Asset Liability Management Training Guide. 3rd Edition.

The brand new, revised 3rd edition of the ALM Study Guide is out. With 190 pages, 189 figures and illustrations, the new edition weighs in at thrice the size of the 2nd edition and spends more time on building a stronger foundation for ALM.

Download the detailed table of content and list of figures and illustrations.

For existing customers if you have purchased a copy of the ALM crash course, 2nd edition at anytime please drop us a note for a complimentary download link to the 3rd edition.

Based on our most popular download the ALM Crash Course, the 3rd edition now includes new sections on yield curves, duration and convexity examples, a history of interest rate shifts and default ALM responses to changing interest rate expectations. We have also added new annexures on calculating VaR for fixed income bonds, liquidity stress testing fixed income portfolios and creating ALM maturity pools for retail and SME customer and product portfolios.

A detailed hands on section reviews building ALM reports including:

- Net interest income at risk

- Earnings at Risk

- Market Value of Equity at Risk

- Price and Maturity Gap

- Balance Sheet Duration Gap Analysis

Summarized Table of content

- ASSET LIABILITY MANAGEMENT

- HOW DO BANKS MAKE MONEY?

- ASSET LIABILITY MANAGEMENT

- DURATION AND CONVEXITY

- A VISUAL HISTORY OF US TREASURY YIELD CURVE SHIFTS (1978 – 2014)

- BANK ASSET LIABILITY MANAGEMENT (ALM) STRATEGY REVIEW

- ALM ASSUMPTIONS REVIEW

- ALM TWEAKS & HACKS

- BUILDING MATURITY & LIQUIDITY PROFILES FOR DEPOSITS AND ADVANCES FOR ALCO, LIQUIDITY COVERAGE & ICAAP REPORTING.

- ALM RISK MEASUREMENT TOOLS

- APPLICATIONS

- FIXED INCOME INVESTMENT PORTFOLIO MANAGEMENT & OPTIMIZATION

- LIQUIDITY RISK MEASUREMENT TOOLS

- LIQUIDITY MANAGEMENT

- LIQUIDITY STRESS TESTING A FIXED INCOME SECURITIES PORTFOLIO

- WHY DOES BANK REGULATION FAIL?

- BOND RISK: CALCULATING VALUE AT RISK (VAR) FOR BONDS.

- A METHODOLOGY FOR SUMMARIZING & POOLING RETAIL AND SME DATA.

Sample extract from introduction

As interest rate change over a period of time, the interest rate spread widens (increases) or tightens (decreases). Even with little volatility in rates, spreads can still change significantly if interest rates move in different directions for assets and liabilities or across maturity tenors and buckets.

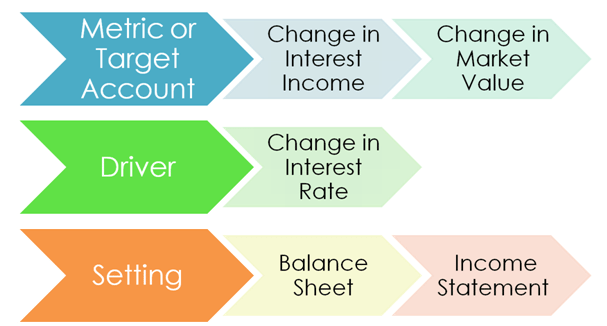

Figure 1 The ALM discussion summarized

Changes in interest rate spread have a direct and significant impact on bank earnings. Which is the reason why bank boards, regulators and industry analysts are interested in financial disclosures that clearly show earning sensitivity to expected interest rate changes in the near term. Combined with an interest rate outlook for the next few quarters, most boards can get an indication of earnings direction and use that to manage analyst and shareholder expectations.

Over the years the industry has fine tuned the usage of reporting tools that focus on the impact of interest rate changes on earnings. While Asset Liability Management (ALM) has a much broader mandate, earning sensitivity reporting is now a core part of the monthly ALM discussion during executive committee meetings.

In addition to earning sensitivity ALM reporting also looks at funding (financing), refinancing and liquidity and contractual maturity mismatch risk. To understand these reporting tools we need to get comfortable with three key drivers of the ALM function.

a) The shift and changes in interest rates,

b) The structure of a typical bank balance sheet, and

c) The interaction of (a) and (b) above and its impact on both earnings and shareholder value.

Figure 2 Bringing it all together – ALM

Sample content

If you would like to try out the content for a dry run, see ALM Training for Board Members. Buy the self paced PDF study guide for practitioners or the ALM video training course.