Disney’ relative financial performance

The Eisner and Iger eras.

Disney has been a household name for more than three generations. From my mother’s generation to my children’s children. While it stumbled and wandered a bit after the death of its founder the business has had two back to back magical runs of growth across 35 years. The first under Michael Eisner from 1984 to 2005 and the second under Bob Iger from 2005 to 2019. The 21 year Eisner era and the 14 year Iger era provide interesting contrasts to growth strategies for global consumer businesses.

The Eisner years focused on monetizing Disney’s existing content and character libraries, creating new ones under Disney Animation and building a more powerful platform for distributing and licensing Disney’s content. The Eisner team did this by recognizing the value of the character franchise Disney had inherited, taking Disney’s ambitions global, opening new parks in Europe, planning a new one in China and acquiring ABC / Capital cities and a host of other networks that brought the magical kingdom a steady stream of traffic.

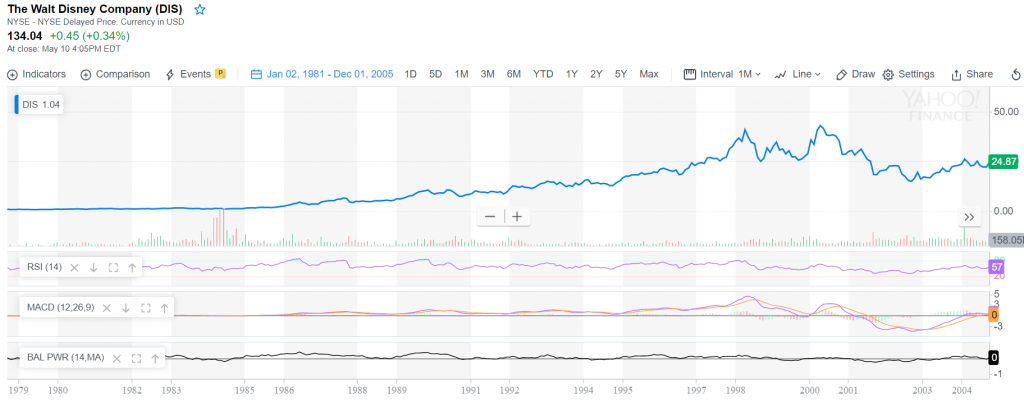

While Eisner’s era was not free of controversies, it saw Disney annual revenues rise from USD 1.5 billion to USD 31 billion in 21 years. Market capitalization over the same period grew from USD 2.8 billion to USD 57 billion. On a 2019 split adjusted basis Eisner took Disney stock from under a dollar a share to 24 dollars a share by the time he resigned.

Was that a big deal? Compare this performance to Bob Iger’s more recent 14-year reign. Bob took the original design behind Eisner’s model and refocused on Disney’s core. The ability to tell great stories and to attract large audiences, specially families. It looked at the biggest hole in that model (teenage boys, young adults and parents) and filled it with Pixar, Marvel and Lucas Films. Films that allowed parents to relive their younger Disney years. Iger also centered Disney’s vision on family friendly entertainment rather than just entertainment letting go of mediums that didn’t fit this format.

On a comparative basis Bob Iger took Disney from 24 dollars a share in September 2005 to 134.04 dollars a share as at close of market on 10th May 2019. Market cap grew from USD 58 billion to USD 241 billion over the same period. Both performances are remarkable given the context of their eras. Together they made it possible for Disney to be what it is today.

While Bob Iger era numbers lag behind Eisner’s growth figure, growing from a base of 60 billion dollars is a significantly more difficult challenge than growing from a base of a billion dollars. In addition to growing from a larger base the true value added by integrating Pixar, Marvel, Lucas Films and Fox is yet to be realized. With the launch of Disney+, Disney has yet another channel to embed its universe in the homes of ready audiences.

Disney – holding period return against peers and competitors

How has Disney done financially when compared to its peers. Cable and media industry in general are apt benchmarks and we know that Disney has done relatively well compared to traditional players in the industry. One challenge is that other than Comcast, NBCUniversal, Warner Brothers and most media studios are private entities or subsidiaries of private entities. One can still use proxies such as box office gross to drive distributions to the studios and other financial metrics. All of which indicate that on a relative basis Disney has done well over the last ten years.

