Market Analysis

Crude Oil

- Crude oil remained weak during the week with WTI closed at $44.74/BBL and Brent closed at $47.37/BBL on Friday.

- OPEC monthly out report depicted increase of 0.33 million barrel a day primarily from Nigeria and Libya, which are not part of production cut deal.

- Libyan National Oil Corporation claimed to reach 900,000 bpd within June 2017 and 1 million barrels by end July.

- EIA Weekly report recorded an inventory draw of 1.66 million barrels with stock at 511.5 million barrel on 6th June 2017 with the market expecting a draw of 2.5 million barrels.

- EIA Gasoline data also put pressure on crude prices, as there is a build up of 2.10 million barrels with stock standing at 242.4 million barrels, depicting higher utilization rates at refinery along with weaker demand.

- Consistent increase of US production increase with oil rigs number at 747, an increase of 6 and gas rigs increase by 1 negated by a decrease by 1 on miscellaneous rigs by one, and total rig count stands at 933.

Natural Gas

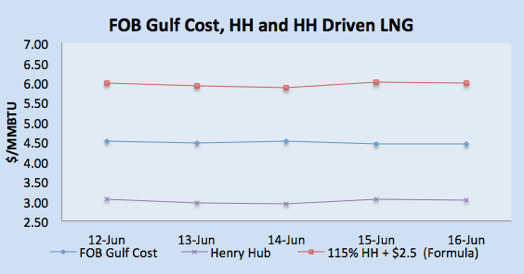

- Henry Hub prices closed on $3.03/MMBTU on Friday.

- US Henry Hub prices jumped by 4.2% at $3.05/MMBTU on Thursday after EIA showed a smaller-than-expected inventory increase.

- S. natural gas stocks increased by 78 billion cubic feet for the week ending June 9.

- Henry Hub prices remained weak at the start of the week due to cooler than normal temperature forecast to cover most of the United States.

- Demand for next week remains moderate as higher temperature in eastern half along with cooler temperature forecast across northern and east central regions.

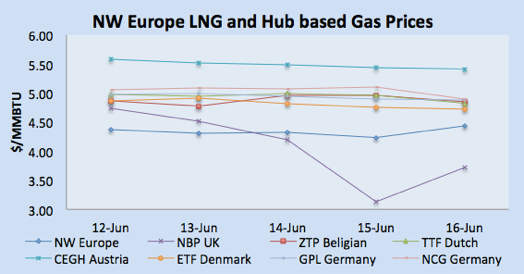

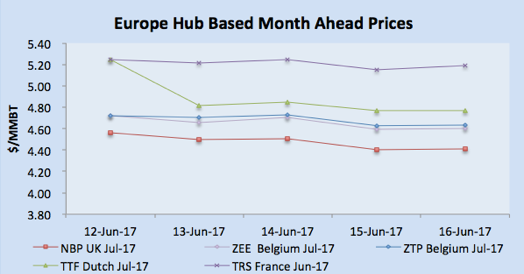

- NBP fallen due to weak demand across the UK as the weather is increasingly warm and expected to remain warm.

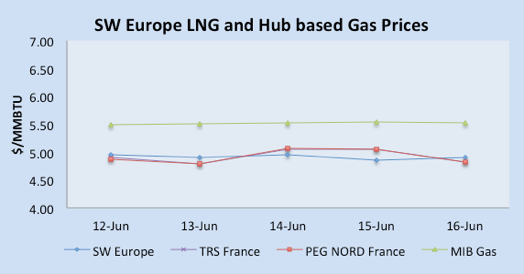

- Dutch and French gas prices remained weak due to weaker demand, TTF and TRS France closed at the equivalent of $4.82/MMBTU on Friday.

- Imports from Norway to the continent have been stable along with strong LNG send outs from Gate and Montoir.

Currency

- The US dollar remains relatively strong post the Federal Reserve rate hike last Wednesday, US DXY closed at rose to 97.14 on Friday.

- USD strength came from the Fed raising the interest rates from 1.00% to 1.25%, in a widely expected move.

- Dollar also got support from US labor data with initial jobless claims in the week ending June 10 decreased by 8,000 to 237,000 from the previous week’s total of 245,000.

- Euro/USD remain volatile during the week, with closing at 1.1146 level on Friday.

- GBP/USD remained volatile during the week and closed at above 1.2750 level, as after the Bank of England left its monetary policy unchanged, in line with expectations, but members of the Monetary Policy Committee surprised markets with three dissents.

