This case study outlines the timeline and consequences of the AML compliance violation by HBL and its New York branch and the resulting supervisory action taken by the NYDFS.

Overview

On 7th September 2017 Habib Bank Limited (HBL) and HBL’s New York Branch were penalized $225 million by the New York State’s Department of Financial Services (NYDFS) for non-compliance with and violation of New York’s state laws and regulations on combating money laundering, terrorist financing and illicit financial transactions as well as violation of a subsequent Written Agreement and Consent order issued by NYDFS. The non-compliance had been systemic, with significant deficiencies noted in 10 consecutive examination cycles conducted by the NYDFS since 2006.

Initially subject to a maximum possible penalty of $630 million for 53 violations stated in the August 2017’s Notice of Charges issued by the DFS, the matter was settled out of court for a third of the amount. HBL offered to voluntarily surrender its license to operate its New York branch which was accepted by the NYDFS subject to certain conditions including an on-going independent expanded lookback transaction and OFAC review and a safe and orderly wind-down of its affairs in New York.

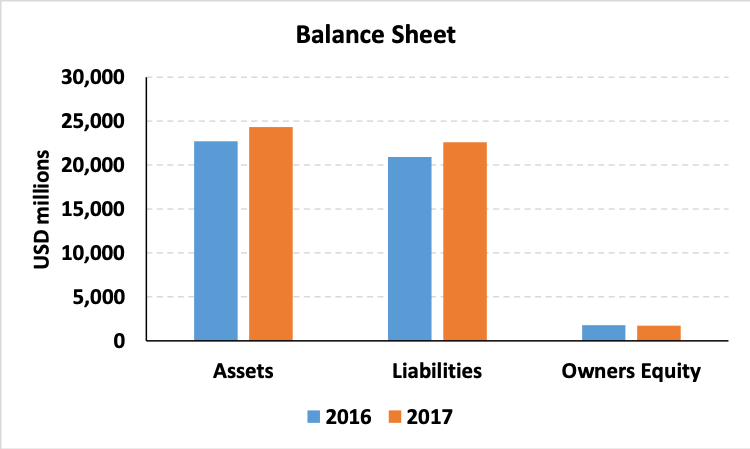

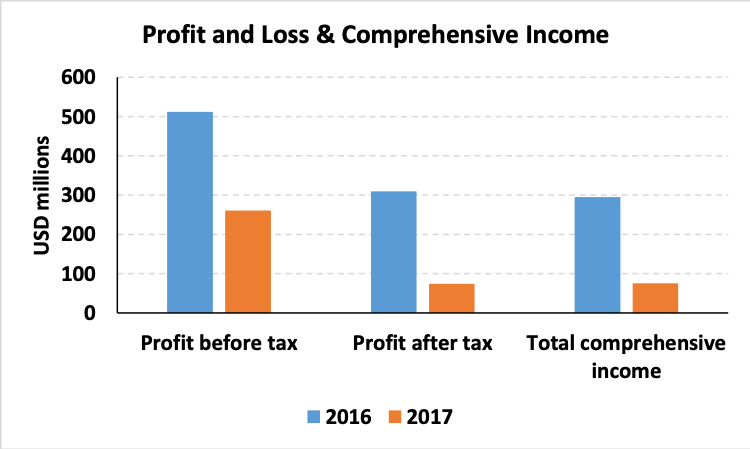

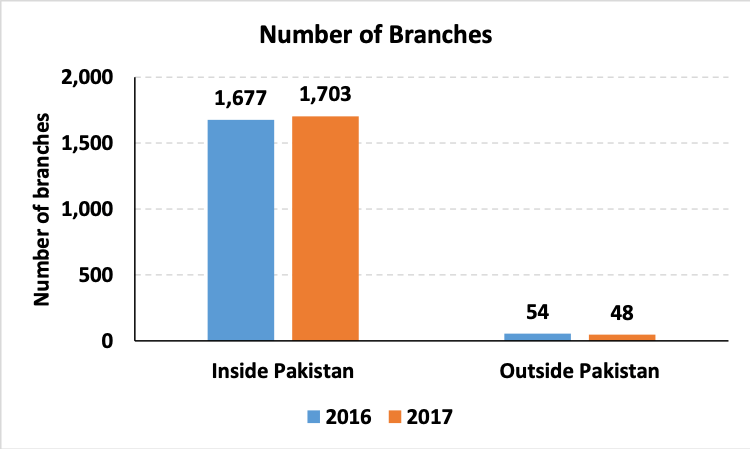

HBL’s Financial Profile – Pre & Post AML Compliance Violation – 2016 Vs 2017

The following snapshot uses the 31st December 2017 Financial Statement. It may be noted that the 2016 and 2017 year end values were restated in the 31st December 2018 Financial Statements.

Following the Consent Order and penalty, HBL’s profit took a one time hit reducing earnings by 50% on a before tax basis and by 75% on an after tax basis.

