Duration and Convexity for US Treasuries

4 mins read To demonstrate how to calculate Duration and Convexity for specific US Treasuries we select instruments from recent US Treasury bill,

4 mins read To demonstrate how to calculate Duration and Convexity for specific US Treasuries we select instruments from recent US Treasury bill,

2 mins read Other Limits Duration Limits Duration measures the sensitivity of the price of the product/ value of the portfolio to changes

2 mins read Bond Convexity calculation example A working example of bond convexity and sensitivity calculation. Earlier we had reviewed the calculation process

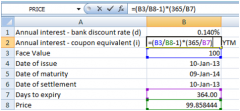

< 1 min read A working example of effective duration calculation. Earlier we had reviewed the calculation process for Macaulay and Modified Duration. In this

2 mins read This post presents a working example of Macaulay & Modified duration calculations. Earlier we had considered the importance of the Duration

4 mins read A normal shaped price-yield curve, such as the one given below, suggests that a bond’s price may not increase by