

- Retained Earnings

- Treasury Shares

- Common Stock

2) Sama invests $1000 of her cash in her business for hand-painted silk ties. She also contributes her car, market value $10000 to the business. In addition, she takes a loan of $2000. What is her equity?

- $13000

- $12000

- $ 1000

- $11000

3) Raisins, LLC. has the following assets

Furniture $ 40000

Vehicles $ 20000

Factory $200000

Cash in Hand $ 10000

Cash in Bank $ 75000

Marketable Securities $ 50000

What is the total amount of current assets?

- $260000

- $135000

- $85000

- $50000

Exercise

1) Put in a balance sheet with a positive share holder equity and common stock.

Stockholders’ equity:

Common stock; $0.0001 par value;

50,000,000 shares authorized; 34,119,948

and 29,324,370 shares issued and

outstanding in 1998 and 1997, respectively

Additional Paid-in capital 95 128

Accumulated deficit (54) (51)

Total stockholders’ equity 41 77

Total liabilities and stockholders’

Equity 58 88

2) Get the balance sheets from edgar

What were the amounts in the 1999 financial statements for the following items

Net Accounts Receivables

Net Fixed Assets

Long Term Debt

Accounts Payable

Additional Paid in Capital

End of Session Exercise

Go to any one of the following sites

- www.quicken.com

- www.clearstation.com

- www.thestreet.com

- www.marketplayer.com

Look up the following ticker symbols

- SPLS

- ODP

- APOL

- RGA

Comments are closed.