As of 31st December 2016 HBL had an international footprint in 25 countries on account of its branches, affiliates, subsidiaries and representative offices, while as of 31st December 2017 it had a presence in 24 countries due to the representative office closure in Iran following security concerns. The number of people employed in the institutions stood at 17,220 and 18,085 as of year ends 2016 and 2017 respectively.

Timeline to Surrender & Penalty

1978: Habib Bank Limited was licensed to operate a foreign branch by the New York State Banking Department (predecessor of NYDFS). The branch was established primarily to offer US dollar clearing services. It was the HBL’s only US branch.

February 2004: HBL was privatized with managing control handed to the Aga Khan Fund for Economic Development (AKFED) which has maintained a shareholding of 51% in HBL. It shares are publicly traded on the Pakistan Stock Exchange.

19th December 2006: Written Agreement between HBL & its New York Branch with the Board of Governors, Federal Reserve Bank of New York & New York State Banking Department was issued to address deficiencies in the Branch’s BSA/ AML compliance function. The agreement required HBL to:

- Develop Bank Secrecy Act (BSA)/ Anti-Money Laundering (AML) & Office of Foreign Assets Control of the US Department of the Treasury (OFAC) compliance programs that would enhance its internal controls, policies and procedures and ensure an effective implementation and maintenance of its BSA/ AML & OFAC compliance function

- Enhance its Customer Due Diligence (CDD) program to ensure that suspicious activities were reported on a timely, accurate and complete basis

- Independently test its branch’s BSA/ AML compliance

- Outline the training that it would provide to its personnel on BSA/ AML policies & procedures, identification and reporting of suspicious activity and legal & risk management processes

- Test and implement the branch’s proposed transaction monitoring system.

- Conduct an account and transaction review by an independent firm for the period 1st January 2005 to 31st December 2005 to identify any suspicious activity that may have gone unreported during that period.

- Submit progress reports to the department on a monthly basis.

2007-2015 Examinations: The annual examinations revealed that BSA BSA/ AML & OFAC compliance programs broke down repeatedly. Further, violations of the 2006 Written Agreement and the state laws were discovered in every annual examination cycle, with the exception of the 2009 cycle.

15th December 2015: Consent Order & parallel Consent Cease and Desist Order issued by the NYDFS, following further deterioration in HBL and HBL New York Branch’s risk management & BSA/ AML compliance functions. The deficiencies were identified in the annual examination cycle conducted by the Federal Reserve Bank of New York and the NYDFS.

It was noted that the bank had not yet achieved compliance with the provisions outlined in the 2006 Written Agreement and therefore was in violation of the applicable federal and state laws, rules and regulations. The consent order called for the following remedial actions:

- Enhanced management oversight and a sustainable corporate governance framework to ensure that the bank was in compliance with BSA/ AML requirements & OFAC regulations

- A BSA/ AML compliance review by an independent consultant to assess the New York branch’s compliance function

- A revised written BSA/ AML compliance program

- A written enhance CDD program

- A written suspicious activity monitoring and reporting program

- A Transaction & OFAC Sanctions review by an independent consultant of the branch’s dollar clearing transactions conducted over the period from 1st October 2014 to 31st March 2015 to determine if suspicious & prohibited accounts & transactions were reported by the bank or whether there were approved transactions violated or were inconsistent with OFAC regulations.

- A restriction on the growth of the branch’s aggregate US Dollar clearing activities

- Enhanced compliance with OFAC regulations

2016 Examination: NYDFS and Board of Governors of the Federal Reserve Bank of New York conducted another examination of the branch’s BSA/ AML compliance function for the period closing 31st March 2016. The examinations found that:

- The Head Office screening & New York Branch risk management and compliance function to be dangerously weak with inadequate BSA/ AML safeguards in place despite 10 prior examination cycles

- Controls to mitigate and manage the BSA/ AML and OFAC risks had still not been implemented

- Training, CDD, EDD, corporate governance and management oversight were still insufficient

- Its transaction monitoring systems were inadequate. They failed to trigger nesting activity, or wire-stripping or to screen all activity of a particular counterparty due to variations in the name. In other instances where transactions generated alerts, they were cleared as some characteristics suggested false positives even though other characteristics, like missing beneficiary names, should have suggested a further review.

- Its OFAC sanctions screening was lacking for some of its product offerings

- Internal audit rating methodology and data systems were weak

- Some of the significant BSA/ AML violations that were discovered in the Examination are mentioned below:

- Facilitated billions of US dollar transactions with Al Rajhi Bank, a private Saudi Bank having reported links to al Qaeda

- Facilitated unsafe nested activity by not adequately identifying customers of Al Rajhi Bank that were using the Al Rajhi account at HBL’s New York Branch to transfer funds through New York

- At least 13,000 transactions which omitted originator and beneficiary information were approved. If the relevant information were included, these transactions would have been screened/ flagged as prohibited transactions or transactions with sanctioned countries or persons

- Improper inclusion of sanctioned persons and entities on the bank’s very low risk “good guy” list led to $250 million in transactions that were not reviewed or screened. These included transactions carried out by persons with identical entries on the Specially Designated Nationals and Blocked Persons list (SDN list) including a terrorist and an international arms dealer among others.

