Why ALM? This post looks at ALM’s purpose, the principal ways banks make use of it, and its core drivers.

Sources of a bank’s earnings

Banks make money in a variety of ways.

The simplest way is to act as an intermediary on transactions (such as buying and selling foreign exchange, equities, bonds, and other financial securities) and take a small cut on both ends of the transaction (buying and selling). So if we buy or sell 1000 Euros from our bank, it keeps a small margin on the trade which will be added to its foreign currency dealing income. Note that this differs from the income the bank generates by trading in foreign currencies for its account using bank capital (proprietary trading).

The next stream of revenues is a charge on services to customers who are part of the bank’s network. For example, for checks issued and processed, account statements, processing loan applications, pay orders and bank drafts, using the ATM network, paying bills, etc. These items are tagged under the fee income accounting head in the earning section of the bank’s financial statements.

But core banking operations drive the biggest component of a bank’s earnings – the business of borrowing and lending money. Depending on how the bank’s franchise adds value, this third and final head may represent as much as 60% – 80% of the total bank earnings.

Under this head banks make money by borrowing in the short term (through daily, weekly and monthly deposits or interbank borrowing) and lending it out for the long term (via fixed maturity loans to business customers, revolving balances on credit cards or short term personal loans, longer terms auto and mortgage loans to individual customers.)

Since there is a clear difference in rates (the spread) between long term (higher) and short term rates (lower), such a strategy allows a bank to earn an interest rate spread. The source of the spread is the intentional maturity mismatch between assets and liabilities. In order to benefit from the maturity mismatch, the bank assumes that:

- The spread between long and short term rates will remain positive over the duration of the borrowing and lending terms.

- They will be able to rollover (renew) their short term deposit base (contractual liabilities) when the original borrowing tenor ends. They will not have an issue continuing funding for longer duration assets by using such rollovers.

- Any interim liquidity shortfall can be temporarily financed by borrowing from the Interbank market.

- The practice of maturity mismatch is an accepted part of the banking business model and does not lead to compliance issues raised by the bank’s board of directors or regulators.

The need for ALM

As interest rate change over a period of time, the interest rate spread widens (increases) or tightens (decreases). Even with a little volatility in rates, spreads can still change significantly if interest rates move in different directions for assets and liabilities or across maturity tenors and buckets.

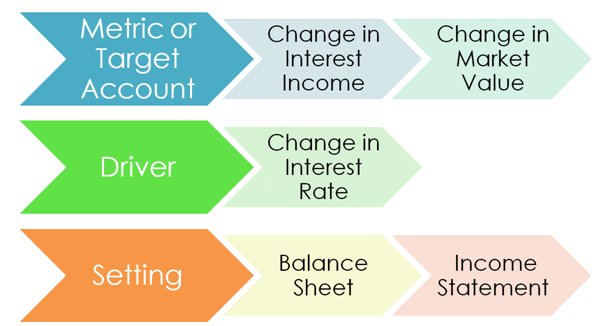

Changes in interest rate spread have a direct and significant impact on bank earnings. This answers the question “What is ALM’s purpose?” It is the reason why the bank’s boards, regulators and industry analysts have an interest in financial disclosures which clearly show earnings sensitivity to expected interest rate changes in the near term. Combined with an interest rate outlook for the next few quarters, most boards can get an indication of earnings direction and use that to manage analyst and shareholder expectations.

Over the years the industry has fine-tuned reports that focus on the impact of interest rate changes on earnings. Though ALM’s purpose and mandate are much broader, earnings sensitivity reporting is now a core part of the monthly ALM discussion during executive committee meetings.

Core Drivers

In addition to earnings sensitivity, ALM reporting also looks at funding (financing), refinancing and liquidity and contractual maturity mismatch risk. To understand these reporting tools we need to get comfortable with three key drivers of the ALM function.

- The shift and changes in interest rates,

- The structure of a typical bank balance sheet, and

- The interaction of (1) and (2) above and its impact on both earnings and shareholder value.

Challenges with ALM

The challenge within the ALM world is that while the framework appears to be basic, things get complicated very quickly. There are assumptions that need to be tweaked as well as understood. A set of neat reports that come with their own readability convention. Explanation of scenarios to board members before a meaningful discussion can begin on ALM strategies specific to those scenarios. Results that need careful interpretation given the assumptions and models used. Report generation uses an even mix of the hypothetical, make-believe and real-world but the impact of decisions, on the basis of these reports, is all real-world. The last thing the board and shareholders want to hear is “But I thought….”

As the Cheshire cat said to Alice, it all depends on where you want to go…

Comments are closed.