Financial Risk Exposure Estimation. Core themes

Welcome to our collection of risk management exposure estimation course lecture transcripts. I teach a week long training course on Financial Risk Management at the SP Jain Campus in Dubai and Singapore. This transcript is an effort to share materials from the course with a broader audience of students across the world. The Financial Risk Management Training Course page is the primary resource where you can download excel spread sheets, high resolution power point slide deck from the class and lecture notes shared with students during the risk management and exposure estimation course.

We are also attempting to share podcasts from the same session and they should be up on a separate podcast page by the end of August. The conversational tone of the lecture has been maintained in the transcript and the pod cast.

Figure 1 Financial Risk Management and Exposure Estimation

Transcript of lecture one.

What is this course about? The traditional, or rather, the academic way of teaching risk is to start off with Value. Some of you asked me about which models do banks use. Values basically come from models. You all have done a course on valuation, right? The valuation course that you did focused on corporate valuations. With respect to both treasury and risk, you are looking at something known as model valuations.

The term and the concept that I am going to throw at you is that there are two prices that you are likely to see. The first price that you see is known as the model price. So for instance, I have a model that runs in Excel or Solaris. This model throws out a price, which is the model’s best estimate of what something is worth. Then there is also something known as the market price.

Figure 2 Risk Management. The Five themes

Risk Management: Market price or Model price?

Now let’s do a quick thought experiment.

I have a model price that says I have some financial instrument or security which is worth USD $ 100.

This financial instrument/security is right now trading in the market at USD $ 150. Let’s call this as Scenario A.

My scenario B is that the same instrument is priced by the model at USD $ 100, and its market price is at USD $ 50.

The challenge that you face in risk management is that almost every single model that you work with breaks. The only time that the model works is when the model price equals the market price. However, this is not something which occurs automatically, but something which you have to work at. Therefore, we use another word known as calibration. We calibrate the model to the market, or rather, we mark the model to the market.

Now, my question to you is, if the model is saying that something is worth $100, but the market is trading it at $150, then, what should we do? You should sell it, right? Similarly, your model is saying that the instrument is worth $100, but the market is saying that its worth $50, then you should buy it,right?

The underlying assumption to this is that your model is right. But what if your model is wrong, and the market is right?

There are temporary instances when the market is in a state of shock and there is a big difference between the market price and the model price. However, ignoring those temporary instances, which may be because of a state of panic or unrealistic bullishness, the biggest challenge that you face is in figuring out when the market is right, and the when the model is right.

As we will see later on this course, occasionally, you will be standing in front of your Board, and your Board will ask you a very simple question: Will you put your neck on the line for your model? How strongly do you believe that this model is right? What is the probability of what your model is saying actually occurring? If they do occur, then how bad can things get, and if they do, then what does your model recommend, and what do you recommend? When this happens, you have to take a call.

Risk Management: Difference between Traders and Risk Managers

The biggest difference between risk managers and traders, or between risk taking and trading, is that risk managers do not like to either take or make a call. They do not like to put their neck on the line, and this is the difference between the theoretical way of risk management and the practical way of risk management. The focus of this course is a mixture of both. We will try to make sure that you understand the models, the reasons why the models, and how to work around them. Some of the books that I listed earlier, especially the Nicholas Naseem Taleb book, Fooled By Randomness, provide essential tools and framework that you would work with.

But then, valuation is also linked to what drives prices. How do you know that your model or the market is wrong? Crude oil has shuttled between the low 80’s to about a $110, and has done this shuttling over the last 60 to 70 days. What is the right price for crude oil? Is it $80,$110,$70, or even $60?

You cannot answer this question until you understand the fundamental drivers in that specific market. One of the things that we have to figure out, although we don’t have time for it, are the key drivers that drive the prices. This is something that will form the foundations of your analysis in the two cases that you are going to look at.

Risk Management: Risk Exposure Estimation Cases

You are going to look at Air Canada, about the impact of oil prices on profitability, and what you should do about it. This is due tomorrow. The second question that you have to answer is GM’s case, in which the question is whether the Canadian Dollar is going to strengthen or weaken with respect to the US Dollar, and what should GM do.