As a result of this examination, the branch was assessed NYDFS’s lowest possible rating, a score of 5 (unsatisfactory). In general financial entities assessed a score of 5 by NYDFS may be subject to regulatory actions, such as monetary fines, and license suspension & revocation.

24th August 2017:

- In light of the discoveries made following the 2016 examination cycle, the NYDFS issued an Expanded Lookback Order for the 2015 Consent Order’s Transaction and OFAC review. Two additional periods 1st October 2013 to 30th September 2014 & 1st August 2015 to 31st July 2017 were to be included for the independent consultant to investigate.

- Surrender Order issued to provide HBL with a 30 day period within which it could notify its surrender of its New York Branch license subject to certain conditions. If HBL did not voluntarily surrender its license, the NYDFS could seek to have it revoked in a hearing.

- Notice of Hearing and Statement of Charges for 53 separate violations that had occurred since 1st January 2007 of the New York Banking Law, the 2006 Written Agreement & the 2015 Consent Order. The Superintendent of Financial Services sought a civil monetary penalty of up to $629.625 million from HBL and its New York Branch for these violations.

31st August 2017: HBL offered to surrender its New York Branch license in accordance with the conditions of the Surrender Order and to commence the safe, sound and lawful wind-down of its affairs with the assistance of an independent consultant according to the conditions specified by NYDFS.

7th September 2017: Consent Order

- HBL was awarded a $225 million civil monetary penalty as part of the out of court settlement arrived at with the NYDFS. The penalty was payable within 14 days of the order.

- Agreement to fully comply with the Expanded Lookback Order.

- No further action would be taken against HBL or its Branch subject to compliance with the Order.

- While the terms and conditions of the prior 2006 Written Agreement & 2015 Consent Order were suspended with the surrender of its branch’s license, they would remain in full force and effect and would need to be fully complied with should HBL ever consider re-establishing itself again within the State of New York.

Other Consequences

31st December 2017:

- Nauman K. Dar, the President and CEO of HBL at that time, resigned from HBL’s Board on 20th October 2017 and retired on 31st December 2017.

- The 31st December 2017 Annual Statement mentioned that the U.S. Office for the Eastern District of New York, a component of the U.S. Department of Justice (DOJ), had sought documents in relation to the compliance with anti-money laundering laws and the Bank Secrecy Act from the bank. Findings from this inquiring were still pending according to the 31st December 2018 annual report.

30th April 2018: Muhammad Aurangzeb, former CEO Global Corporate Bank – Asia Pacific at JP Morgan, appointed as the President & CEO.

Post NYDFS AML Compliance Sanction Challenges

Outside of the challenges with NYDFS, HBL had a great deal going in its favor in 2015-16. Historical goodwill, a solid deposit base built upon the legacy of loyal customers, supportive and educated owners and board members, a dynamic and experienced management team, creative branding and positioning, no shortage of talent and one of the most well respected and regarded banking franchise in the country. Partially owned by the Aga Khan Foundation for Economic Development, HBL was consistently recognized as one of the better-managed banks in Pakistan.

The initial news of NYDFS ruling was received with shock. As is the case with US sanctions against Asian and European institutions, most followers of the bank immediately thought of a hidden bias or agenda on part of the regulator. But all this was before the detailed findings and hearing records, the transcripts and the consent decree were released. When the record became public, sentiments changed immediately to how could HBL executive team be so blind to the risk raised by NYDFS over 10 consecutive examinations.

Post 2017 the bank rolled out enhanced screening and compliance reviews across its customer network that created significant friction within its core customer base. Specifically, at risk were pensioners and retirees, who couldn’t comply with the new enhanced documentation requirements. Retirement certificates, final settlement documents, proof of post-retirement source of income, repeated biometrics and account debit blocks on 70 and 80-year-old grandparents don’t really lead to good advertising copy. Simple issues became customer service nightmares because knowledge of workarounds, exceptions and the compliance process were not widely shared or disseminated across the branch network. Centralized operations became a bottleneck in resolving customer challenges linked to documentation and paperwork.

The bank also managed to turn off remittance customers and dollar account holders who found the new requirements, processes and associated delays awkward and cumbersome to work with. This was tragic in a way given the effort and time the bank had invested in branding itself as a forward-looking progressive bank and the infrastructure to support that position. The real damage wasn’t the USD 225 million penalty HBL paid to NYDFS. It was the change in HBL’s internal outlook and psyche. Instead of facilitating and attracting the next generation of customers that would drive profitability for decades, the bank unwittingly turned on the same community.

While it still retains its position as one of the largest banks in Pakistan, the NYDFS compliance disaster shows how dramatic an impact such an event can have on an institution long after the compliance penalty is paid and settled. The scars remain and the shadows only lengthen with time.

References:

- NYDFS Enforcement Action: Settlement Agreement with Habib Bank Limited and Habib Bank Limited, New York Branch – September 7, 2017

- NYDFS Enforcement Action: Notice of Hearing and Statement of Charges to Habib Bank Limited and Habib Bank Limited, New York Branch, August 24, 2017

- HBL Annual Report 2017