We wrote this piece together as a group as our final submission for our Strategy course led by Ralph Biggadike at Columbia Business School.

At the turn of the century in March 2000 the battle for the online MBA was just heating up. At the forefront was University of Phoenix (APOL) run by a maverick CEO beating numbers, analyst expectations but getting into just as much trouble with regional academic authorities. The University of Phoenix model was part brick and mortar, part online and part convenience for frequent travelers and road warriors who wanted to get an MBA but couldn’t afford to attend classes because of their travel schedule. On the pure online side you had players like Digital Think, which were nothing more than a glorified aggregator with decent funding; companies like Zoologic that had mastered the content, the faculty relationship and the investment banking client niche and then tools and infrastructure providers like blackboard. We wanted to know for sure if the business we were trying to build could be the best of both world, content and technology and the theme of the paper was to see if that was possible in the online MBA world, given what we knew about the core players in this arena. While the financial and numbers are dated and some of the competition no longer exists (including Avicena), the paper should give you a decent overview of the online education space.

Overview

700 Billion dollars are spent on education every year in the US. 220 Billion dollars of these are consumed by post-secondary education. Corporate training budgets account for an additional 60 Billion dollars. Today this sector faces two critical challenges.

The first is technology; the second is resources and capacity. Although technology has been aggressively adapted as a medium and delivery channel, it still hasn’t had its transformational impact on “learning”.

Resources and capacity are interlinked. There are only so many teachers who can teach. This is a function of training, experience, desire, skill set, domain knowledge, entry into the profession and opportunity.

Growth within this industry has been severely constrained by a limited talent pool and commitment on part of candidates to get the requisite credentials. It all boils down to there not being enough teachers to meet the demands placed on the profession. Limited supply of critical manpower leads to capacity problems. Content (defined here as content as well as experience) is expensive to generate, is recycled again and again and is only provided by a handful of suppliers. This in turn gives the content suppliers and the education industry tremendous power when dealing with their respective customers. It also fosters a spirit of co-optition rather than competition between the key players within this industry.

Firms that address either of the two issues have the potential to be market shapers. In recent years a number of new startups have tried to design solutions addressing the technology transformation issue. Avicena is a fairly ambitious startup that plans to focus on solving the resource and capacity problem. It plans on using resources available in offshore markets to solve the content generation problem. It then plans to use innovations in technology and teaching methodology to further leverage its model. In the long run Avicena sees itself as a supplier of processes, content and technology to existing and future players within the education industry, rather than a threat or direct competition.

The challenges that Avicena faces relate primarily to managing growth in a nascent market & managing multicultural mindsets of its various partners and customers (operating from US, Europe, Middle East & South Asia). The success of this venture depends on how well Avicena responds to these challenges.

Our paper focuses on three key issues. Comparative Performance, Competitive Landscape, Competitive Positioning.

Comparative Performance & Valuation

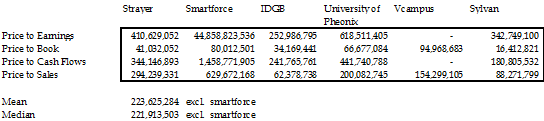

In order to assess the integrity of Avicena’s financial projections and its valuation we looked at a mix of publicly listed educational ventures. We looked at four very successful firms and two struggling ones. Table 1.0 profiles the sample firms. Exhibit II presents a summary of their financial performance. Broadly speaking Avicena’s numbers are in line with general industry trends. The only exceptions were return on equity and return on asset. We felt these two ratios were artificially high. The reason for this may be the absence of the impact of the planned IPO between the 3rd and the 5th year. Once this adjustment is made the ROE & ROA fall back to more reasonable levels.

