This week we took a deep look at a number of common structured products and their hedge effectiveness. One product stood out in terms of its performance – the unconventional participating forward contract.

Traditionally when we look at hedging structures for customer needs, cost considerations drive almost all conversations. Customers are hesitant in paying out of pocket for solutions that may or may not be needed depending on which direction their risk exposure go. If forward cover is needed and they can buy at below market costs when markets rise, everyone is happy. But if the cover is not needed and they end up buying at above market prices when markets decline, things get awkward.

A number of times, especially in large organizations as well as state owned or state backed enterprises the allure of zero cost structure is driven by anticipated audit objections. Why did you buy this structure if it wasn’t used? Couldn’t you tell ahead of time if you really needed to manage your risk? Was this a useful allocation of capital and expenses when there was no way to predict the direction markets would take? Hindsight is 20/20 and is always strongest with teams with compliance checklists.

The case for risk management is weakest when it is not needed or required. That is when the second guessing starts. Once the blame game begins every one wants to jump on the bandwagon. The case for risk management is strongest generally just after the entire population of the barn has escaped after someone left the door open or the barn has been burnt to the ground and someone left the door locked. You just can’t win.

In such a setting forward contracts (zero upfront cost) and zero cost structures are immensely appealing.

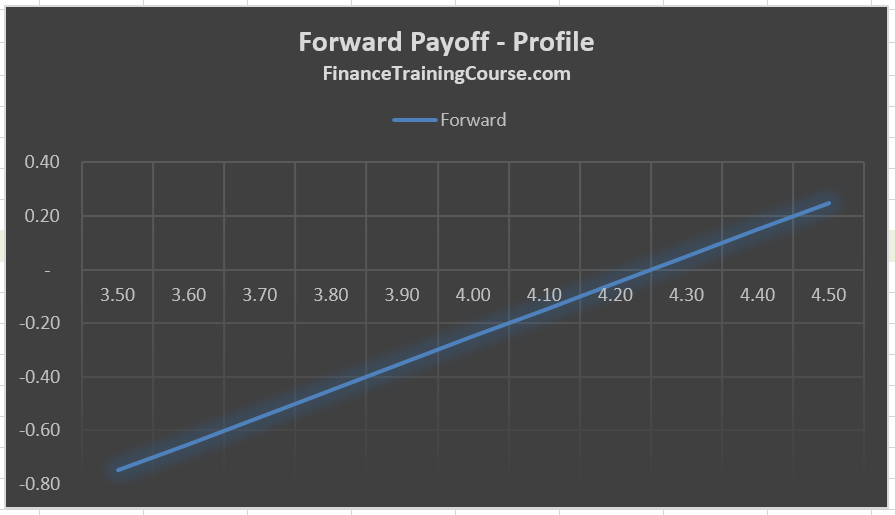

Forward contracts are the simplest and basic of all products but their biggest strength is also their biggest weakness. A forward contract strength is that it allows us to hedge our exposures using zero upfront cost. It allows us to buy or sell at prices different from those prevailing in the market as long as we have the foresight to lock them in weeks or months in advance. The problem is when markets move against us and we have to buy at above market prices. This happens when the anticipated future shock does materialize or markets move in the opposite direction.

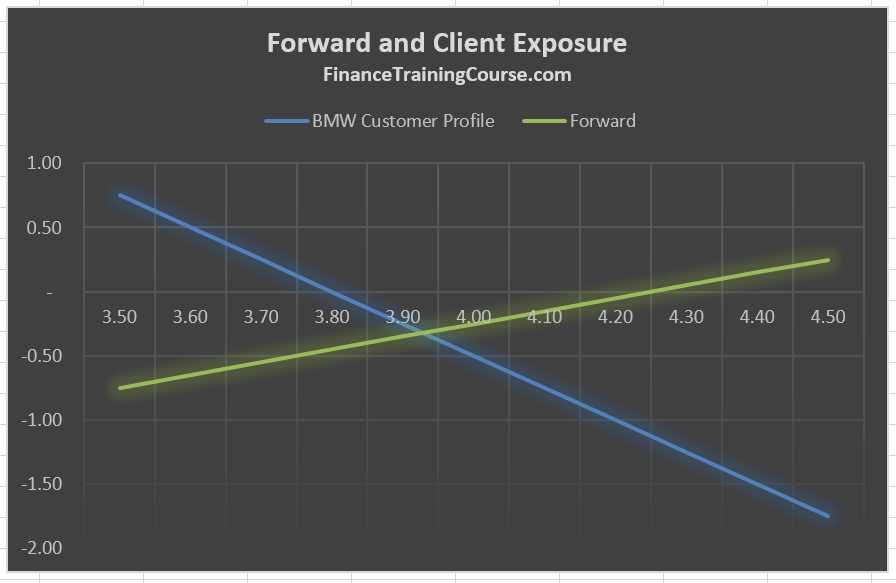

A simple example will help illustrate the case. An importer of BMW 7 series in Dubai has to remit Euros on a regular basis to BMW Germany. Given the recent volatility in both USD and Euro, upcoming talks on Brexit and the stated Federal Reserve goal of raising interest rates, there has been a great deal of uncertainty with respect to exchange rate outlook. If our client decides to hedge using forward contracts he can lock in a rate but he is still exposed to some adverse deviations if the rates move against him. He will be able to hedge his exposure and lock in a rate but his worry is what if the exchange rate decline and he is stuck with buying euros at a significantly higher price.