The third piece that this course is about is Risk. One of you asked about the method of measuring it and the tools used for measuring it. Also, how do you report and manage it? One you’ve done these three, i.e. value, price and risk, and you want to reduce your exposure, then you look into what Products are available for you to work with. Since you are not going to run this transaction all by yourself, there will be a counterparty on the other side as well. There is going to be somebody that you’re going to do trade with, and that is where the concept of Limits comes into play; the amount of exposure that you are willing to take to different counterparties.

Here’s a simple example for this. My name is Jawaad, and I have a business that has exposure to the Euro. Nikhil, Priyanka and Gautham work for banks. My overall exposure is of around USD $600 million. So when it comes to hedging, should I just hedge it with Nikhil, or Priyanka or Gautham, or should I split it three-ways? If I split it three-ways, should it be USD $ 200 million with each one of them, or $100/100/400, or $150/150/300? How do I decide on this?

More importantly, when I say that I have this exposure that I am hedging with these guys, if they or any one of them defaults, what is the maximum amount that I am going to lose? So if the Euro plunges by 10 or 15 percent over the next six months, and the exchange rate comes down to 1 Euro to a US Dollar from 1.25 Euro to a US Dollar, on that USD $ 600 million, that’s a movement of around 25 percent. How much of that will I have to put out of my pocket and put in the market? How do I calculate this amount? This is the kind of piece that gets covered in Limits.

In summary, there are five things: Price, Risk, Value, Products and Limits. The LTCM case is about Price and Risk, and also about Value. The Banc One case is about Limits and Risk. The Air Canada and the GM cases are about exposures to risk.

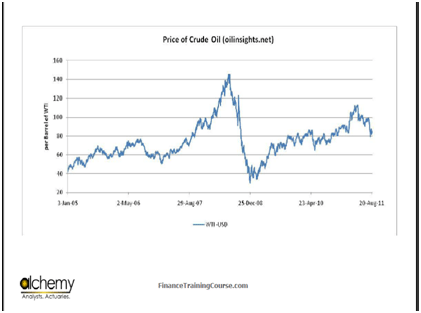

Figure 3 Understanding price. Crude Oil price graph

Risk Management: Understanding Price, volatility and Risk exposures

For most of us, when we speak about pricing, it’s a very one-dimensional statement. What you see in front of you are prices of crude oil. Given the fact that two of the cases that we are working on are set in 2010/2011, the data set that I have used is primarily 2010/2011.

These prices are between January 2005 and August 2011.On the lower side, you have $ 40, $33, $147, &110 and $80. For most of us, pricing comprises of only highs and lows in a single one dimension. When you work as a trader or a risk manager, you add a second dimension, which is a little different.

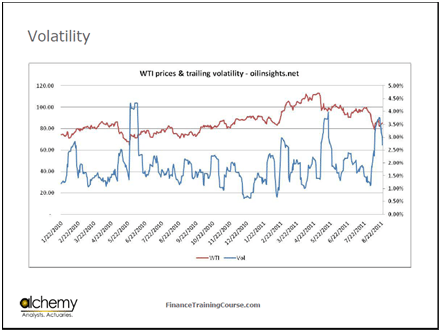

Figure 4 Working with price and volatility. The trading dimensions

One the first graph that I showed you, there was just a price curve. In this graph, I am showing you two things. The time span is now compressed, so its no longer the same graph. My time here starts in 2010 and ends in 2011.

The previous image started in 2005 and ended in 2011. So this curve (highlighted in red) is the price of crude oil. What you see beneath it, the blue line that goes up and down, is something with which you should now be very familiar and comfortable. In simple speak, its standard deviation.

In trader and risk management speak, its volatility. If you take a course on standard deviation, you will pay USD $ 1000 for a seven-day course. If you take a course on volatility, which will essentially be teaching you the same thing, you pay USD $ 10,000 for a one day course. Thus, terminology makes a big difference.

In this case, we have plotted volatility. However, we haven’t plotted volatility for a single day. We have taken a time series for 60 days, and we have calculated a moving average, which is moving over a period of time. Like prices, the moving average also has highs and lows. So in this case, the low is about 0.75 percent, or 75 basis points. On the high side, its around 4.25 percent. SO when I say that the trading volatility is at 4 percent per day, what does that mean? How does that translate into longer time intervals?

