Credit Management? What does the credit risk management function do?

How does the credit risk management function work at a bank? What are the different layers and sub functions involved in credit risk management?

What follows is a transcript of a lecture on credit risk management delivered to MBA students in Singapore at the SP Jain campus. A high level review of the credit management function at a bank in a 90 minute lecture.

Yesterday we looked at the steps involved in setting up and running the derivatives book function at a large investment bank. Today we are helping the same large bank set up their brand new credit risk management function in Asia. As part of their big move they are looking for someone to head and design their credit risk platform. You are leading candidate for the role, they have asked you a simple question highlighting your vision for the function? Where would you start?

Figure 1 Credit Management Life cycle

You have to begin with how risk is booked on the bank balance sheet and how it flows through the different layers of the credit management function across its life cycle. Which means we have to go all the way to the relationship managers who bring and book assets to the bank balance sheet, end with credit admin if the loan performs, or special assets or recovery if it does not.

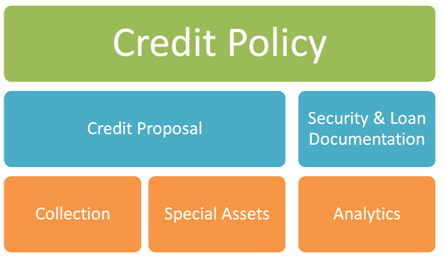

Credit management. Credit Proposal

What do relationship managers look at? If I asked you to lend me a million dollars and you are my relationship manager, where would you start? What would you look at? What information would you need and how would you convince the lending function at the bank to approve my request? Let’s make a list of relevant data that we would need to evaluate such a request.

- My credit history as a borrower as an individual or an entity in the past with this bank or other banks.

- The nature of my business and the industry segment.

- The outlook for that segment as well as the entire economy/region.

- The reason why I need to borrow money.

- My plans for usage of the proceeds from the loan and the impact of that plan on my ability to repay the loan.

- My sources of loan repayment and my ability to repay the amount borrowed.

- Any security or collateral that I can pledge to the bank to secure my loan.

As a relationship manager I would look at all of this and more and prepare a document called a credit proposal. A credit proposal documents all of the above and makes a recommendation in alignment with the credit policy of the bank to lend or not lend, approve or not approve the credit proposal. While the universal name is credit memo, credit proposal or CP for short, we also recognize it by Application for Limits (AFL), limit approval or credit application.

Credit Management. Credit Policy

When a credit application is received by the bank, it cannot just walk in through the door. It generally has a sponsor (the relationship manager) or a champion and it must make its way past a gate keeper called the negative list. A negative list is a list of attributes, the presence of which will guarantee the kiss of death for a credit applications.

At any given point in time a bank may decide that a given sector or segment is too risky (or too popular) because of their prior experience (or limits) or an industry wide trend, capital requirements for products. They may also identify security or collateral which is not acceptable for securing a loan (given an ability to collect, repossess or liquidate) or attributes of owners, shareholders or sponsors that the bank has decided to not take a risk on.

Figure 2 Credit Management & Credit Policy

This negative list plus a number of additional credit selection/underwriting decisions are documented in the credit policy of the bank. The credit policy document defines what is acceptable credit for the bank, the information requirement for a credit proposal, the format of a borrower fact sheet, the reporting requirement for the credit risk management function and much more.

Credit policy documents also come in two flavors. The lean and mean policy version that only focuses on policy decisions as well as the thick brick manuals that also detail policy implementations procedures and processes. There would generally be separate credit policy document for commercial, SME, retail and consumer businesses, while product specific credit policy issues may get addresses as part of the program or product guides.

A CP is also influenced by central bank policy with respect to specific segments and products. For example in developing, emerging and frontier markets a credit policy document is generally in close alignment with the national economic policy of the government and the central bank. However the ownership of the credit policy document rests with the head of credit function but it is approved and validated by the board of directors and reviewed and audited by the central bank supervision team every year.

As a relationship manager it is required for you to be familiar with credit policy requirements of your bank so that you don’t waste your time in preparing proposals that will not make it pass the initial filtering list.

Credit Management. The underwriting and approval decision

If you are lucky enough to make your proposal pass the initial filters and the requirements specified in the credit policy, your job just got started. Your proposal is now safely sitting on the desk of the credit portfolio analyst who is going to review it and make his recommendation. The analyst will review the recommendations made by the relationship manager as well as the branch and if the proposal meets all the requirements needed to approve the loan, the analyst will make a positive recommendation and forward the proposal to the next level in the chain of approval. If the proposal is deficient on account of a specific factor, in most cases the proposal won’t be declined outright but sent back to the relationship manager with feedback on the deficiency. Once the deficiency is fixed, the cycle would restart again at the credit portfolio analyst desk.