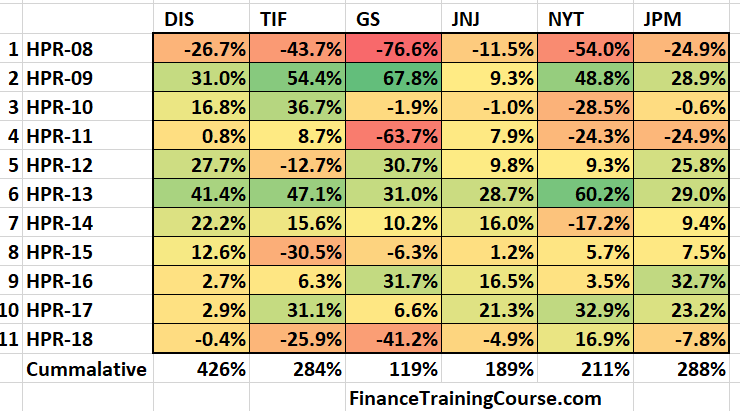

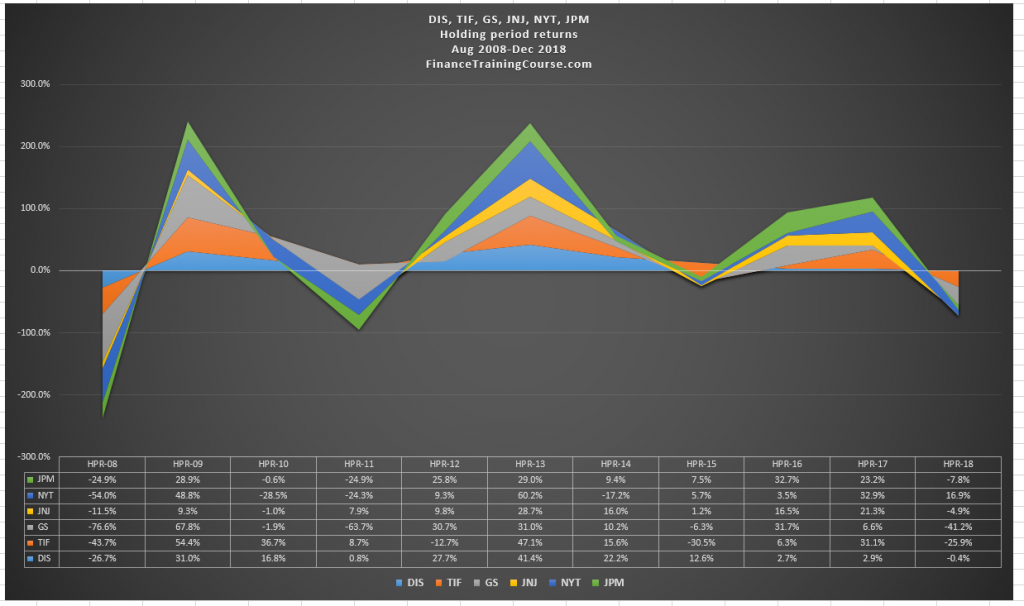

Beyond traditional competitors Disney has also done well against a number of defensive, retail and financial services giants. Names such as Tiffany, Goldman, Johnson and Johnson, New York Times and JP Morgan Chase over the last eleven years.

At first pass Disney appears to be a better defensive bet than both JNJ and Tiffany and a significantly better bet than both Goldman and JP Morgan Chase. Disney stands well even when we extend the securities universe to other well established names

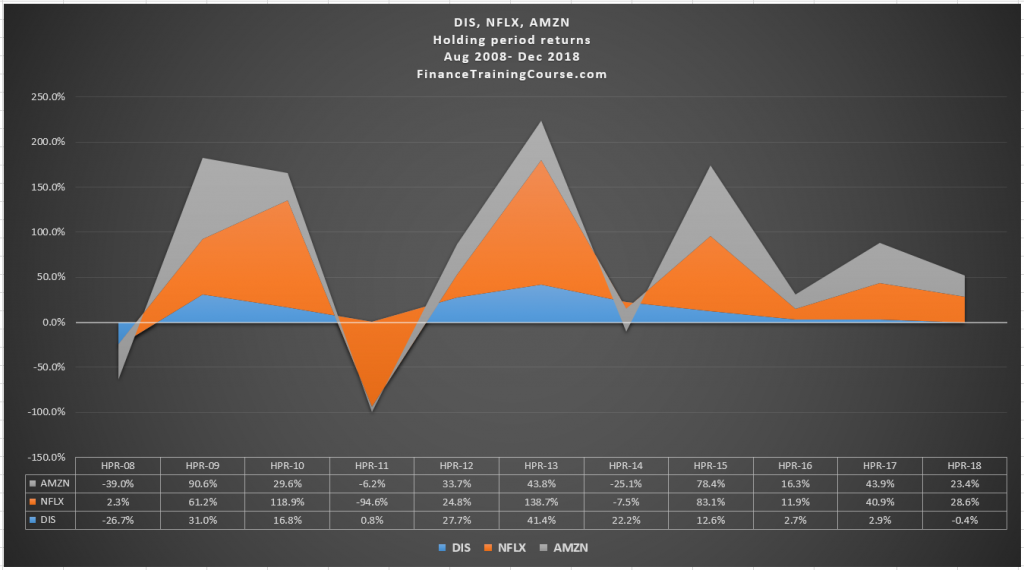

How about two direct contenders for the Disney throne – Amazon and Netflix? Two businesses with their own independent content generation and streaming platforms and a significant head start on the subscription front.

