Market Analysis

Crude Oil

- Brent and WTI pries remained bullish till Friday before moving south primarily due Hurricane Irma and Chinese aim to reduce capacity of its teapot refineries.

- Hurricane Irma is expected to make landfall on Saturday and expected to impact the demand for energy and fuel for Florida and Southeast.

- From Monday till Thursday both Crude and Brent remained bullish on impact of Hurricane Harvey, Production cut from Saudi Arabia and weaker US dollar performance.

- Hurricane Harvey has impacted US crude production by 750,000 BPD resulting in operating rate reduction for refineries, surging the gasoline prices.

- Saudi Arabia will cut oil production by 350,000 BPD in October for its worldwide customers especially in Japan.

- Crude prices got support from weak US Dollar as greenback slide to 31 month low on Friday.

- Brent price reached $54.49/BBL before sliding to $53.78/BBL on Friday, closed at $53.78/BBL, an increase of 1.95% from last, whereas WTI closed at $47.48/BBL, after reaching at $49.14/BBL on Wednesday.

- Brent/WTI spread this Friday closed at $6.30/BBL, highest in last two years.

- Libyan largest oilfield is now fully operational after couple of week’s output issues due to armed group assault; Libyan oil production fell from 990,000 BPD to 830,000 BPD in August due to pipeline closures.

- EIA Weekly report reported a buildup of 4.6 million barrels with stock at 462.4 million barrel on 1st September 2017; against a market expectation of 4.0 million barrels build up.

- Gasoline inventories at 226.7 million barrel reported on 1st September 2017, recoding 3.2 million draw on week on week basis.

- Refinery use fell 16.9% on the week due to the impact of outages as flooding caused substantial damage to infrastructure.

- Baker Hughes rig count reported a decrease by 3 in oilrigs with total standing at 756, whereas gas rig increased by 4 and now at 187, with a total number of rigs at 944.

Natural Gas

- Henry Hub prices closed at $2.89/MMBTU, down by 5.86% from last Friday, due to cooler than normal temperature, expected lower power generation due to Hurricane Irma and increased production and gas rigs number.

- Temperature forecast is cooler than the week ending on 8th September 2017 and lower than normal all across US with the exception of Rocky Mountains.

- Market is expecting demand destruction due to Hurricane Irma, as at the time of writing this report 119,000 homes and business are without power and 3.1 million homes are expected to be without electricity because of the storm.

- Average total supply rose by 2% compared with last week, whereas demand remained unchanged from last week and stands at 55.7 BCF/D.

- Baker Hughes reported an increase in natural gas rigs by 4.

- US LNG export suspended from Sabine Pass due to Hurricane Harvey and resumed loading from 6th September 2017 due to high currents.

- Working gas in storage was 3,220 BCF as of Friday, September 1st 2017, an increase of 65 BCF from previous week, which was inline with expectations. Stocks were 212 BCF less than last year at this time and 15 BCF above the five-year average. At 3,220 BCF, total working gas is within the five-year historical range.

- October Natural Gas futures settled at $2.900/MMBTU, whereas $2.976/MMBTU for November & $3.131/MMBTU for December delivery on Friday, exhibiting bearish tone.

- Gas prices in UK remain bullish primarily due to uncertainty of Norwegian gas pipeline supply due to planned maintenance, cooler weather outlook, increase in prices for carbon and emission prices up by €0.55 for December 2017 and weaker LNG outlook for European market.

- UK power generation is weak from Solar, however wind power generation has been up, however cooler temperature has increased residential demand.

- NBP UK DA prices closed 45.9360 Pence/Therm (equivalent $$6.07/MMBTU) on Friday, increased by 1.03% from last Friday of 45.5300 Pence/Therm.

- NBP UK curve market for October and November closed at 45.2500 Pence/Therm & 49.1100 Pence/Therm (equivalent of $5.98/MMBTU & $6.49/MMBTU), putting bullish trend on prices and making it attractive for spot LNG offers from US.

