Advance Risk Management Models (aka RM II) course is a 1 credit course taught at the SP Jain Campus in Dubai and Singapore by Jawwad Ahmed Farid. A variation of this course was delivered (22-29th August 2012) at the SP Jain Dubai Campus by and in Singapore (mid October 2012). The next scheduled delivery is in first week of January 2013 in Dubai.

The course builds up on the work done in earlier MBA specialization courses (Risk Management I, Derivatives I and Derivatives II) conducted for regular and executive MBA students. The focus is on risk model building and practical applications in the banking and investment management space using hands on Excel. The course reviews and builds on risk management models from the world of portfolio optimization, derivatives pricing and hedging, hedge optimization, regulation, credit risk and probability of default estimation.

Update: The new Monte Carlo Simulation how to reference, Delta hedging using Monte Carlo simulation and the Delta Hedging Cash PnL Simulation posts are now up.

Advance Risk Management Models – Course Prerequisites

Students are expected to be comfortable with materials covered in Risk Management I and the Derivatives I and II course series. See the Reference site for Risk Management I for a quick Review of risk management concepts as well as the Derivative pricing crash course for dummies. Without the relevant background you are likely to struggle so familiarity with the shared material is highly recommended.

Advance Risk Management Models – Course Plan

Here is the lesson plan for seven days of classes. The training workshop classes run for 150 minutes every day with homework assignments due for submission the next morning. As course material is documented and available for release the core theme links on this page (below) will be updated.

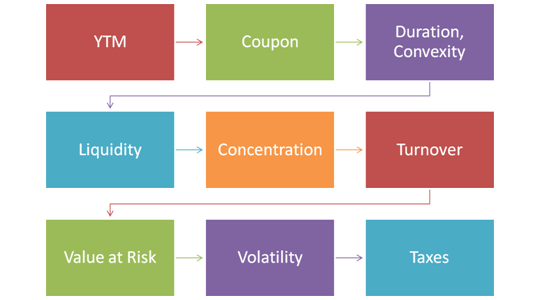

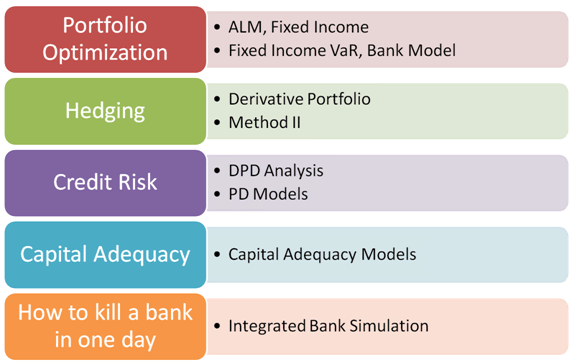

Advance Risk Management Models – Core Themes and study notes

- Fixed Income Value at Risk (VaR) Calculations for fixed rate bonds

- Fixed Income Investments Portfolio Optimization Model using Excel Solver

- Implied volatility, a simple introduction

- Delta Hedging introduction

- Delta Hedging European Calls and Put Contracts using Monte Carlo Simulation – new

- Delta Hedging Cash PnL Simulation – new

- War on Greeks – The weekend Option Greek Challenge – new

- Option Greek Crash Course – Delta, Gamma, Vega, Theta & Rho – new

- The evolution of banking regulation – From Reg Q to Basel II

- A review of bank regulation and why it really doesn’t work.

- Why does bank regulation fail? The Kill a bank in one day simulation – new

- Basel II – A quick introduction & walk through

- Basic credit analysis and models

- Probability of default calculations using the structured (Merton’s) approach

- Integrating funding, liquidity, ALM, credit allocation, capital adequacy and probability of shortfall.

- Building a liquidity risk management model for a bank under ICAAP & Pillar III reporting requirements

- Liquidity Stress Testing a Fixed Income Portfolio – new

Course note in the form of html posts are available for free. Downloadable pdf files and excel templates are available for purchase separately from our online store.

Final Exam – Practice Test Question and Solved Solution

The Prime Brokerage – Margin Lending – Margin Risk Management Case Study – new

Risk & Treasury Case Studies

Comments are closed.