So the first question now. Let us say that the price of crude oil is around $80 per barrel. When I say crude oil, I am primarily talking about something called the West Texas Intermediate, or WTI. There is another benchmark that is called Brent, which is sort of a Northern European blend. The WTI is the primary US benchmark, while the Brent is the primary European benchmark.

When you look at Crude Oil as an outsider, you might say that all blends of oil are essentially the same. But oil has different properties. There’s a blend that sweet, and there’s a blend that’s sour. Sweet and sour simply refers to the amount of sulfur in the oil, and the amount of refining that is required. Then there’s also light oil and heavy oil. There are different blends and each blend has its own name.

WTI is a lighter blend, as is the North Sea blend. The Libyan crude is a sweeter blend. The Saudi Arabian Aramco blend has more sulfur. The Iranian heavy is a heavier blend. In Dubai and Abu Dhabi there are two oilfields, Zakum and Marbam which produce slightly different oil blends. Depending on where the oil is produced, it is priced differently.

From a risk management point of view, if you want to get a contract, and you want to hedge that coverage, there are only two blends that are liquid, which means that you can actually trade on them without killing yourself or the market. These two blends are the WTI and the Brent.

WTI produces approximately 425,000 barrels per day. The Saudi Aramco blend produces about 11 million barrels per day. The interesting bit is that the WTI sets the price in the market for everything else. When it comes to risking or managing your exposure, you can only work with the WTI or the Brent and not with the other blends, because those contracts are not liquid at this point in time.

When we say that crude oil trading volatility on a daily basis is about 4 percent, and there are 250 trading days in a year, then what is the annual volatility? How much would you expect prices to move if prices move by standard deviation in a given year? So 4 percent by 250? You would have been right if I had said that this was the expected annual return from crude oil. However, we are looking at standard deviation. If I had said variance, you would still have been right. Sigma is standard deviation and sigma squared is variance. Since variance times 250 gives us the annual return, and you take both of these under the square root sign, you are left with sigma times the square root of 250. Therefore, if I want to calculate one standard deviation impact over the next 12 months or so, it’s going to be 4 percent times the square root of 250. The square root of 250 is around 15. 4 percent times 250 comes down to 4 percent times 15 which is about 60 percent. That is a one standard deviation move, also known as one vol move.

For some of you, this may be a little too fast, as we have done around seven or eight core concepts very quickly and have jumped straight into calculations. But this is a foundational step. Almost everything that we will do will be based on what we have just done. It will be an extension of the same principles. Later on in class if we have time, we will try doing this with our hands using real data. Ghazal has uploaded an excel sheet with data on it. What we are going to do is to play with that data and try and generate these graphs ourselves.

What I have now done is that I have said that square root of 250 into 4 gives me 60 percent, which means that if the price of oil right now is USD $ 80, then, 80 times 60 percent is 48, which means that the change in price is USD $ 80+-48. 80 minus 48 is equal to 32, while 80 plus 48 is equal to 128. Thus, one standard deviation move of oil is between $32 and $128 over the next one year. Whats a two standard deviation move? Plus minus 96.

We are trying to answer two questions.

The first question that we are trying to answer is that oil right now is at $80. How high can it go? If I am an airline, what do I care about?

I care about oil prices going up, one because it has a direct impact on my cost structure, and two because higher oil prices means higher costs, which generally push the economy down and push travel down. If I am an oil refinery, what am I concerned about? Do I care about if prices go up? No, I care about when prices come down. And the reason I care about prices coming down is because as prices go up, my inventory gets marked up, but when my prices go down, my inventory goes down. As my inventory goes down, all the profits that I have booked get reversed. In the long scheme of things everything evens out, but in a shorter market focused point of view, my share price also comes down.

When you work either as a trader or as a risk manager, you have to learn to think in two dimensions. Not just simple one dimensional price, but also volatility.

