I have long felt a need for a high level overview course on ALM training for board members, executive committee and ALCO teams. A course that focuses in equal measure on high level concepts behind Asset Liability Management and basic calculations. Enough to give you a flavor of the subject, but stopping just before the numbers overwhelm you.

It doesn’t matter if you teach Board members or executive MBA students. Teaching applied ALM is difficult. The basic ALM concepts start easy but complexity ramps up before you can say NII or Earnings at Risk.

Therefore our current tutorial starts with the basics, adds on some context and keeps calculations to the minimum. While we have now been teaching this topic for 12 years, we still remember the dread we felt when we sat down to comprehend the difference between Maturity, Rate and Reset gap. It took a while.

The seven posts that follow should give you a full flavor of the topic. They were put together especially as pre-readings for our ALM training for board & ALCO members workshop. If you need more punishment there is more where that came from. Drop us a note and we will be more than happy to point you in the right direction.

I apologize for breaking the tutorial down into seven components but I wanted you to get a feel for the overall theme in one go. And give you the ability to pick and chose the components most relevant to your immediate needs. Feel free to skip the topics you are familiar with. The downside are the seven clicks to completely review the course.

1. Why Asset Liability Management (ALM)?

A short and sweet post that establishes the need for ALM within a bank and the requirements from a framework used to analyze the data.

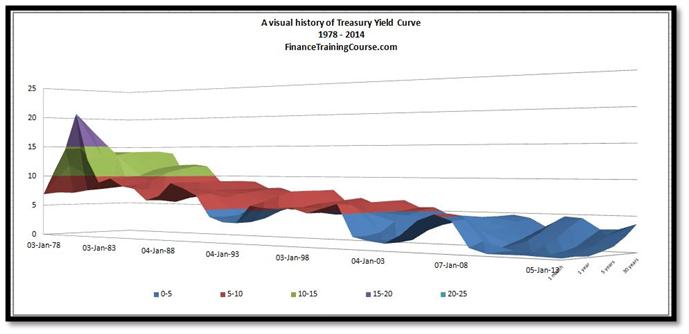

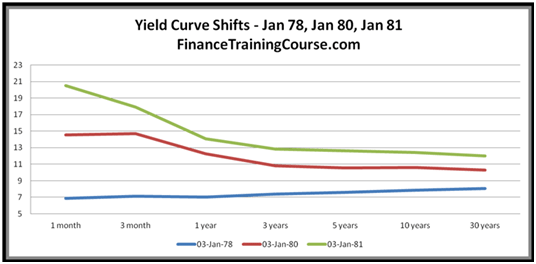

2. A visual history of yield curve shifts – 1978 – 2014

You can’t understand applications until you are comfortable with context. Our visual history walks through some of the recent interest rate shocks (recent being a relative term) recorded in the history of the US Treasury yield curve.

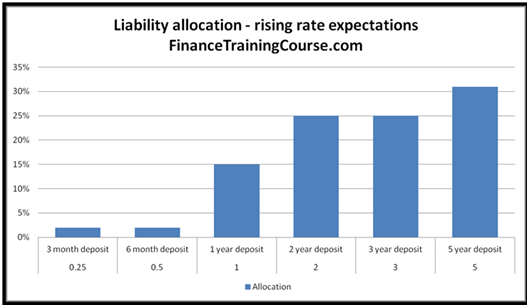

3. Default Asset Liability Management strategies for default interest rate scenarios

We introduce the concept of maturity bucketing for assets and liabilities and review default strategies for default interest rate scenarios.

Asset Liability Management Reports

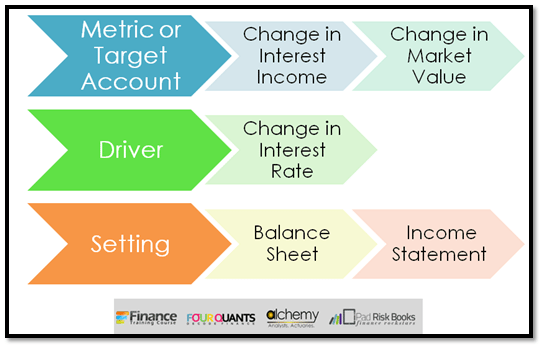

4. Asset Liability Management Strategy – The Earnings versus Value debate

Should you focus on Net Interest Income – NII (Earnings) or MVE (Value)? Can you optimize both? A brief review of the debate and the reason why boards find it easier to focus on NII discussions. We also sneak in a brief discussion on the NII template and basic calculations. Nothing too intense, just a flavor.

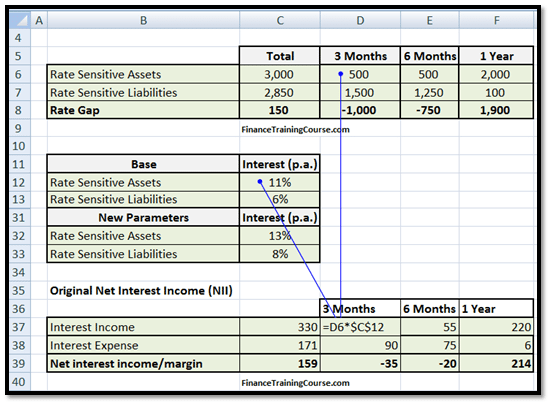

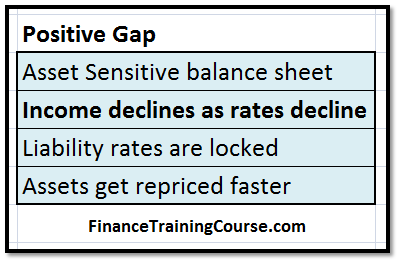

5. ALM Cheatsheet – NII, Gaps, Asset & Liability sensitivity

An opportunity to dissect the interaction between Gaps (Positive or Negative), Sensitivity (Asset or Liability) and interest rate outlook (rising or declining). How does that fit in with your assessment of your bank’s strategy?

6. Duration and Convexity calculator for US Treasuries

You can’t walk away from a course on ALM training without discussion modified duration and convexity. We try and keep it painless using the example of building a duration and convexity calculator for US treasuries.

Asset Liability Management glossary of terms for the lost and confused.

Need more great content on Asset Liability Management. Check out the Asset Liability Management Crash Course Package on our store. Combined study guide with sample Excel templates.

Comments are closed.