The new textbook on risk

3 mins read I owe all of you an apology. You must be wondering where in the world have we disappeared to. It’s

3 mins read I owe all of you an apology. You must be wondering where in the world have we disappeared to. It’s

5 mins read We will look at two methods to calculate the value at risk of bonds. There are two common challenges that

4 mins read Value at Risk – Calculating Portfolio VaR for multiple securities with & without VCV Matrix . In an earlier VCV

3 mins read Risk Models, Option Pricing & Bank Regulation training for practitioners A typical MBA program allows a candidate to take a

5 mins read Imagine a board meeting. You have just presented your Value at Risk (VaR) analysis and a board member asks a

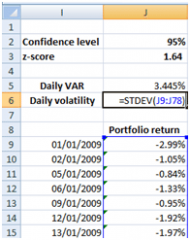

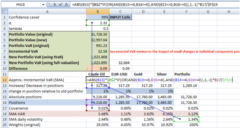

8 mins read Have you ever wondered what Value at Risk (VaR) numbers would look like across the same dataset but using the