Furthermore, not just volatility, but about where is volatility now, where is it likely to go, and where will it be over the life of your trade/transaction. This thinking comes to you as you spend more and more time in this field. Your question should be that yes, you understand that historically speaking volatility has been at, for instance, half a percent, but if you are doing a trade and during the life of this trade, volatility goes up to 4 percent, what will be the impact of that move on your pricing, evaluation, risk, exposure, capital requirements, and ultimately on your profitability.

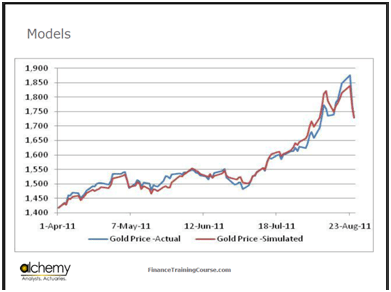

Figure 5 The perfect model for predicting gold prices?

Risk management: Markets and Models and the Relative Value cross check.

The Second graph that you see here shows you the price of gold. There are two lines in the graph, a blue line and a red line. The blue line is the actual price of gold. The red line is the simulated price of gold. You can see that the fit between the two, i.e. the actual market price and the model price is actually quite reasonable. Assuming that I am willing to sell it, would you like to buy this model?

The question that you should always ask yourself is that if Jawwad really has this model and is so good at predicting the price of gold whether it’s coming down or going up, then why is he wasting his time teaching over here?

When you see a perfect fit, you need to ask yourself whether this fit will hold in the future and whether it can be extrapolated. Some of you have taken courses in supply chain management, operations and research etc. You have process simulation models. You have done all of these things that work for conventional mechanical processes.

But a market is a different animal. What holds true in the market last week is not going to hold true for the market tomorrow. This is why the model that you build on historical prices will in most cases diverge from its calibration. In this specific case, the challenge with this model is that there is no broker in the world who will allow you do to a trade effective 12th June 2011 on 24th June 2012.

So even if you knew where prices would be and your model did a good job of fitting it, no broker would allow you go back in the past to trade and make money on it. A broker will only allow you to trade on what we call the hard right edge. The effectiveness of your model depends on how accurate your pricing is on 24th August 2011 and on later dates. In the field of risk, there is a very unhealthy focus on building complex and complicated models, with the perception that if one gets the model right, everything else will follow. This doesn’t work. Just keep this qualification in your mind.

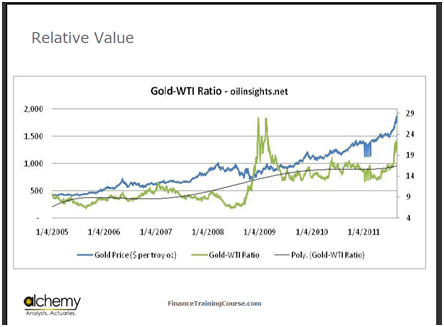

Figure 6 Relative value. The link to grounding yourself

Earlier, I spoke about price, about value, and about how to figure out whether something works together or not. One of the tools that we work on a regular basis, both in the world of risk as well as trading is something called relative value. What you see in front of you are three lines. The blue line is the price of gold. The green line tells us how many barrels of oil an ounce of gold can buy. This ratio, which is known as the oil-to-gold ration or the WTI-to-gold ratio is at about 9 in 2005, and stays around 9 till you hit 2009. In 2009, it jumps from 9 to about 27/28. It then comes down, but does not come down to 9. It is now trading at around 17. What relative value basically says is that if you look at historical relationships, if an ounce of gold could buy you 9 barrels of oil, and if suddenly an ounce of gold is buying you 29 barrels of oil, then something has to be wrong.

This holds true not just for gold and oil, but you could repeat this exercise with anything else. If you run the same numbers with consumables, you can get a good sense of how a specific commodity or security is faring with respect to others. You can also do the same thing with what we call the gold-to-silver ratio. There are times when you need to decide whether the market or the model is right. Relative value is one very quick rule of thumb that you can use to find out how off prices are with respect to other instruments and securities in the space that you deal with.

The question that I am asking myself is that in 2005, I could have bought 10 barrels of oil for one ounce of gold. One of the reasons why you ask this question is that generally, when markets are performing well and the times are stable, you have good proxies.