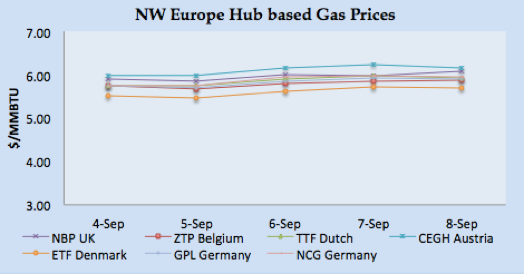

- Overall cooler temperature in France and Netherlands along with weaker LNG arrival outlook and Norwegian gas supply issues has resulted in bullish rally for TTF and PEG Nord.

- Gas Prices in Iberian Peninsula remained range bound as weather eased a bit and there is not significant increase in the demand.

- TTF closed at €16.82/MWH (equivalent of $5.94/MMBTU), PEG Nord France closed at €16.61/MWH ($5.86/MMBTU), and Spanish at €17.25/MWH ($6.17/MMBTU) on Friday.

- In the curve market TTF November closed at €17.46/MWH ($6.16/MMBTU) and December at €17.17/MWH ($6.29/MMBTU).

- November & December PEG Nord forward prices closed at €17.91/MWH ($6.32/MMBTU) & €18.33/MWH ($6.47/MMBTU, defining the price direction for winter season.

Currency

- US Dollar remained bearish through out the week due to geo political tension, uncertainty around interest rate hike, Hurricane Irma and Euro strength.

- Geopolitical tension between US and North Korea along with fear that North Korea may launch another missile is supporting safe heaven currencies like Yen and Swiss Franc to gain against US Dollar.

- Uncertainty prevailing as mixed comments from Fed Officials are dampening the expectation of interest rate hike this year, however, Dudley is reiterating that central bank should gradually increase the interest rate.

- Hurricane Irma transforming back into category 5, and insurance companies are concerned as investors feeling massive damages in its path.

- Euro performed strongly due to ECD decision on leaving interest rates unchanged and tapering of bank’s asset-purchase program to be delivered in October.

- Market is looking at CPI data for the month of August to be released next week with the expectation of improvement from July, any downward deviation will bring bearish factor on US dollar.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, fell by 0.25% to 91.26.

- Euro throughout the week remained strong against USD and closed at $1.2031, increased by 1.50% from last Friday. The bullish Euro tone is attributed to ECB decision of keeping the rates unchanged.

- GBP/USD closed at 1.3210, a jump of 1.98% from last Friday, primarily on weak USD and strong Euro.

- Japanese Yen remained bullish during the week due to US-North Korea tension, which encouraged investors to focus more on Yen. Yen/USD closed at

- USD/JPY fell to 109.19, as US-North Korea tension is causing the investor to focus more on Japanese Yen as a safe haven currency. YEN/USD jump by 2.36% and closed at 0.00928 (Yen107.70675) on Friday.

- AUD/USD closed at 0.80713, stronger against USD on Friday due to weaker USD.

- Chinese Yuan jump to 6.47571 on Friday, an increase by 1.27% from last Friday.

Weather

- UK, Germany & Belgium weather remained pleasant around 17-23oC and expected to be cooler next week around 15-18oC with rain forecast.

- Netherland weather remained cold between 17-22oC, and expected to be cooler next week around 15-18o

- France was cold this week around 18-23oC and expected to be cooler next week around 17-20oC with rain forecast.

- Weather easing a bit, but still warm in Spain & Portugal with the temperature around 26-34oC and expected to around 23-30oC next week.

- Temperature in Argentina remained around 15-23oC, and expected to be bit cooler around 15-19o

- Brazil remained hot with the temperature around 26-30oC, and expected to remain around the same range next week.

- Mexico is getting warm with the temperature around 20-23oC and expected to remain same next week.

- Middle East region summer season still prevailing, with Egypt around 35oC and expected to be warmer next week, Kuwait 47oC and Dubai around 44oC, next week weather easing a bit with Kuwait around 43oC and Dubai around 38o

- Indian Subcontinent is in monsoon season with temperature in Pakistan and India around 30-35oC, and expected to remain same next week.

