Building implied and local volatility surfaces in Excel tutorial – coming soon

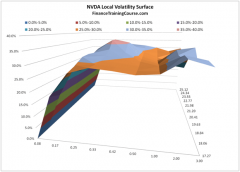

2 mins read Volatility surfaces – everything you ever wanted to know but were afraid to ask. Volatility Surfaces, for an option pricing

2 mins read Volatility surfaces – everything you ever wanted to know but were afraid to ask. Volatility Surfaces, for an option pricing

4 mins read While we have shared a great deal about Simulation Modeling and Analysis on this blog, over the years, I felt

< 1 min read Before you begin there are two Black Scholes background posts that you will find useful in deciphering the logic behind

5 mins read Simulating Commodity Prices Our course on Building Monte Carlo Simulators in Excel and related available-for-sale excel examples for Commodities, Currencies

3 mins read On the other hand N(d1) will always be greater than N(d2) because in linking it with the contingent receipt of stock in the Black Scholes equation, N(d1) must not only account for the probability of exercise as given by N(d2) but must also account for the fact that exercise or rather receipt of stock on exercise is dependent on future value

< 1 min read 1. COURSE OBJECTIVES At the end of this workshop the participants will be able to: Construct the par, zero coupon