Before you begin there are two Black Scholes background posts that you will find useful in deciphering the logic behind N(d1) and N(d2). The first deals with understanding the difference between the two Black Scholes probabilities. The second deals with an intuitive derivative of N(d2). The first is just text. The second has two videos which you will find interesting and that are required reading before you start simulating N(d1) and N(d2) in Excel.

Once you have completed your review, the full Monte Carlo Simulation – N(d1) and N(d2) in Excel training course is now available for free. Add it to your shopping cart and complete the process at zero cost and you will get the details to access the course.

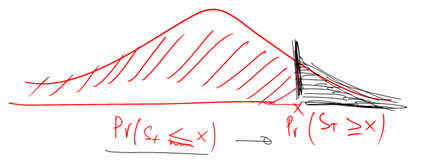

Take a quick look at the three part series that uses Monte Carlo Simulation to show the difference between our two friends from the Black Scholes equation.