- Temperature eased a bit but still hot in North East Asia, with the temperature around 27-35oC in Taiwan, 24-30oC in Korea, China 28-32oC, and Japan is around 23-28o Weather expected to remain same next week, with Taiwan 29-33oC, Korea around 24-29oC, China 28-30oC & Japan 28-29oC.

- South East Asia already in hot weather, Thailand around 30-35oC, Indonesia and Malaysia around 33oC, and will remain same next week.

- USA Weather: Overall weather remained warm but eased down and expected to be cooler next week.

LNG

- Global LNG prices remained bullish through out the week due to anticipating winter demand, forward curve market specially UK and TTF, rising Brent prices and absence of shipment from Sabine Pass.

- This has created some urgency from portfolio players and utility buyers to cover their buying in anticipation of winter demand and bullish price trend.

- On Supply side there are ample availability from end September as Australia’s Wheatstone is expected to be in production by End September along with resumption of supply from Sabine Pass.

- There is demand arising from India post Monsoon season along with expectation of buying from China and Korea.

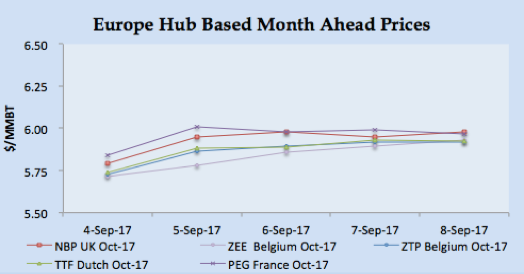

- European Hub prices also played pivotal role as due to Norwegian supply constraint and cooler weather along with bullish carbon and emission price resulting in upward movement for European Hub prices especially for TTF and NBP.

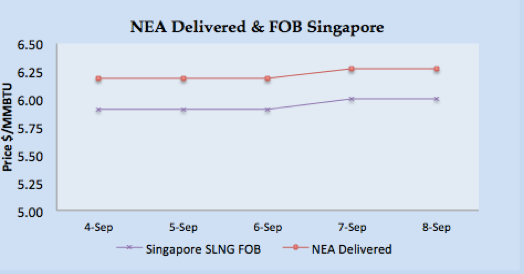

- Asian prices were heard to close at JKM $6.4250/MMBTU, SLNG NEA Delivered at $6.2680/MMBTU and FOB Singapore at $6.0040/MMBTU, higher than last week.

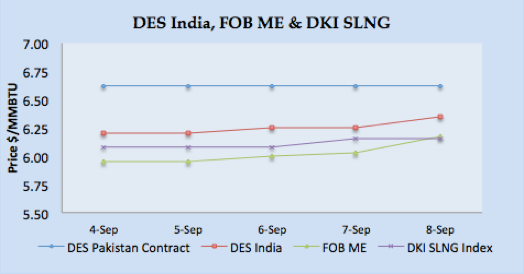

- Indian buyers are in the market for November delivery and based upon Singapore, DES India is calculated around $6.20- $6.30/MMBTU level. DKI SLNG Index on Friday reported at $6.1550/MMBTU.

- JKM Future curve market closed at $6.210/MMBTU, $7.100/MMBTU & $7.525/MMBTU for October, November & December respectively. Future prices direction is emphasizing that market will be entering in winter buying season soon.

- European hub price remained bullish due to cooler weather in North West Europe along with hot weather in South West plus Norwegian supply issue due to planned maintenance and poor LNG vessel arrival outlook.

- For North West Europe imported LNG prices assumed based upon 96% of NBP UK October prices, which comes around $5.7408/MMBTU. For Netherland market the imported LNG prices are estimated at 20 cents discount of TTF October price of $$5.92/MMBTU level.

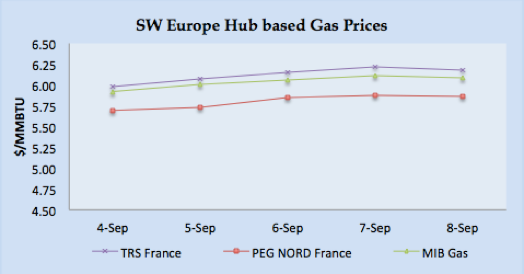

- South Western gas prices were stable, as hot weather plus Norwegian maintenance and poor LNG outlook has put pressure on the prices. PEG Nord closed at €61/MWH ($5.86/MMBTU) whereas Iberian Peninsula prices closed at €17.25/MWH ($6.09/MMBTU) on Friday.

