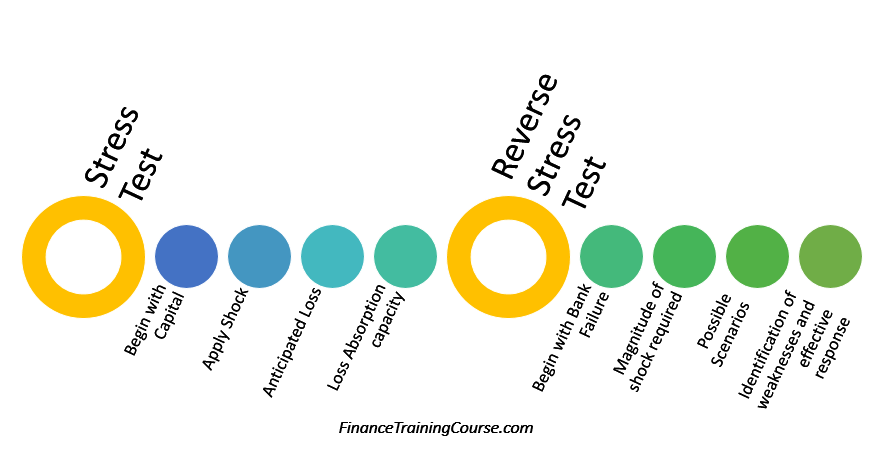

A typical stress test creates a scenario and evaluates how a bank would fare under it. In comparison to reverse stress testing, we use conventional stress tests to assure shareholders, regulators and customers that the capital on the bank balance sheet is sufficient to weather a given storm.

A reverse stress test starts with the failure of a bank. That is the desired or modeled event. The end state. We assume that an unexpected challenge strikes and we don’t survive as a bank. We then identify the exact sequence of events – scenarios and probabilities that would lead to our modeled event – the failure of the bank. And work through possible responses today that can help us avoid that end state.

The reverse stress test helps answers three important questions.

- What would it take to kill us as a bank?

- What sequence of events would lead to such a scenario?

- How can we avoid such a future? What can we do today?

The third question is the most important one. Ideally, a reverse stress test should highlight weaknesses in exposures, the balance sheet, processes, models and/or concentrations. The right answer to the third question focus on addressing specific weaknesses identified by the reverse stress test.

1. Who wants a reverse stress test?

a. Regulators

Bank regulators now require a reverse stress test as part of the stress testing process as well as regulatory reporting. The overall capital adequacy (ICAAP) and internal liquidity adequacy assessment process (ILAAP – EU, EBA and BOE) now include reverse stress testing.

In the late 80’s and early 90’s tracking a daily Value at Risk (VaR) target account was presumed to be sufficient to reduce risk levels at a bank, whether we looked at market or credit risk. The inherent failings of VaR models were adequately highlighted first with the LTCM collapse in August 1998. Then, by the break down of VaR based risk systems during the 2008-2009 financial crisis.

But the financial crisis also highlighted a few other failings:

- One, Capital adequacy is not the best predictor of bank failure.

- Two, liquidity and funding choices have a greater impact on our ability to survive than static ratios measured on a quarterly basis.

- Three, bank boards and management were ill-prepared to weather severe shocks to their systems. Especially those outside the scope of their presumed worst case scenarios.

Post 2008, Regulators have increasingly favored tools such as reverse stress tests. They are a better fit for their needs. Especially when it comes to involving boards in the risk management process. Free from the challenges of calibration with real world probabilities, such a tool may serve the important needs of highlighting weaknesses in bank balance sheets ahead of a crisis.

b. Executive Teams & Boards

While the shape and form of a crisis would not be as important, the insight provided by reviewing possible routes to failure would more than repay any additional costs incurred by performing the reverse stress test. As long as executive teams and bank boards use this opportunity to test and refine their responses to future crisis.

Quantitative Impact Studies conducted by a number of central banks indicate that there is only marginal cost and effort impact for including the reverse stress test in the stress testing protocol of a bank. While regulators are open to small bank only using qualitative analysis for their reverse stress testing submissions, larger banks are expected to use more quantitative techniques.

Calibration with real world probabilities and rating agency models (1 in 200 years, 1 in 100 years models) is not a requirement for regulatory reverse stress testing. However, probabilities of shortfall models allow boards to get a stronger sense of balance sheet strength as well as weaknesses. They also make it possible to set risk appetites using a quantitative approach.