The US Dollar is a good source of proxy because it is a stable source of value. The Euro too was a stable source of value. Normally you rely on these stable sources of values. However, when these stable sources of values are no longer stable, such as the fluctuations in the value of the Euro over the past two years, what do I do now?

Are there any other alternate sources of value that I can look at to get an idea of where prices are, with respect to both historical norms as well as what they allow me to purchase? Are they priced too high or too low?

Let’s say that tomorrow the world decides that the US Dollar and the Euro no longer exist, and that they will only trade in terms of coins of gold. If you go back to the previous model, you could see how much amount of any commodity would an ounce of gold buy you.

The concept is that unless something dramatically changes, for instance, a new discovery that the consumption of oil decreases the lifespan of all living organisms which would lead to a gradual cut down in oil consumption in the next five years, you should see a stable relationship adjusted for economic growth, consumption etc over a period of time. All that we are saying is that by looking at these trends, we can relatively say whether something is overvalued or undervalued.

When I look at this trend, my opinion is, and my opinion may be wrong, that fundamentally speaking, nothing changed in the world, other than in the world of finance, that supports the movement of the ratio from 9 to 17.Once I have formed this thesis that gold is overvalued, I can question it and dig more information to find out whether it’s true or not.

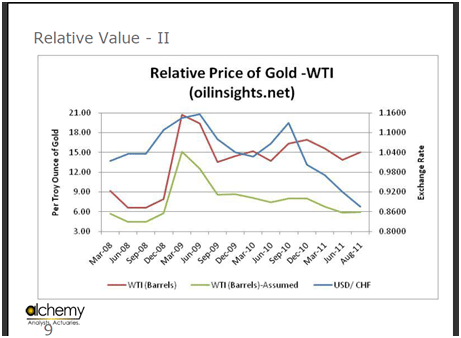

Figure 7 Relative value. Adding currencies to the mix

I am now looking at a currency rather than just oil. In this case, it is the US Dollar/Swiss Franc exchange rate. The red line is the number of WTI barrels of oil that you can buy per ounce of gold. The green line is a simulated model, something which we will talk about later. The blue line is the exchange rate between the US Dollar and the Swiss Franc. You can even extend this further by bringing more commodities into the mix. Again, these are several tools that we are introducing and which we will be constantly using over the next few days as part of our work and analysis.

Risk management. Products and Counterparty Limits

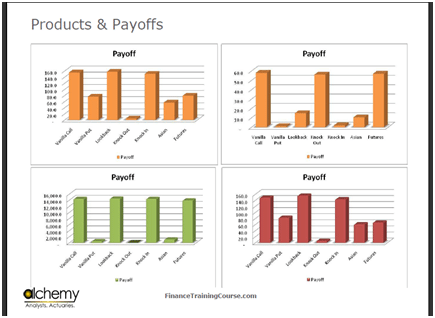

Figure 8 Derivative product payoffs and stress testing

The next thing that we are going to talk about is that each scenario that you see has a product that works for it. I have a handful of products here: vanilla call, vanilla put, lookback, knock out, knock in, Asian and futures. For each of these, I have a different payoff in different scenarios. In each scenario, some products do consistently well, while some products do consistently bad. Which products you pick and choose depends on your exposure, scenario, expectation, and the policy which you have with respect to hedging your exposure. We will briefly do exotics depending on how much time we have. When you will do the LTCM case, you will realize there is a fair bit of coverage of exotics in that.

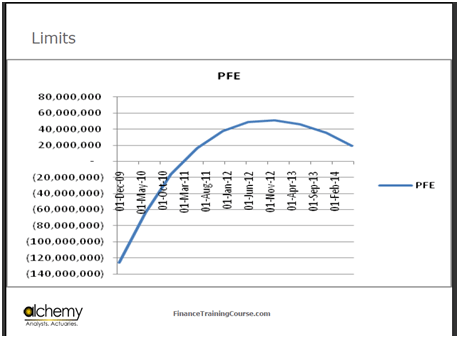

Figure 9 PFE and PSR Counterparty limits

Risk Management: Counterparty Limits and Pre Settlement Risk. Default a simple example

With respect to limits, the example that I have is very simple. I want to hedge Euro 100 million. My exposure is to the US Dollar.