- South West Europe imported LNG prices were estimated at 5 cents discount to PEG NORD October Forward price, calculated to come around $5.920/MMBTU level.

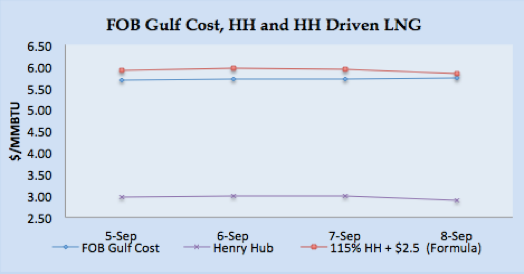

- US Producer price on FOB basis for October delivery comes around $5.480/MMBTU whereas for November delivery it is $5.990/MMBTU. This is based NBP curve price for October and November.

- Based upon November future price for North East Asia and European destinations, US Gulf Coast manufacturers prices are coming around $5.50/MMTU level.

- FOB EAM prices based upon DES Spanish from Algeria is calculated to be around $5.940/MMBTU level on Friday.

- South Korea is planning to boost its power generation share from LNG and renewables from 4.7% to 9.5% by 2030 as outlined in the draft policy from the Korean energy ministry.

Author’s Comments

- Brent based prices in comparison with JKM forward prices seems to be more attractive and looking at Brent price bearish trend and supply availability, the upside on spot JKM price will be controlled for winter season.

- Cooler Weather & Poor LNG outlook for European destination will keep European Imported LNG price bullish especially in the UK, which does have an adequate gas storage facility, so we expect prices to remain bullish in the European market.

- Overall LNG price is forecasted to remain bullish for October delivery cargoes and November seems to be balanced, as there will be supply availability from US and Australia besides the regular supply.

|

|

|

|

|

|

LNG Merchant Activity

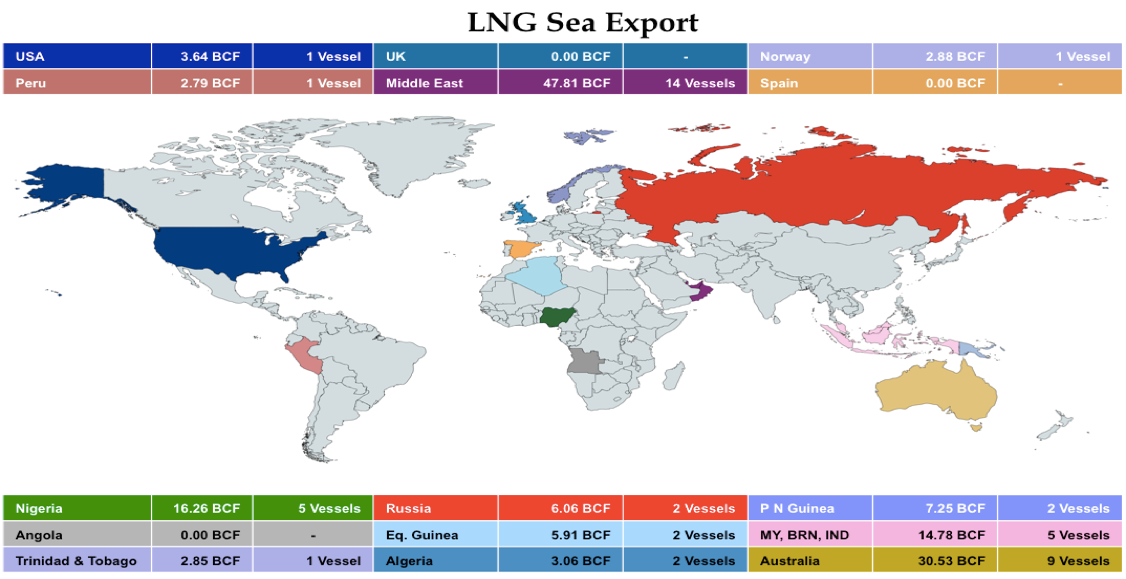

- 45 vessels carrying 2.82 million tons (143.81 BCF) loaded from various supply centres, a decrease by 0.38 million tons from last week.

