Target Redemption Forward (TARF) Pricing Models in Excel

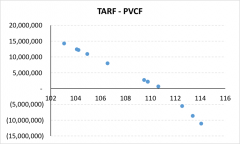

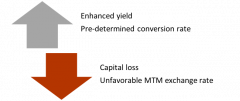

5 mins read Our two part series on TARF pricing models begins where we stopped with our analysis on TARF hedge effectiveness. We

5 mins read Our two part series on TARF pricing models begins where we stopped with our analysis on TARF hedge effectiveness. We

5 mins read Dual Currency Deposits (DCD) are structured products that allow an investor to earn an increased interest rate as compared to

11 mins read Your challenge working as a treasury professional is to take this term sheet and turn it into this payoff profile. If you do this successfully, you would do exceedingly well because you would understand what the counterparty, what the competition sitting on the other side has done by combining A+B+C. You would read this structure and immediately know that they have taken one part A, one part B and one part C and have sold the customer something called D. But if you can’t this term sheet and translate it into this diagram then you will always be clueless about what exactly has gone into D. And if you are clueless about what has gone into D you can’t price it. If you can’t price it, you can’t value it. If you can’t value it, you can’t compete against it.

8 mins read To summarize, the principle objective of estimating the amount at risk in each of these transactions is to determine how the transaction should be structured and what would be the impact of the structure on cost both out of pocket and explicit cost as well as implicit cost and what is the long range impact on the customer’s portfolio and profile of the structure that you have suggested.

3 mins read August 2007 – October 2007: Goldman Sachs asks AIG to post additional collateral in view of the falling market value

6 mins read AIG Financial Productions Corporation (AIG FP) a subsidiary of AIG issued and traded credit default swaps. These non-traditional insurance instruments