Let’s assume that the Euro right now is at 1.25 to a dollar. For every Euro, I will get $1.25. My exposure in US Dollars is therefore $125 million. My expectation is that the Euro will come down from 1.25 to 1.0.

Under what scenario would I be exposed, and I would want to manage this exposure? Let’s assume that today, I do a contract in which I have sold 1 million barrels of oil at 100 Euro per barrel. The payment for this is due in 60 days. If the exchange rate remains the same, I get USD $125 million. If the exchange rate comes down to 1.0, I will receive only USD $ 100 million. Thus, if the Euro comes down, the amount of dollars that I will receive will be less, and I want to cover this risk.

Now, if the exchange rate goes up to 1.5 from 1.25, I would receive USD $ 150 million. Therefore, I am concerned with the Euro going down because it will reduce the actual amount of cash that I will receive.

Let’s say that I am ADNOC. ADNOC has sold a million barrels of oil to a refinery in Portugal. The refinery in Portugal has committed to pay 100 million Euros in 60 days time. Now, ADNOC does not like the Euro outlook, has already booked USD $ 125 million and wants those dollars at all costs.

What will ADNOC do? ADNOC will come to Harsh, who works for a Bank in Abu Dhabi. Harsh tells them that he has one hundred million Euros coming in 60 days time. So today is the 24th of June, and on the 22nd of August I will receive 100 million Euros.

ADNOC would want to sell these 100 million Euros at an exchange rate of not less than 1.25 in 60 days time, so that at the end of these 60 days, it have USD $ 125 million in its bank account. The bank then says that they are good with it and the deal is done. Now, 60 days later, one of the counterparties, let’s say the bank, defaults and refuses to deliver. Under what conditions would the bank default? Would the bank default if the Euro went up?

The bank will (has an incentive to) default if the Euro comes down to 0.8. What happens to ADNOC? ADNOC now has to sell 100 million Euros at an exchange rate of 0.8, which means that ADNOC will now receive only USD $80 million, while it was expecting USD $125 million. ADNOC then calculates and figures out that its exposure to the counterparty is the difference between 125 and 80 million dollars.

Neither the bank nor ADNOC will default, because they are big names and they don’t carry net exposure. They square and hedge it the minute they write it.

Let us change the scenario. We are not dealing with the bank or with ADNOC anymore.

My name is Jawwad. I have a large contract that will pay me in Euros in 60 days time. I have Sachin as a friend, who is the CFO at another trading company. We decide to cut out the bank from the middle completely. I am going to get Euros; Sachin needs Euros so we decide that when I get the Euros, Sachin will give me the Dollars for them at the agreed exchange rate of 1.25.

60 days down the road, Sachin says that even though he made a deal with me, his boss says that it doesn’t make sense to buy Euros from me at a rate of 1.25 , when the market rate has gone down to 0.80. Now, I have a real problem. That problem is my risk exposure.

In most cases, there is a chain of credit. At the highest tier are financial institutions and banks because they deal directly with us. Then, there are high level corporate counterparties that are very stable and secure.

Further down the chain, you have people who are more sensitive to market changes. That is where the concept of counterparty limit comes into play. Therefore, the two instances that we have looked into, ADNOC and Sachin and Jawaad, are both instances of counterparty credit exposure.

Each counterparty, both ADNOC and the Bank, will assign a limit. One of the principles of risk management which is often ignored is that of concentration. I do not want too much concentrated exposure to a counterparty, but rather, exposure to several counterparties, so that even if one defaults my loss is limited. So if I have a 100 million Euros coming in, I need to ensure that the exposure to my counterparties is within the limits assigned to them. If it is beyond those limits, then I am breaching protocol policy.

In recap, there are five themes: price, risk, limits, value and products. The field of risk is not just limited to risk. It works at the intersection of these five things. If you want to get good at risk, these are the five themes that you need to get good at. When you apply your minds as a group to the four cases that we will do in this course, I want you to keep in mind these five themes. Use these themes as frameworks for asking and answering questions.

Comments are closed.