- Primarily decrease in the quantities is from Qatar, Angola & Trinidad & Tobago.

- Month to date 17 vessels carrying 1.16 million tons, have been dispatched from Ras Laffan, Qatar, this represent 35% of total global trade

- 13 Vessels left from Qatar carrying 44.98 BCF for India, Korea, Japan and Europe.

- Five vessels carrying 16.26 BCF departed from Nigerian port, two for European destination.

- Algeria loaded two vessels carrying 3.06 BCF for Italy and Spain.

- Pont Fortin, Trinidad & Tobago loaded one vessel with 2.85 BCF.

- Two vessels loaded from Brunei with load of 4.58 BCF, one destined for Japan.

- Nine vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Korea carrying 30.53 BCF, depicting regional penetration of Australian producers.

- One cargoes left for Poland with 2.88 BCF from Norway

- Middle Eastern terminal at Das (UAE) loaded one vessel carrying 2.83 BCF for Japan, whereas none loaded from Qalhat, Oman.

| Departure Date | Vessel Name | Capacity (CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 2-Sep-17 | LNG BAYELSA | 137,500 | Bonny, Nigeria | Europe | 11-Sep-17 | 2.84 |

| 3-Sep-17 | MARAN GAS AMPHIPOLIS | 173,400 | Bonny, Nigeria | Not Known | 09-Oct-17 | 3.58 |

| 5-Sep-17 | GOLAR KELVIN | 162,000 | Bonny, Nigeria | Not Known | 26-Sep-17 | 3.34 |

| 8-Sep-17 | LNG LAGOS II | 177,000 | Bonny, Nigeria | Not Known | 3.65 | |

| 4-Sep-17 | EXCELSIOR | 138,000 | Bonny, Nigeria | Spain | 12-Sep-17 | 2.85 |

| 2-Sep-17 | EXPRESS | 150,900 | Punta Europa, Africa | Not Known | 22-Sep-17 | 3.11 |

| 8-Sep-17 | SESTAO KNUTSEN | 135,357 | Punta Europa, Africa | Not Known | 27-Sep-17 | 2.79 |

| 6-Sep-17 | CHEIKH BOUAMAMA | 74,425 | Skikda, Algeria | France | 08-Sep-17 | 1.54 |

| 2-Sep-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | Italy | 04-Sep-17 | 1.53 |

| 3-Sep-17 | GALLINA | 135,269 | Pampa Melchorita, Peru | Not Known | 2.79 | |

| 3-Sep-17 | BW BOSTON | 138,059 | Point Fortin, Trinidad | Not Known | 20-Sep-17 | 2.85 |

| 8-Sep-17 | RIOJA KNUTSEN | 176,300 | Sabine Pass, USA | Spain | 23-Sep-17 | 3.64 |

| 6-Sep-17 | SERI CENDERAWASIH | 206,000 | Bintulu, Malaysia | Japan | 12-Sep-17 | 4.25 |

| 4-Sep-17 | METHANE SPIRIT | 163,195 | Bintulu, Malaysia | Taiwan | 03-Sep-17 | 3.37 |

| 6-Sep-17 | GRACE DAHLIA | 177,425 | Lese, Papua New Guinea | Japan | 15-Sep-17 | 3.66 |

| 3-Sep-17 | SPIRIT OF HELA | 173,800 | Lese, Papua New Guinea | Taiwan | 12-Sep-17 | 3.59 |

| 8-Sep-17 | HYUNDAI UTOPIA | 125,182 | MIGAS LNG BATU, Indonesia | Japan | 13-Sep-17 | 2.58 |

| 4-Sep-17 | AMUR RIVER | 146,748 | Prigorodnoye, Russia | Japan | 10-Sep-17 | 3.03 |