2. Difference between stress testing and reverse stress testing

Here are a few instances that would clarify the difference between a regular stress test and a reverse stress test.

a. Stress test examples

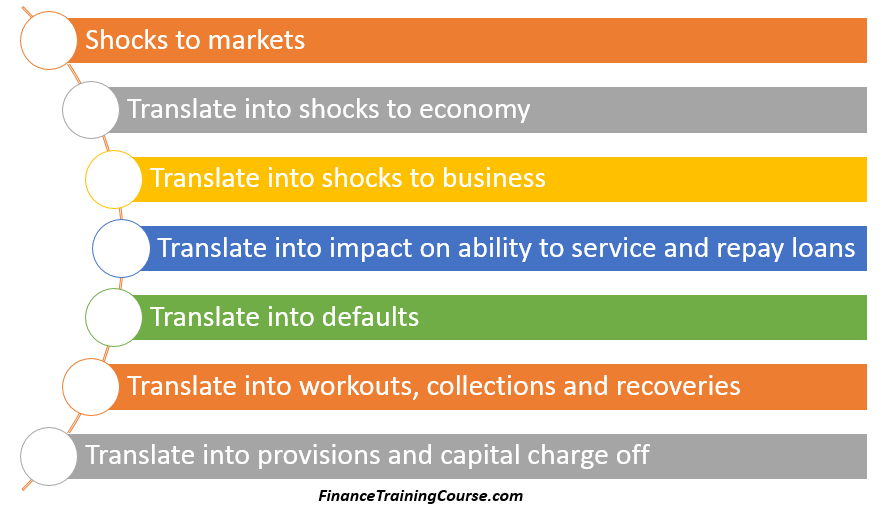

A typical market risk stress test would use the worst case market price shock recorded in the history of our applicable financial markets over the last ten years. It would apply this price shock and evaluate the size of the loss the bank would have to book on its balance sheet. We would quote that loss as part of our stress test report. If the worst possible day in the history of our markets would repeat itself, the bank’s investment book would drop 30% in value in a single day. The objective is to see how much damage a shock can do and that is it.

Typically if we are heavily invested in equities and equity markets go down, bond prices rally as capital moves from riskier equity securities to relatively safer government and treasury bonds. And if for some extreme reason equity and bonds market both go down, the safer (perceived to be) currencies should rally. Depending on which market the run is occurring in that safe currency could be the US dollar, the Japanese Yen or the Swiss Franc. While a flight to safety test may already be in use at a bank, it would stop once the data set reaches its final threshold.

b. Reverse stress test examples

On the other hand, a reverse stress test would use a range of flight to safety scenarios to identify the specific one that would kill the bank. No action on part of management at the point of crisis would be able to deflect.

A reverse stress test would begin with a simple assumption. Our entire stock of capital is wiped out because of a market price event or a combination of such events. With our current book of positions, by how much would markets move for such an event to happen? What would be the probability of such a move? Is there anything we could do to survive such a shock when it occurs? Is there anything we can do now to avoid that specific version of the future? A reverse stress test could be based on actual historical data. For instance, the collapse of market prices in October 1987 (Black Monday) or the financial stocks and debt markets meltdown of 2008-2009.

3. A reverse stress test for credit and liquidity risk?

The concept applied to credit risk uses a similar framework. Our entire account of capital is wiped out because of provisions recorded on overdue and non-performing loans. With our current book of advances, what proportion of loans would need to default to make such an event possible? Over what time? Is there a single relationship, a sector, a sub segment that can sink us all by itself? What combination of events, economic or otherwise would lead to such a situation? (The recessionary credit crunch of 2001-2001 and the major credit lockdown between 2008-2010).

a. Key questions to consider and model

- Credit default impact on Capital – How much would we need to write off and provide for?

- Follow on effects – Impact of defaults and delayed payments on cash flows and liquidity? More importantly what would such events do to our ability to borrow money or rollover existing lines from our institutional lenders? On our stock of liquidity and our ability to defend that stock?

- What would be the impact on overall profitability and ability to do business, our performance and stability ratios on an ongoing basis?

- How would this impact treasury flow business and trade products? Customer flows as well as counter party and correspondent banking limits?

- What would be the follow on impact on income other than provisions? Reversals of accrued interest, fee income, good will and planned future budgeted items related to these product lines?

b. Liquidity risk

While each of these shocks and scenarios sound implausible by themselves to kill a healthy bank, there is one factor that can very easily scale up a minor shock in prices or credit portfolios into a system wide melt down.

What if, the real shock that leads to such an event is neither linked to market or credit risk but is linked to liquidity drying up.

Liquidity problems may arise due to:

- Institutional lenders refusing to rollover lines of borrowing,

- Depositors deserting the bank in large numbers, and

- Treasury counterparties requiring additional collateral and margins on in the money transactions for future fee income generating lines of business.

Liquidity can dry up for many reasons. The biggest is fear triggered by a name crisis involving our bank or a country crisis involving our economy. Both instances trigger chain reactions that can push the strongest of institutions into insolvency. And it doesn’t take much to push a bank into receivership with the right conditions.

Banks don’t fail because their balance sheets are fragile. They are fragile to begin with given the leverage a typical financial institution needs as part of its business model. But that leverage is counterbalanced by market confidence. Once you remove market faith in your ability to survive, the strongest balance sheet transforms into a house of cards.

