How is the world equipped to handle an additional 1.29 million barrels per day of demand in 2019? We once again turn to OPEC’s December 2018 monthly review.

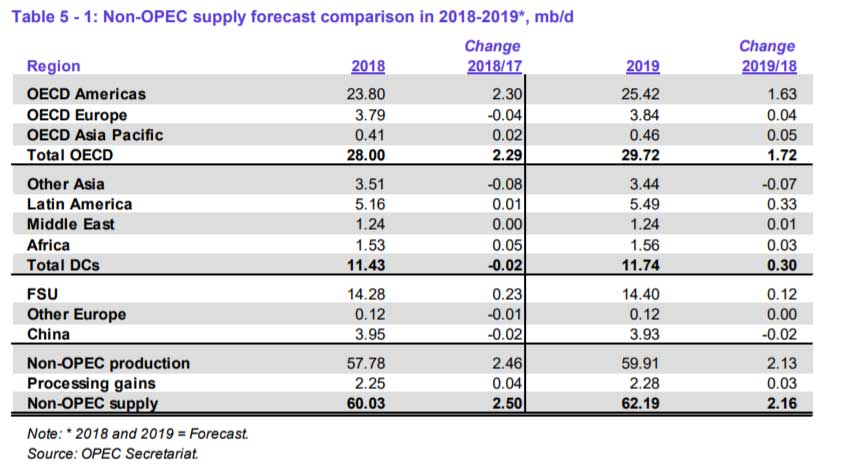

OPEC breaks down supply across non-OPEC and OPEC suppliers. Non-OPEC supply in 2019 is likely to grow by 2.16 million barrels per day to 62 million barrels per day as per December 2018 figures. Compare this with 2.5 million barrel per day of growth booked in calendar year 2018 from the same sources. Growth in supply from non-OPEC sources is slowing down but it is still running at 3.6% a year.

Keep this figure in mind. This is a group that has no incentive to align its production strategy with OPEC. It may benefit from an OPEC coordinated supply cut but these producers cannot curtail production at short notices.

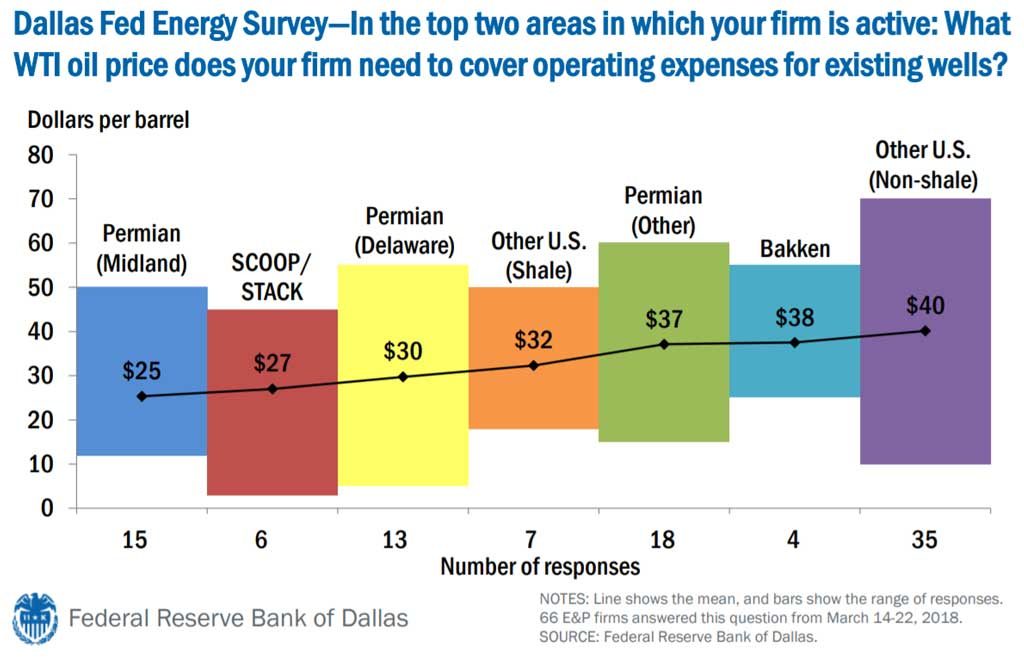

Often because of operational reasons and in case of US shale because of liquidity and cash flow concerns. When oil prices decline this group has an even stronger incentive to pump more oil to meet their cash flow requirements. Consensus across recent industry studies is that marginal cost of producing a barrel of at operational tight oil wells in the US has dropped by 40% in recent years. An efficient shale producer in the Permian basin can now make money with oil prices hovering in the lower $40 a barrel range. The Dallas Fed energy survey (March 2018) indicates breakeven prices at the most efficient producers are now as low as $25 a barrel leaving ample room for profitability at the $45-$50 price level.