Table 1.0

| Firm | Profile |

| Strayer University | A small, high profile, very profitable, regional university that has just begun to roll out its online education products |

| SmartForce PLC | A leading player in the CBT market that has recently finished its transformation to web based learning |

| IDG Books | An excellent executor of program learning in the offline paper based world. We looked at IDG books as the bench mark brick & mortar firm |

| University of Phoenix | One of the very first players in the online education world. High profile, extremely well managed group of educational ventures. University of Phoenix was our online benchmark |

| Virtual Campus | One of the two struggling firms in our sample. V Campus had problems managing growth and profitability. |

| Sylvan Learning | Despite owning a monopolistic and extremely profitable franchise (Prometric), Sylvan today is in serious trouble. |

On the valuation side we used the Price to Earnings, Price to Book, Price to Cash flow and Price to Sales multiples. Firm value was calculated using the terminal year numbers of 2005 from Avicena’s’ projections, then discounted back to January 2000.

The results of valuation are presented below. The numbers indicate Avicena’s value today using the multiple for the firm and the appropriate Avicena numbers. Exhibit (xx) gives the detail of these calculations

The results of valuation are presented below. The numbers indicate Avicena’s value today using the multiple for the firm and the appropriate Avicena numbers. Exhibit (xx) gives the detail of these calculations

Competition

The size of the education market—and its easy adaptability to an electronic environment—promise a bright future for E-Education. As the industry is still young, there are many smaller players in the market, all touting slightly different business models and serving slightly different market segments. Cross-over between models and segments is easily made and as the sprint toward “first to scale” continues, many player in the field will begin converging on what emerges as the most economically-viable business model. Much of the analysis of Avicena’s competitors, therefore, lies in understanding the potential of the businesses as much—or more—than what each is currently offering.

For Avicena, competition occurs across different levels. Content, Process, Technology & Segments. An analysis of Avicena’s five greatest competitive threats follows. With Pensare its segments and content, with U Next its Content and Processes, with Smartforce its Segments, Processes & technology, with Blackboard its technology. University of Phoenix represents an interesting contrast where it can be a complementor as well as competition.

| Pensare.com | |

| Arena:On-line delivery of business education via online communities.Targeting those in the workforce interested in taking business classes as well as higher education institutions who wish to provide courses online.

Technology focus is on online community development. Value addition will come in transmission of licensed content from HBS Press, Wharton, Fuqua as well as individual experts. In addition, the Company provides facilitators for each community to guide the discussions. |

Vehicles: On-line “learning” community technology is developed internally. The goal of the technology is to bridge the gap between the workplace and campus and allow for a free exchange of information amongst students and between individual students and the facilitator, not just the latter.Content for courses obtained by partnering with the top B-schools listed as well as individual subject experts. Content may be customized to a certain degree, probably with regards to which sub-topics to view, and in which order. Both live and recorded course transmissions will be provided. |

| Staging: Supply courses to Duke University StudentsExtend relationship to other universities Extend relationship to corporations Extend offerings to individuals |

Advantages: Alliances with top business schools: Harvard, Wharton, Duke; and industry experts: Anthony Parinello. Adds flexibility by not having to develop all content in house. Big names add instant credibility. |

| Business Economics:Outsourcing content to established institutions of learning and recognized individuals reduces costs of generation.Business model places great deal of value on the “community” aspect of the learning process. The facilitator of the class acts as a guide vs. a lecturer. This requires a certain level of scale, quality and repetitive attendance of the student body. The “stickiness” of the offering must be high. | Challenges:Pensare is dependent upon its content providers in order to expand its scope of offerings. This imbalance may make it difficult to negotiate optimal terms of license renewal and expansion.Barrier to entry is only as great as the strength of the partnerships. A number of companies will be able to develop online communities. The differentiator will be the content and peripheral services. Pensare may be in a weak position of the value chain.