A large part of the analysis is based on the original need for the loan, the product being used to finance it, sources of value creation, sources of repayment, security and collateral, margin, documentation and guarantees by sponsors, shareholders and directors. The analysts also look at the capacity of both your balance sheet as well as your P&L to bear the loan and debt servicing capacity.

Credit Management. Post approval life cycle of a loan

Once the loan is approved, the credit proposal moves through the next stages in the life cycle. The first post approval step is loan documentation. This is the step where the loan offer or term sheet is shared with the client and is returned with his acceptance.

The term sheet specifies the loan terms and conditions (loan covenants), the specification of collateral, the nature of the pledge, pledge documentation, loan servicing requirements, late payment penalties, arbitration, collection and repossession clauses. It also includes the legal documents required for registering a charge against the asset of the entity being financed with the regional or national charge registration authority (Corporate Law Authority, the Registration of companies or the Securities and Exchange commission).

Figure 3 Post loan approval credit life cycle

Once these two steps are completed the loan is ready to be disbursed and the consumption and repayment cycle of the loan starts. Throughout the life cycle the relationship manager for the client plays a central part since in addition to the bank he has the most data about the relationship and its prospects at any given point in time.

Figure 4 The role of a relationship manager

However while the credit management function can use that insight, it cannot solely rely on the relationship manager to control the risk inherent in a given credit relationship because there is an inherent conflict of interest. Therefore the credit management function relies on a mix of branch level data as well as its own analytics to manage, control and run the function.

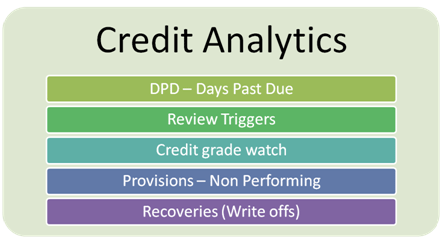

Figure 5 Credit management – credit analytics

These analytics include:

- a breakdown by product, region, branches and segments of the days a payment is overdue (days past due or DPD analysis) across the entire banking franchise and how it compares with the overall industry average

- Relationship review triggers that serve as leading indicators of blood in the water such as issues with margins, deposits, transactions, industry slowdown, credit downgrades, client specific chatter on the banking system grapevine and default on other banking relationship

- Client or industry specific credit downgrade by internal or external credit rating systems

- Changes in sector, segment, region provisions or loan classifications

- Changes in recoveries and write offs.

- Bank exposures concentration across sectors, segments, products, markets and clients

The DPD tracking piece is the most crucial analytic generated by the credit management function. It is used not just in collections tracking and client management but also in provisions projections and capital management. But the source and control of DPD data is crucial. If the credit management function relies on branches to generate and compile DPD data they are just asking for trouble. For DPD data to be reliable and effective it should be generated automatically without manual intervention by any concerned or related party.

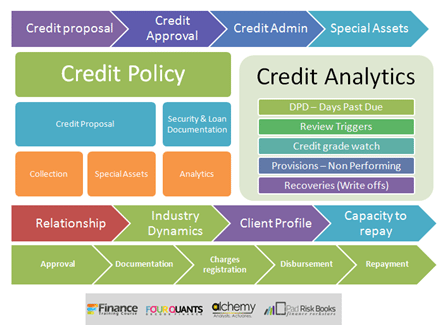

Credit Management – The 10,000 meters view

From policy to proposal, from proposal to approval, from approval to disbursement, from disbursement to analytics, the credit management function seems to have its fingers everywhere. If you run the credit management function you need to be comfortable with all the dimensions of the function.

The challenge in credit risk however is the inherent conflict built in the nature of these dimensions. Proposals and approvals are market driven. Documentation and charges are legal. Analytics are performance and behavior driven. Provisions, recoveries and special assets use a completely different language and rely on negotiations, positions, give and take. And the whole house of card is linked to economic outlook and growth. Build a book of assets going into a recession and the best of underwriting will still face challenges; build a book growing into a growth cycle and a number of your mistakes may be forgiven.

So what should you have on your profile before you apply for that head of credit risk role. Experience in both business development and corporate banking as well as special assets and credit administration. Ideally some technology and Analytics so that you don’t get taken for a ride by technology vendors. An ability to read the economic cycle as well as a knack for identifying which relationships to save and which to cull.

Figure 6 The credit risk management function – 10,000 meters view

The challenge is that conventional banking experience does not allow the cross pollination of functions required to effectively run a credit risk management group. If you come from Special Assets or Credit Admin, you stay with SAM or CAD. If you get into legal and documentation, you tend to stay with legal and documentation. And technology and analytics are generally alien to your DNA unless you have had a brush with engineering or applied mathematics in an earlier life.

If you liked this post, here is a list of additional readings that would fit right in.

- What is Risk? What is Risk Management?

- Stop Loss Limits – Review triggers

- Value at Risk models

- Advance Risk Management Workshop – Singapore

- Risk Models in EXCEL