Collateral Recognition and Counterparty Credit Risk

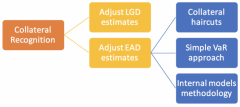

6 mins read In the previous post we reviewed the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches

6 mins read In the previous post we reviewed the credit risk requirements under the internal ratings based (IRB) and advanced measurement approaches

< 1 min read A look at how stress test shocks are applied to various elements of the profitability analysis to determine their impacts on the profitability of the bank’s loan portfolio.

3 mins read In this post we discuss one way of stress testing a rating grades transition matrix. The stressed transition matrix will then be used in the other credit risk quantification calculations. The revised results will be compared to the original credit risk quantification calculations to determine the impact of the stress test.

< 1 min read In this post we will consider how to derive expected classification rates for “current” customers of a loan portfolio. This is used to calculate the expected “current” customers who will be classified within the next period, which will in turn be used in the quantification process of credit risk under the Internal Capital Adequacy and Assessment Process (ICAAP).

< 1 min read One way of stress testing credit risk under the Internal Capital Adequacy and Assessment Process (ICAAP) is to stress test the rating grades transition matrix. In the post below we will first look at how a rating grades transition matrix is constructed.

< 1 min read One way of stress testing credit risk under the Internal Capital Adequacy and Assessment Process (ICAAP) is to consider percentage falls in the Forced Sale Value (FSV) of mortgaged collateral which is discussed below.