Branding going forward. |

| Smartforce plc | |

| Arena:Provides interactive education software to meet the information technology (IT) education and training needs of businesses. SmartForce provides comprehensive, integrated e-Learning solutions that help businesses deploy knowledge across their extended enterprise of employees, customers, suppliers, and other business partners. |

Vehicles:Smartforce actively develops applications in house as well as acquires other companies who have attractive technologies. For example, Smartforce purchased Learning Productions this month for its advanced, Internet-based role play business simulation software. Smartforce.com’s partner list is a who’s who in Silicon Valley: Intel, Cisco Systems, Netscape, Microsoft, Oracle, Lotus Education, Sybase, SAP, Novell, Informix. |

| Staging:Publishes and markets more than 800 software titles covering a range of client/server, mainframe, Internet, and Intranet technologies.Bulk of this is and was in CBT form. Next step is to transform existing content to the web

Lock in existing customers for future technology and products, so that competition is locked out. |

Advantages:Unlike other companies who are developing relationships with educational organizations, Smartforce started by targeting corporations.This strategy is based upon the belief that corporations have greater purchasing power and need to increase knowledge transfer efficiency than educational institutions. |

| Business Economics:Smartforce is trying to sell its products to corporations by justifying its price with increased efficiencies in training, a major expense within all growing organizations, especially those listed as partners under Vehicles. | Challenges:There is no barrier to entry to this segment of the market. Pricing pressure should become fierce once new suppliers enter the market. Some software providers currently acting as a partner may also become a competitor later if the profit margins are attractive enough. |

| UNext.com | |

| Arena:Corporate clients and individuals who would not otherwise be served. Not MBA degree candidates Newest technology Not professor-centric Not degree programs |

Vehicles:Alliances Controlling processes & standards (over contents providers) |

| Staging:Secured financingRamping up content

Exploring distribution/technology & alliances Roll out of content to target segments |

Advantages: Ivy credentials have established the UNext.com brandColumbia University, Stanford University, The University of Chicago, Carnegie Mellon University, London School of Economics and Political Science Capital markets advantage (pure play, Michael Milken connections) |

| Business Economics:Looking to corporations to foot the billIn large part, corporations already are footing the bill for Ivy-League educations by donating to schools and offering huge salaries which allow high tuition/low financial aid

Still not settled on technology or full implications of cost Separation from professor allows greater scalability and flexibility How superior is Ivy content? Or is the Ivy experience more than class content? E.g. relationship development, special guest discussions, administrative resources. How do you deliver that? |

Challenges:Pricing will be an issue:Expensive to acquire content from branded institutions

Expensive technology acquisitions to support “cutting edge” distribution Contention within the alliance: Branding going forward Within content-providing institutions (what’s in it for the Professors?) Unable to prevent commoditization of on-line education? Unproven management capability |

| University of Phoenix | |

| Arena:Offers both classic-style on-campus courses as well as online courses.Targeting individual, degree candidates.

Current organization customers happy with old technology which is Professor-centric. Attempting to bring their content online to expand their customer pool. |

Vehicles: Mostly through internal growthSome small acquisitions. Content development mostly internal. Will transfer many of its current offerings online. |

| Staging: Customers involved with mortar part of the business.Older player, more established. Technology generation old. No significant initiative to improve dramatically upon it. Scaling up reach and on ground facilities |

Advantages: Generates own content.Digital & Physical Distribution True click and mortar |

| Business Economics: Entrenched, first mover for individual, degreed educationStill – to some extent – an old economy player. High level of fixed assets made up of numerous campuses. Bricks and accreditation gives the ability to price according to a traditional “classroom” setting, discounted. Serving an otherwise un/under-served population. Ability to utilize older, established technology which will keep R&D costs down. |

Challenges: Relative ease of entry into the space for those who have access to content.And there is A LOT of educational content out there. Players currently playing in the corporate/branded arena may decide to move into the individual market. The old technology must finally be upgraded at HUGE cost. At that point, will have to move further into the capital markets which discounts bricks and mortar. |

| Blackboard.com | |

| Arena:Targets education providers who wish to launch and grow online teaching environments.Provides a platform for education content transmission Product allows institutions to move campus based courses online Provides consulting services to assist clients in using products and making the transition online. |

Vehicles:Partnered with PeopleSoft and Datatel to deliver open solutions. Aligned with EDUCAUSE IMS initiative which defines Internet architecture for learning Planning to work with Sun Microsystems to make online content affordable for K-12 schools The Company is one of two companies designated a Tier One partner for online learning by Microsoft. |

| Staging:Currently working with 1,600 colleges, universities, K-12 schools, in more than 70 countries.Hosts over 12,000 individual courses with 100,000 registered users.