Exchange traded vanilla options are the next best solution but they come with an upfront cost. Isn’t there something in between that we could use?

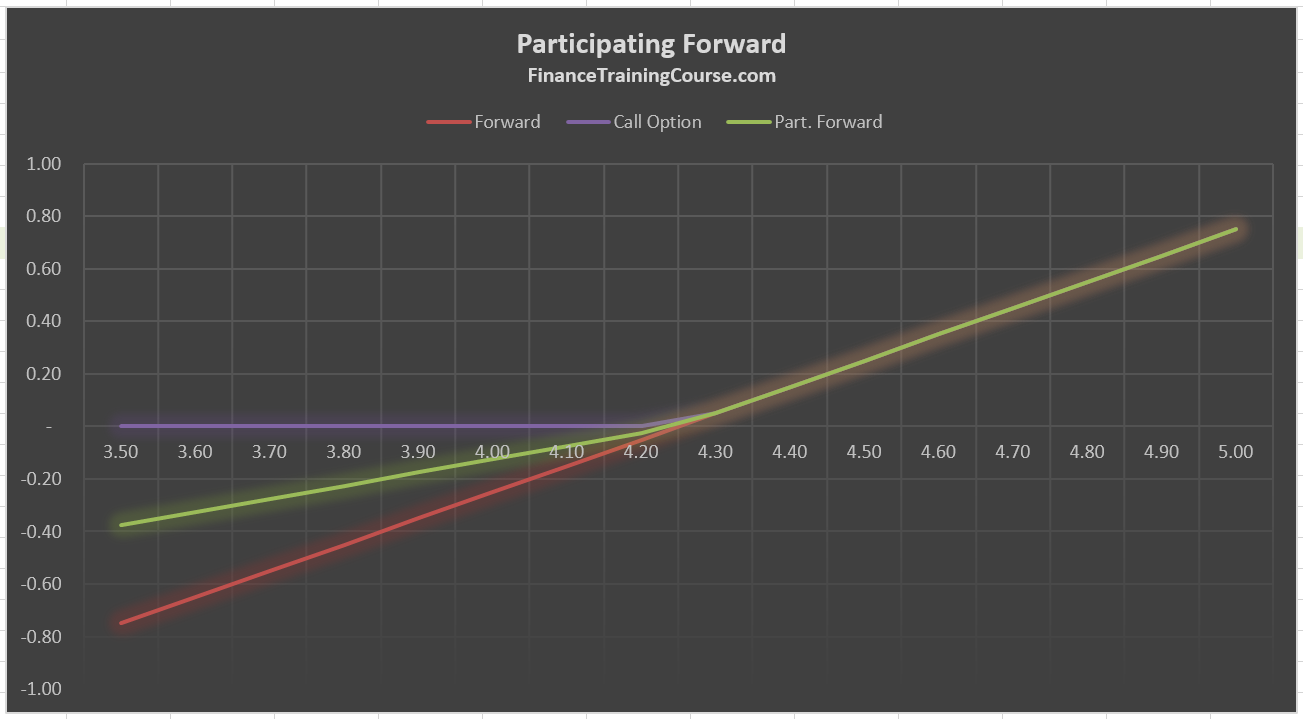

Enter the participating forward contract. Participating forward come in many flavors. The one we are interested in is not a zero cost structure. It is a structure that sits half way between an option contract and a forward contract. The reason for its attractiveness is very simple. When prices rise we are able to purchase the underlying security at half the effective cost of options. Because the formula we have used is one half forward contract and one half call option. When price decline we only have to buy half the covered amount using our forward contract. Once again because we only covered half our exposure through forward contracts and the other half through a call option which has expired worthless.

Going back to our friend the BMW importer if we needed to buy Euro 10 million, we would buy a call option for 5 million and enter into a long forward contract for 5 million. It will be cheaper than buying a call option on 10 million and will have a slightly better downside protection than entering into a long forward for purchase 10 million euro.

This is the vanilla, non zero cost version of a participating forward contract. The primary benefit is that it delivers a below average cost profile when you are in the money (cheaper than vanilla call, more expensive than long forward) as well as a lower than usual downside when you are out of money (better than a forward, slight worse off than a long call).

The zero cost version involves a more complicated and less recommended strategy. To achieve zero cost rather than use the forward to your benefit and advantage you aim for an off market rate and use that to cover the cost of the call or vice versa depending on the original intent of the transaction. That strategy and structure is significantly more riskier than the one covered above.