A simple reverse stress test for liquidity would begin with a run on the bank and would end with analysis and recommendation on the steps needed to take to shore up liquidity today if a run did materialize at some point in the future.

c. Funding choices & ALM Gaps

In the past as part of our training workshops on ALM and Stress Testing, we have also used funding choices and simulating asset liability management gaps to drive banks all the way into insolvency as well as bankruptcy.

4. The key to building a reverse stress test

The key to building a reverse stress test is understanding that it won’t be a single shock that would undo our bank. It would take a combination of factors to sink our ship. Liquidity can make the biggest holes in our hull. Once that happens, a trigger event in financial markets or in our credit portfolio or an accounting scandal would be sufficient to drive us to a point where the market or regulator would take preventive actions.

a. Reverse stress testing factors

While a name crises are one possible source or starting point for reverse stress testing, the three other big ones are:

- a general weakness in the economy (EU or North American recessions),

- an asset price bubble collapse (equity markets 2008-2009), and

- commodity price collapse (the impact of falling oil prices on Middle Eastern, Canadian, Nigerian and Russian economies). These could be mild (Australia) or severe (Nigeria-2016, Dubai-2009 and Russia-2015-16) or in somewhere in between (Iran and India).

b. Modeling the factors

Modeling broader economic weakness is always a challenge. However, credit portfolios tend to behave in well recognized cycles when hit by recessionary shocks. Certain economic segments remain neutral while others weaken significantly (airlines, hospitality, construction, building materials). Liquidity and cash are hoarded and forced sale value of pledged collateral falls. Customer delay payments but if their core business is strong and the bank is willing to work with them, everyone can ride the cycle.

But the modeling exercise will vary. For instance, modeling the impact of falling oil prices on construction and real estate development in Dubai is a different exercise from modeling the impact of the same shock on refining complexes, down stream petrochemical manufacturers in China or shipping industry and the Baltic Dry Index in Singapore.

c. Consider broader applications

We also have to understand that the reverse stress test is not just for regulatory consumption. Here is what the FSA has to say about the intent behind the stress test as part of their FAQ on reverse stress testing.

We are asking firms to identify those events (or confluences of events) that would lead to their business model failing after currently available management actions had been taken.

This will enable firms to identify those management actions that would not be sufficiently effective in their current state of development and/or would not currently be possible.

Given this knowledge, firms should then consider:

- Strengthening currently available management actions to the point that they could prevent failure of the business model and/or

- Putting in place the conditions necessary for new, credible management actions, with the outcome that the business model subsequently would not fail under the same single event or set of events.

5. What is bank failure?

There is also the failure threshold argument that needs to be considered. Market participants and regulators don’t wait till the entire stock of capital is gone before reacting to a bank in difficulty. They react on a preemptive basis while they (counterparties) can still get their money out and regulators can still salvage the bank’s balance sheet. The only way you can ensure that you are paid out in full is if you are the first one out of the gates.

This means the definition of bank failure is not bankruptcy or even insolvency. It could be set as high as the inability to transact regular business under normal conditions. It’s the same definition that the FSA points to in their FAQ’s on reverse stress testing.

6. FSA’s guidance on bank failure and expectations

The “FSA Reverse Stress Testing Surgeries – FAQ” answers a number of key questions addressed by a regulator on expectations as well as methodologies. Here are two important extracts from the document.

a. On Bank Failure

Firms may start to develop scenarios that lead to the business model failing by considering the cause, consequence or impact (financial or otherwise) of one or more events that lead to the failure of the firm. Firms should note that ’failure’ is not necessarily identified with the point at which the capital and/or liquidity of the firm is exhausted. For example, it may be the point at which:

- Market participants see that the firm is over-exposed to a particularly risky sector (cause);

- Market sentiment results in the refusal of market counterparties to deal with the firm or under such onerous conditions that it is economically unviable for the firm to do so (consequence); or

- The firm is unable to transact any new business and its revenue streams dry up (impact).

Firms might consider any one of these as a starting point from which to develop the scenarios. (This may be contrasted with a real-world failure, where the sequence of cause-consequence impact occurs in that distinct order.)

And

b. On Expectations from the process

The reverse stress-tests that cause a firm’s business model to fail are those where prospective management actions would not be sufficient to prevent such a failure.

Having identified such scenarios, we ask firms to think about ways in which they might strengthen their business models now to mitigate the risks posed by the scenarios.

This strengthening may include enhancing the impact that prospective management actions would have, or putting in place the necessary conditions for taking new management actions that could avert business model failure

7. Related Stress Testing Terminology

- Vertical Stress Test – Stress Test one institution

- Horizontal Stress Test – Stress Test a segment or industry

- Bottom up Stress Test – Stress test individual banks and add them up by pushing up the results

- Top Down Stress Test – Stress test entire segment and then push down results

References

- FSA Guidance – Reverse Stress Testing surgeries – FAQ

- Using volatility of earning to estimate bank capital shortfall probabilities.