Adding ~ 40 new institutions for its software business each month Revenue growth of more than 300% year-to-year Planning on working with Kaplan, Princeton Review, Caliber and others to help them bring their content and brands online. |

Advantages:Deciding to not compete in the content portion of the value chain, BlackBoard instead is striving to become the standard platform for content transmission. This focus may help it to succeed while others who may try to develop both transmission and content may dilute their resources.Combining a consulting service with its product offerings uses the standard IT software implementation model. It may accelerate adoption of its products by attracting customers who are techno-phobic. |

| Business Economics:In the short term, revenue growth should continue to be substantial as more and more educational institutions move online. However, unless there is proprietary technology, there seems to be little barrier to entry to provide a similar service.Blackboard offers an “open solutions” implying that it will be able to integrate with existing systems. This can work against them because it also allows competitors to develop systems which are compatible and may replace BlackBoard systems. | Challenges:Being able to become the transmission standard for the educational insitutions is key. They need to become the Netscape, AutoCad, and Windows of educational content transmission. Even if they achieve their goal of becoming the platform, they may find it a difficult position to defend. |

Given this competitive landscape, what is the optimal positioning for Avicena? Their business plan focuses on generating content offshore, rolling it out to select segments in the US and then extending their product offerings as well as customer base. However if established and well financed firms have already staked their individual claims on financial content, content generating processes, content storage technology & premium segments how can Avicena find gaps that it can claim its own?

Value Chain Analysis

How can we answer the above questions? We looked at Value Chain Analysis for some clues. We felt that an understanding of the value chain would help our strategic analysis because of the following reasons

It lays out the terrain on which the firm will face its competition

It indicates areas and direction where the “higher ground lies”

It identifies components of the chain where a little effort can create tremendous value

It helps in identifying core competencies and segments of the industry the firm should mark as its own

The exhibits at the end of this paper present the analysis. A summary of key results is presented below

Competitive Edge

Avicena’s biggest edge is in its ability to create, manage, drive and retain an outstanding team of professionals in the Middle East. The team is created from a huge pool of manpower available in South Asia

Avicena’s offshore team, its access to the resource pool, its technology and its processes allow it to work with a cost structure that cannot be replicated in the US. Although the cost advantage is transitory, the product / content created during the transition phase are not. As long as the initial products sell, the cost advantage will remain on Avicena’s books.

Value Creation

Avicena can create tremendous value focusing on five low complexity activities that capture 40% of the value within the value chain. These are: Knowledge management technology, selection of course subjects, selection of human resources, standards & guidelines & knowledge synthesis process.

Components like editorials & communications, quality assurance, manpower training, market research & need analysis also create value but are commodity services. Avicena has the option of retaining them inhouse, but if the need arises can easily shed them

Defensibility

Once again the most defensible and the most value creating component is the retention & sustainability of the offshore team. This is Avicena’s unfair advantage and its “higher ground”. As long as the firm focuses on getting this bit right, they will be unbeatable

The least defensible components are the standards, the processes & editorial capability.

Competitive Positioning

Once again we return to the competitive positioning question. What is the optimal positioning for Avicena? Based on the competitive landscape, value chain analysis & our assessment of management & leadership we feel that Avicena should position itself as a complementor to existing and future industry players. This is the same strategy that Blackboard.com is following and given Avicena’s vision for being the industry standard, it is also the right fit. A standard is not one customer or product, it’s a following.

Comments are closed.