Iran oil economy. Nowroz comes to Tehran.

Nowroz, the Persian New Year arrives 21st March. As Tehran shrugs off a mild winter there is optimism about coming months. Iran’s journey on the road of isolation ended in December 2015. The flurry of activity it triggered is as breath taking as spring in Tehran.

Iran Oil Economy. A review of days past.

Construction was the first economic sector to take off with the election of Hassan Rouhani, the new Iranian president, in 2013. While infrastructure projects in Iran have dominated construction sector, real estate investments are essentially speculative trades used to hedge the bite of inflation. On the road to Dizin, the ski resort with twenty dollar day passes, you see a new generation of summer homes being put up on the mountain side. A short visit to any major city exposes you to a smattering of new construction sites everywhere. Tehran itself is witness to a blend of brand new single plot apartment complexes at alternate corners and large block sized multi storied mixed use commercial projects.

While property prices in Tehran shot up for three years post the election of President Rouhani, there was significant softening in that market in 2014-2015. With the removal of sanctions and with Iranian banks reconnecting with the SWIFT network, prices are set to rise again. Much before oil prices tanked globally and it became apparent that Iran was heading back into the international fold, you could feel the liquidity drain away in Dubai as Iranian cash, stored overseas for years, headed back home.

Iran’s other very visible sector enjoying signs of renewal and growth is tourism and hospitality. Ignored on account of the absence of leading regional hospitality chains, its quickly picking up pace. You can now see it at work in near completed hotel sites in prime locations in Tehran. You observe it in jazzy and ritzy fusion cuisine and sheesa bars mushrooming around inner cities and suburbs. And the grand new airport terminal being built next to the current one with a metro service that will run into the heart of the city.

For decades Iran has been a religious tourism destination for one half of the Muslim world. The new bet is on business travelers. One measure of the magnitude of deal making and the queue of projects being negotiated is the availability of Persian Azadi and Espinas – two of the leading 5 star properties in town. While alcohol and clubbing remains banned Iran is an international destination sitting at the junction of the modern world and a rich tapestry of historical and cultural heritage. It is home to Ferdowsi, Omer Khayyam, Saadi (Sherazi), Shams Tabrez and Hafez, poets that have defined literature in the region for a thousand years. If nothing else you see shades of that tradition seep in the creative canvass utilized by Iranian films, animation and artists.

Banking and financial services stand just as tall as tourism and hospitality. The expectation is that the coming wave of liquidity will raise many hulls. One of them will be banking. Capital, technology, market access, new products but most importantly growth and improved profitability that will help with recovery of infected loans and investments gone south. In anticipation of that recovery, modernization is on the cards. A decade of isolation has left Iran’s 28 banks hungry for all that is new. They have survived given the hand they were dealt, some doing far better than others.

To compete effectively they now need to step up their game. At risk is not just market share but the recovery and growth of the Iranian economy. Unless Iranian banks and insurance companies succeed in fast tracking integration with the international banking system, Iranian players, importers as well as exporters, will not be able to fully benefit from sanctions relief. The integration is linked to modernization of Iranian banking regulation (a big task) and the ability of Iranian banks to building and renewing correspondent banking relationships. Small missteps will lead to bigger challenges and problems on the trade balance front as export cargoes are delayed for lack of correct documentation and insurance cover.

Today banking is serviced by a booming technology sector, local payment systems including a debit card standard, ATM networks and switches. But there is always room for growth and progress. The banking sector is blessed with an ample supply of local PhDs in Finance, Economics, Statistics and Risk but the real charge is led by expatriate professionals who headed home with the initial thaw marked by the rise of moderates to power. Armed with North American and European experiences all they need is a change in the operating environment outside Iran. With sanctions relief and opening up of previously shuttered exports markets the much awaited improvement is finally here.

In one way sanctions and the recent price decline have been a blessing in disguise for Iran. Despite the pain and the challenges, the sanctions finally pushed Iran to let go of its dependence on oil. And that change is paying off as oil prices flirt with rock bottom levels. For Iran, oil now represents marginal revenue. It is a large part of the domestic economy, but not the only part. It helps, it opens doors to incoming streams of hard currency but its absence over four years has made Iran stronger. Perhaps not completely immune to price swings but certainly a stronger tolerance because unlike other oil producers where petrochemical dollars represent life blood, for Iran, oil is now truly a commodity.

Iran oil economy – Iran impact on oil prices?

The February Reuter Thompson Research special report on Iran post sanctions makes for an interesting read on the current state and the future of the petrochemical industry in Iran.