While we are at it how does Disney compare with the darlings of the tech industry in terms of returns as well as conventional star listed securities in the securities universe. If you were running an allocation model for personal or institutional investors, will Disney find a place in that universe?

When you read media commentary on Disney you cannot help but notice comparisons to Netflix and Amazon. Does this mean that beyond a content, media and consumer brand someday Disney may also be recognized as a tech giant riding on the shoulders of its streaming service? Or aspire to the same returns that Amazon and Netflix generate?

We don’t think so. Here is the evidence.

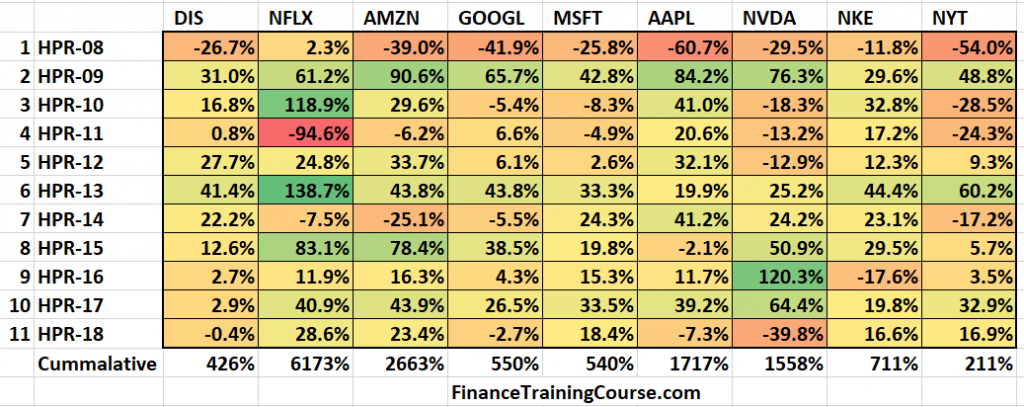

While Disney 426% holding period return over the last 11 years is certainly impressive, it pales in comparison to both NFLX and Amazon. The big surprise is how well it ranks against Microsoft and Google despite Disney’s own flat performance in ’16, ’17 and ’18.

The verdict

Disney’s strength remains its ability to tell great stories and attract new audiences to pay for that experience. While content distribution models get disrupted it doesn’t change the fact that the underlying commodity being delivered by new disrupted mediums will remain content. On that one measure Disney will rule supreme.

Within its traditional business lines and revenue segments Disney will continue to execute with excellence. These will remain the same – Media Networks, Parks and resorts, Studio Entertainment, Consumer product and Interactive media. There will be some shifting and rebalancing of revenues and profitability from Media Networks to Consumer products and interactive media but that won’t turn Disney into a technology company or get Disney to a point where it begins to boast of tech sector returns.

What does that mean for the Disney versus Netflix versus Amazon battle? Is Disney likely to make money down the road on Disney+?

Netflix is the 800 lbs. gorilla in this battle with its base of 149 million paid subscribers. Disney is the new kid on the block in the streaming wars. Amazon with its deep pockets, Prime subscription and an estimated 100 million Prime subscribers subsidizing Amazon video has a strong defensive position.

While Disney has fired its first salvo in the streaming wars by under cutting the competition on price, the odds for picking a winner in this race are still wide open. Netflix and Amazon have a choice. They can side step the price cut and let Disney establish a beachhead on the streaming front. Or they could tackle Disney head on?

The smart move is to let Disney battle it out with the long list of newer entrants committed to enter this space in the next two years. Once the dust settles and Disney has been bloodied, tackle it on the content front. Take the war to Disney rather than fight it on Disney’s term on your own turf. We all agree that Disney has a formidable content advantage. But will that be enough for butting heads with Jeff Bezos and Reed Hasting? Bob Iger has certainly done well in his 14 years at Disney. But how Disney fares in the upcoming streaming conflict will be his real test.

Disney against Amazon and Netflix

Disney against TIF, GS, JNJ, NYT and JPM

References

- https://flixed.io/golden-age-of-cord-cutting-over/

- https://gizmodo.com/why-disney-freaks-me-out-about-the-future-of-streaming-1834762436

- https://observer.com/2019/05/disney-plus-price-netflix-amazon-hulu/

- https://www.thedrum.com/opinion/2019/05/21/stream-wars-can-netflix-survive-the-disney-juggernaut

- https://www.cnbc.com/2019/05/10/disney-and-the-new-york-times-media-dinosaurs-staying-on-top.html

- https://edition.cnn.com/2019/04/16/media/netflix-earnings-2019-first-quarter/index.html

- https://www.marketingcharts.com/digital/video-107217