Risk Management Framework for the Crude Oil & Petrochemical industry: Course Guide

< 1 min read A short six session introduction to a risk management framework for the Oil, Gas and Petrochemical industry focused on managing

< 1 min read A short six session introduction to a risk management framework for the Oil, Gas and Petrochemical industry focused on managing

5 mins read Risk models only have value if they are used effectively in combination with limit management and control process. While a

3 mins read A VaR based model can be extended to frame a number of questions for commodity consumers concerned about extreme price

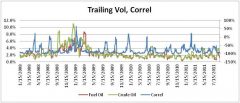

6 mins read This paper presents an extension of well accepted risk models in the financial services space to the risk management needs of the oil, gas and petrochemical industry in the region. We primarily extend the Value at Risk (VaR) framework and apply it to estimating refinery margins and inventory losses using crude oil price volatility as an input.

3 mins read Good Data and a first look at models The second element in our list deals with data and models. While

4 mins read A policy document identifies roles, responsibilities and occasionally the outline of a process to review, set and evaluate limits. It