Iran’s crude oil production in 2012 stood at 4.1 million barrels per day. Pre revolution production peak in 1976 was 6.6 million barrels per day. Post lifting of sanctions January 2016 production estimates range between 2.9 – 3.1 million barrels per day. Production fell because of loss of skilled workers and management post revolution, limited international investment and restriction on importing new technology and skill sets into the Petrochemical sector in Iran. With foreign investments and modernization it is estimated that Iranian oil fields may produce between 5 – 7 million barrels of crude per day becoming the second largest middle eastern producer behind Saudi Arabia and ahead of Iraq. Without such investments, Iranian estimates indicate the ability to add between 800 thousand to a million barrels per day of production over the next six months.

Between August 2015 and January 2016 Iran exported an average of 1 million barrels per day of crude oil. Post sanction export estimates range between 1.5 million bpd of crude oil (within 3 months) to 2 million bpd of crude oil (through 2017). However this growth in production is limited by available storage capacity, the state of Iranian shipping vessels and trading conditions and restrictions. While fleet modernization is on the cards, the turnaround time for that effort is two to three years. Primary buyers of Iranian crude and condensates include China, Japan, India, South Korea followed by European customers lead by France, Spain, Italy and Greece[1]. Higher energy consumption in these markets will easily drink up any additional capacity Iran can serve via increased production.

Iranian budgetary figures last year (March 2015) indicated US$ 55 billion of earnings from crude oil exports. At current price levels crude oil production required to match the same revenue figures is not possible. Factor in competitive discounting on exports offered by Saudi Arabia, Iraq and Russia, and the Iranian Heavy crude would sell at an additional discount to other competitive blends, further impacting export revenues.

Even with the 30 million barrels available for sale through floating off shore storage (read: ships), Iranian crude oil sales will still miss the year ended March 2015 exports figure in March 2016 and March 2017 unless a sharp rebound in price occurs. The floating storage at current discounted prices is worth 900 million USD.

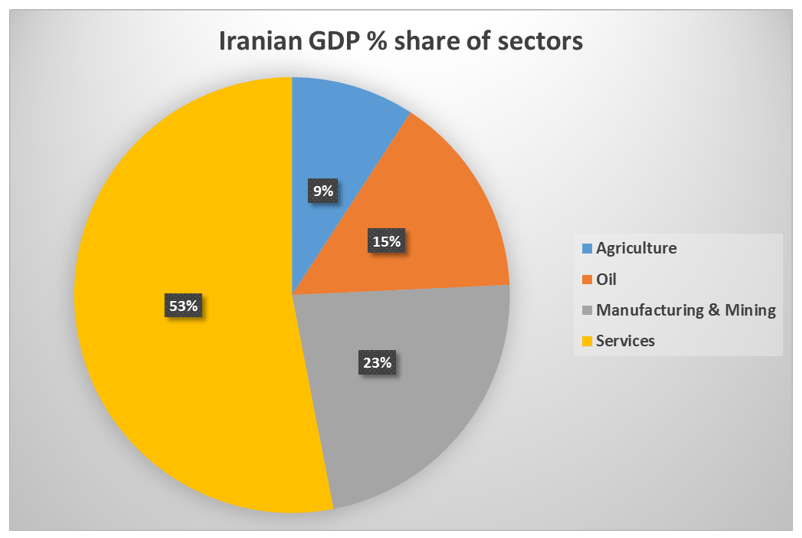

While Iranian GDP is no longer completely reliant on oil, oil exports still represent a critical part of the economy and balance of trade. The sharp reduction in prices witnessed in 2015 has created additional pressures on the economy. Despite renewed access to US$ 49 billion in previously locked away funds, Iranian requirements for hard currency are quite substantial. Part of this shortfall would get addressed by new investment in petrochemical, manufacturing, banking and other services sectors.

What does all of this mean for crude oil prices?

Iran can and will add a million barrel of production capacity and serve it to buyers of the Iranian Heavy blend in 2016. The question is will they be able to add more? And how quickly? Opinion is divided on this front. The challenge is speed and the removal of frictions that still remain on the trading front for Iranian partners. Iran certainly has the reserves and the will to make it work but will be limited by its ability to get crude cargoes into destination ports. Irritants like insurance, acceptable trading instruments, banking relationships are likely to get in the way of expanding the customer network. When oil inventory is tight, one is willing to jump through hoops to buy oil. When the market is flooded with discounted products, a buyer is likely to opt for the easiest path.

Still a anticipatory price war is being waged on account of this increase in capacity with Saudi Arabia, Iraq and Russia. With an additional one million barrel of planned production increase by Iraq in 2016-2017, crude will remain under pressure for the next 12 months as the four major players battle it out for market share. Despite short term swings in prices, given these pressures, oil is likely to stay down on the floor.

[1] Source EIA. https://www.eia.gov/beta/international/analysis.cfm?iso=IRN

The two most useful sources in the compilation of this analysis were the quarterly economic review prepared and issued by Middle East Bank and Thompson Reuters Research’s special report on Iran.

See the complete series on dissecting crude oil at The knives are out in the oil market.