Of the projected growth above, 1.7 million barrels per day (79%) is likely to come from producers in the US. Of that 79%, 1.17 million barrels per day in additional production will come from shale oil. The industry still has some logistical issues to resolve especially around pipeline capacity.

Lower prices for crude oil are likely to lead to higher volumes of production, not less by US producers. New wells may be put on hold as prices hold below $50 per barrel. There are some pipeline constraints that are expected to ease towards the end of 2019 which will also reduce price pressures (logistics discounts) on some US and Canadian producers. US Rig count may fall but as we saw earlier in 2016 with lower rig count, rig productivity tends to rise across US fields.

OPEC understands this and has responded. In its December 2018 meeting OPEC announced planned production cuts of 1.2 million barrels per day for the first six months of 2019. December quota for cuts was 800,000 barrels per day with Saudi production cuts estimated to range between 400,000 to 460,000 in December. The Kingdom added a little over a million barrels per day of supply post June 2018 in anticipation of US sanctions on Iran. They now plan to partly reverse the production surge. The cuts however exclude Libya (likely to add back stalled production due to field and pipeline security issues) and haven’t factored in resumption of supply from fields in Kirkuk in Kurdish Iraq.

Despite the size of cuts Saudi Arabia will still end up with higher output when compared to Saudi production levels at start of 2018. Same holds true for announced Russian production cut of 230,000 barrels per day. December 2018 Russian production stood at an all-time high of 11.49 million barrels per day. While the cut may bite, the bite is a lot less than what they gave away in 2016.

OPEC’s smaller members can see through the optics of the cuts. The most likely results of this bit of hand waving is likely non-compliance on part of smaller OPEC members. As Saudi and Russian cuts take hold, price will adjust briefly but the supply glut will not disappear. There are also questions about Russian compliance with the cuts based on their historical behavior. Dallas Fed’s energy charts for instance indicate that markets will reach balance somewhere in 3Q of 2019. Goldman Sachs in its January ’19 oil update also agrees that there will be ample supply in markets for the first two quarters of 2019.

All this is with the expectation that the demand side of this equation will behave. However, any disappointing news coming out of China, US or India is likely to impact prices and create additional pressure on both OPEC and non OPEC members to push production higher to meet revenue quotas.

Noise, bias and opinions

While the three don’t impact or move prices, they do shape perceptions and conversations. Opinions on direction of oil prices can be classified in three broad categories.

a) Prices are heading south in 2019. 2019 year is going to be a repeat of the slump oil prices faced in 2015-16-17. Analysts who opt to sit on this side of the table are rare these days.

b) Prices have finally found their true level. Prices are going to be range bound between low forties and high fifties for next two years (2019-20). Not as rare an opinion as (a) above but still not common.

c) This is just a temporary year end correction. As hedge funds book their losses or gains and close their trades markets will adjust upwards beginning January 2019. Celebrate as much as you want now but between OPEC cuts and limited buffer of spare capacity prices will head north again in 2019. This is the most common view in news and opinion pieces as we head into the new year.

The opinion you favor is a function of data you are looking at, news sources you follow and the particular brand of cool aid you favor. There is no directed intent to misguide or mislead the world, it just how your model is put together.

OPEC member countries. If you are an employee of the ministry of energy, petroleum products or planning at any of the OPEC members you are likely to belong to the third school. Rising oil prices make your job easier and your budgets hold true to their planned levels. Your national interest and your OPEC strategy would be focused on actions that would push oil prices higher. More dollars per barrel imply more dollars in the sovereign wealth fund and room to breathe on the current account front. It is also going to be difficult arguing with your Minister’s optimistic outlook on prices.

Trading desks. If you are a member of a commodity research or sales and trading desk at a leading investment bank or research house, your opinion is going to be a function of your trading positions. Traders have a four-hundred-year history of talking up their positions. They don’t necessarily do it maliciously but their positions reflect their world view. Right or wrong the world view seeps into conversations. While research functions do independent work and are strictly regulated it is difficult to ignore powerful opinions and quite often fairly logical arguments in favor of the original trade. Groupthink is a difficult force to resist. Hence if you are short oil, you are likely to support thesis (a) above. If you are long (c) is your game. If you have bet on short term volatility you would be happy with (b).

If you are in neither of the first two camps, have a strong dislike for OPEC, would prefer global economic growth over a similar downturn, are essentially a perennial optimist or simply like lower fuel bills you would be rooting for option a) or b).

Think through the impact of the same opinions when it comes to planning annual budgets at the largest crude oil producers in the world. If we expect balance in prices on account of already announced production cuts, would we factor in the impact of additional production cuts if required. We know that the Kingdom of Saudi Arabia does, but what about the other 5 producers on that list.