CIR Model – Simulating the term structure of interest rates

2 mins read Earlier we had estimated the parameters of the Cox-Ingersoll-Ross (CIR) model from market data. We now apply these estimated parameters

2 mins read Earlier we had estimated the parameters of the Cox-Ingersoll-Ross (CIR) model from market data. We now apply these estimated parameters

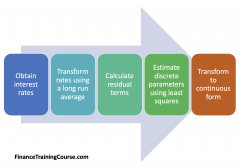

2 mins read In this post, we explore CIR Model parameter estimation. In other words, we consider how to calibrate the Cox Ingersoll

2 mins read In the second stage of the construction of the Black-Derman-Toy (BDT) one factor interest rate model in EXCEL we will

2 mins read This is the first of seven posts where we will be considering the step- by- step process of building the

2 mins read The Black Derman Toy model Excel implementation guide. A one factor interest rate model and some simplifying assumptions made in its

3 mins read The prerequisite for this course is the first course on pricing interest rate swaps. Online Finance – Pricing Interest Rate