| 6-Sep-17 | OB RIVER | 146,791 | Prigorodnoye, Russia | Taiwan | 14-Sep-17 | 3.03 |

| 6-Sep-17 | AMALI | 147,228 | Sieria Oil Terminal, Brunei | Japan | 16-Sep-17 | 3.04 |

| 8-Sep-17 | BELANAK | 75,000 | Sieria Oil Terminal, Brunei | Not Known | 1.55 | |

| 3-Sep-17 | DAPENG SUN | 147,200 | Dampier, Australia | China | 10-Sep-17 | 3.04 |

| 2-Sep-17 | NORTHWEST STORMPETREL | 125,525 | Dampier, Australia | Japan | 26-Sep-17 | 2.59 |

| 6-Sep-17 | NORTHWEST SWAN | 140,500 | Dampier, Australia | Japan | 19-Sep-17 | 2.90 |

| 8-Sep-17 | WOODSIDE ROGERS | 159,800 | Dampier, Australia | Pacific Basin | 17-Sep-17 | 3.30 |

| 4-Sep-17 | CESI BEIHAI | 240,000 | Gladstone, Australia | China | 15-Sep-17 | 4.95 |

| 3-Sep-17 | GASLOG SYDNEY | 154,948 | Gladstone, Australia | China | 18-Sep-17 | 3.20 |

| 7-Sep-17 | LNG SATURN | 153,000 | Gladstone, Australia | China | 19-Sep-17 | 3.16 |

| 3-Sep-17 | LNG KOLT | 210,000 | Gladstone, Australia | Korea | 14-Sep-17 | 4.33 |

| 7-Sep-17 | K.MUGUNGWHA | 148,776 | Gladstone, Australia | Korea | 19-Sep-17 | 3.07 |

| 2-Sep-17 | ARCTIC DISCOVERER | 139,759 | Melokya, Norway | Poland | 09-Sep-17 | 2.88 |

| 5-Sep-17 | UMM AL ASHTAN | 137,000 | Das, UAE | Japan | 20-Sep-17 | 2.83 |

| 5-Sep-17 | PSKOV | 170,200 | Ras Laffan, Qatar | Argentina | 29-Sep-17 | 3.51 |

| 4-Sep-17 | WILPRIDE | 156,007 | Ras Laffan, Qatar | Egypt | 12-Sep-17 | 3.22 |

| 3-Sep-17 | TEMBEK | 211,885 | Ras Laffan, Qatar | Far East | 20-Sep-17 | 4.37 |

| 4-Sep-17 | AL KHUWAIR | 211,885 | Ras Laffan, Qatar | India | 10-Sep-17 | 4.37 |

| 4-Sep-17 | ASEEM | 154,948 | Ras Laffan, Qatar | India | 07-Sep-17 | 3.20 |

| 3-Sep-17 | SK SUNRISE | 135,505 | Ras Laffan, Qatar | Korea | 18-Sep-17 | 2.80 |

| 3-Sep-17 | AL BAHIYA | 205,981 | Ras Laffan, Qatar | Korea | 5-Sep-17 | 4.25 |

| 6-Sep-17 | HYUNDAI COSMOPIA | 134,308 | Ras Laffan, Qatar | Korea | 21-Sep-17 | 2.77 |

| 2-Sep-17 | AL MARROUNA | 149,539 | Ras Laffan, Qatar | Mediterian | 09-Sep-17 | 3.09 |

| 6-Sep-17 | ARCTIC AURORA | 154,800 | Ras Laffan, Qatar | Not Known | 18-Sep-17 | 3.19 |

| 8-Sep-17 | AL NUAMAN | 205,981 | Ras Laffan, Qatar | Not Known | 4.25 | |

| 4-Sep-17 | TAITAR NO. 4 | 144,596 | Ras Laffan, Qatar | Taiwan | 18-Sep-17 | 2.98 |

| 5-Sep-17 | TAITAR No. 4 | 144,596 | Ras Laffan, Qatar | Taiwan | 18-Sep-17 | 2.98 |

| Total | 143.81 | |||||