FAS 157 Fair value liabilities disclosure. Term B loans, credit lines, revolvers and LCs.

Fair values of highly customized and ill-liquid credit instruments like institutional Term B loans, credit lines, revolving credit facilities, letters of credit, etc., are determined using assumptions and inputs that are in most cases un-observable. Under the Financial Accounting Standards Board (FASB) FAS 157 standard their values will likely qualify as those measured at fair value using significant un-observable inputs (Level 3).

This series of posts will first provide a brief review of some of the elements of the FAS 157 standard and then walk through the methodology that may be used to value such instruments.

FAS 157 – a recap

Under Financial Accounting Standards Board (FASB) FAS 157 financial instruments (assets or liabilities) have to be measured at fair value. This means that the asset or liability needs to be measured at the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

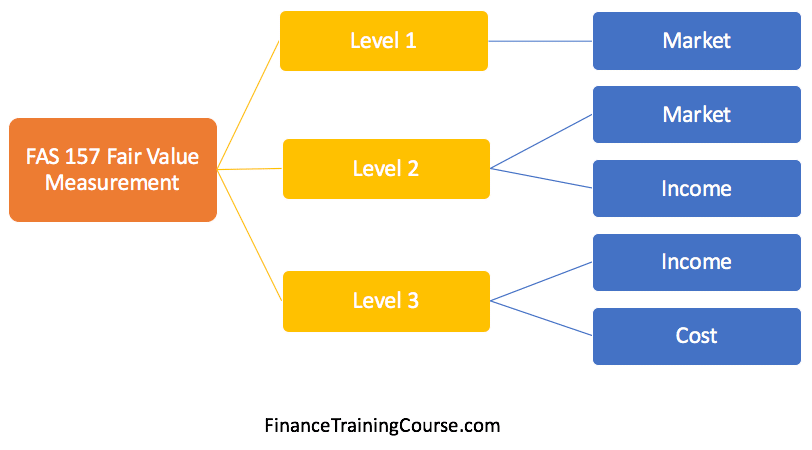

The fair value measurement is subject to a hierarchy that has to be disclosed along with the resultant fair value in the financial statements of the entity. This hierarchy is dependent on the inputs/ assumptions that are used in the calculation of the fair value and comprises of three levels.

Level 1 inputs are unadjusted quoted prices in active markets for identical assets or liabilities available on the valuation date. By its very nature, Level 1 inputs give the most reliable result for fair value.

Level 2 inputs are based on observable inputs other than quoted prices for identical assets or liabilities in active markets. They may include quoted prices of similar instruments in active markets or quoted prices of identical assets or liabilities in inactive markets or other inputs for the same assets or liabilities like yields, credit spreads, default rates, loss given default rates, prepayment rates, etc. Adjustments may be needed to these inputs before they can be used in valuing the given asset or liability.

Level 3 inputs are unobservable in the market and reflect management’s own assumptions as to the inputs that market participants will include in a valuation of the asset or liability. These inputs should be developed based on the best information available including the entity’s own data and must include information that a reasonable market participant would consider in their valuation exercise.

Acceptable valuation approaches under FAS 157 include the market approach, the income approach and the cost approach.

Market approaches use quoted prices and other information relevant to identical or comparable assets or liabilities to derive the value of the instrument. They may be used with Level 1 or Level 2 inputs to determine fair value.

Income approaches use valuation techniques to discount future amounts of the asset or liability to a single amount as of the valuation date. They are used with Level 2 or Level 3 inputs to calculate fair values of assets or liabilities.

Cost approaches calculate the replacement cost of an asset or liability.

In this series on FAS 157 fair value of liabilities we will focus on the income approach, in particular present value techniques for valuing the asset or liability. There are two type of present value techniques – discount rate adjustment technique & expected present value technique mentioned in the standard. The former discounts contractual cash flows using a discount rate that reflects expectations about future risk. The latter method uses probability weighted cash flows and either discounts this value using the risk free discount rate and then adjusts the resulting value by deducting a cash risk premium (Method 1) or discounts the value using a discount rate that is equal to the risk free rate and a risk premium that reflects the systematic risk associated with these expected cash flows (Method 2).

- FAS 157 Fair Value disclosures – Term B Syndicated Loans

- FAS 157 Fair Value disclosures – Revolving credit facilities

- FAS 157 Fair Value disclosures.

References

- Building a credit risk valuation framework for loan instruments – Scott Aguais, Larry Forest and Dan Rosen – Algo Research Quarterly, Vol. 3, No. 3, December 2000, pp. 21–46.

- Statement of financial accounting standards No. 157 – Fair Value measurements – FASB – 2010

- Credit exposure and valuation of revolving credit lines – Robert A Jones & Yan Wendy Wu – 19 July 2009

- Questions you should be asking about Senior Secured Loans – Joe Lemanowicz – May 2011

- A one-parameter representation of credit risk and transition matrices – CreditMetrics Monitor Third Quarter 1998 (pp.46 -58)

- Ratings symbols and definitions – Moody’s Investor services – May 2016