Weather

- European weather remained in spring and will follow the same pattern across Europe for next week with Spain, Portugal, and France in the summer season.

- Cooler temperature in Argentina and Brazil, with temperature range for Argentina, is 15-20oC and Brazil around 25oC-30oC for next week.

- Mexico will be around 23 -27oC and expected to remain same for next week.

- Middle East summer season in full swing with Egypt 35oC plus, Kuwait is 45oC plus, and Dubai temperature is going to be around low 40o

- Indian Subcontinent in hot summer season: with temperature ranging between 35oC -40oC in Pakistan and India for next week.

- Summer season in North East Asia, with the temperature around 27 -30oC in Taiwan, 25-28oC in Korea, China 27 -35oC, and Japan is around 25oC for next week.

- South East Asia already in hot weather with temperature in low 30o

- USA Weather: Overall weather remained cooler than seasonal limits with east cost is getting warm.

LNG

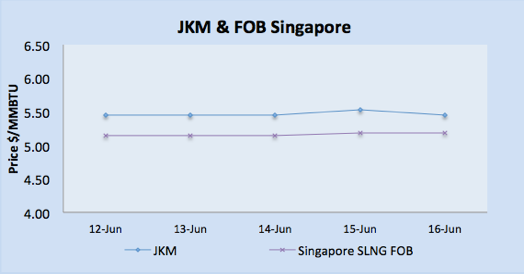

- Weaker demand kept the prices down in the Asian market with JKM at $5.40/MMBTU, FOB Singapore $5.19/MMBTU, SLNG DKI Index at $5.32/MMBTU.

- European gas hub prices remained weak with TTF at $4.82/MMBTU, PEG & TRS both at the equivalent of $4.82/MMBTU and Spanish market in high $5.50/MMBTU level.

- East of Atlantic market based upon Nigerian and Norwegian supply region is ranging between $5.20 -$5.30 net back based upon Spanish hub prices.

- North Eastern buyers from Taiwan and Japan remained on the sideline with Komipo Power securing one July delivery cargo at $5.60/MMBTU as per market news.

- Some demand emerging from India as GSPC had re-issued a tender, which they canceled earlier.

- As per market news, Jordan’s NEPCO paid in the mid $5 per MMBTU for an August cargo.

- Qatargas signed an agreement with Shell for the delivery of up to 1.1 million tons of liquefied natural gas (LNG) per year for five years.

- Smaller vessels still using Suez Canal, however one vessel Al Mafyr on its way to South Hook via Africa.

- Taiwan have received it first ever cargo from Sabine Pass via Cadiz Knutsen

- carrying 2.79 BCF of LNG, which makes it the 23rd country to receive US cargo.

- Qatar is back on managing its business with shipping line operating from Oman instead of UAE and food supply options are numerous like Brazil, Far East, however, any interference on LNG export poses a major threat of escalating the crises.

- Recent Qatar crisis has given strength to Japanese buyers in term of reviewing long term LNG supply contracts and will attempt seek more flexible terms.

- Donggi-Senoro LNG plant in Indonesia has dispatched 18 cargoes of the chilled fuel by June 2 this year.

- LNG exports from the three liquefaction plants located on Curtis Island offshore Gladstone reached 1.68 million mt during May, a rise of almost 13 percent as compared to May last year.

- Climate control results are coming with 13 Japanese trading houses are moving away from thermal coal which will support LNG and Petcoke demand.

- ENI has signed up $8bn agreement to develop gas field off the coast of Mozambique with formally approving a FLNG terminal.

- Greece, Israel, and Cyprus plan to focus on developing gas pipeline and utilization of Egypt’s LNG assets for European and Turkish. The planned project will be utilizing the gas field of Cyprus and Israel and 2025 is the target completion date.

- Bangladesh Petrobangla signs an MOU with AOT energy to supply 1.75 MTPA of LNG by mid of 2018.

- Pakistan has shelved $2 billion IP gas line project and now focusing more on setting up the infrastructure for imported LNG. There is a project under development for setting up Karachi-Lahore pipeline in which Qatar has shown interest to develop the project.

- Australian Energy Market Operator has revised its outlook on gas shortage, however still emphasizing on a remedial action in case of an extreme condition like summer season.

|

|

|

|

|

|

LNG Merchant Activity

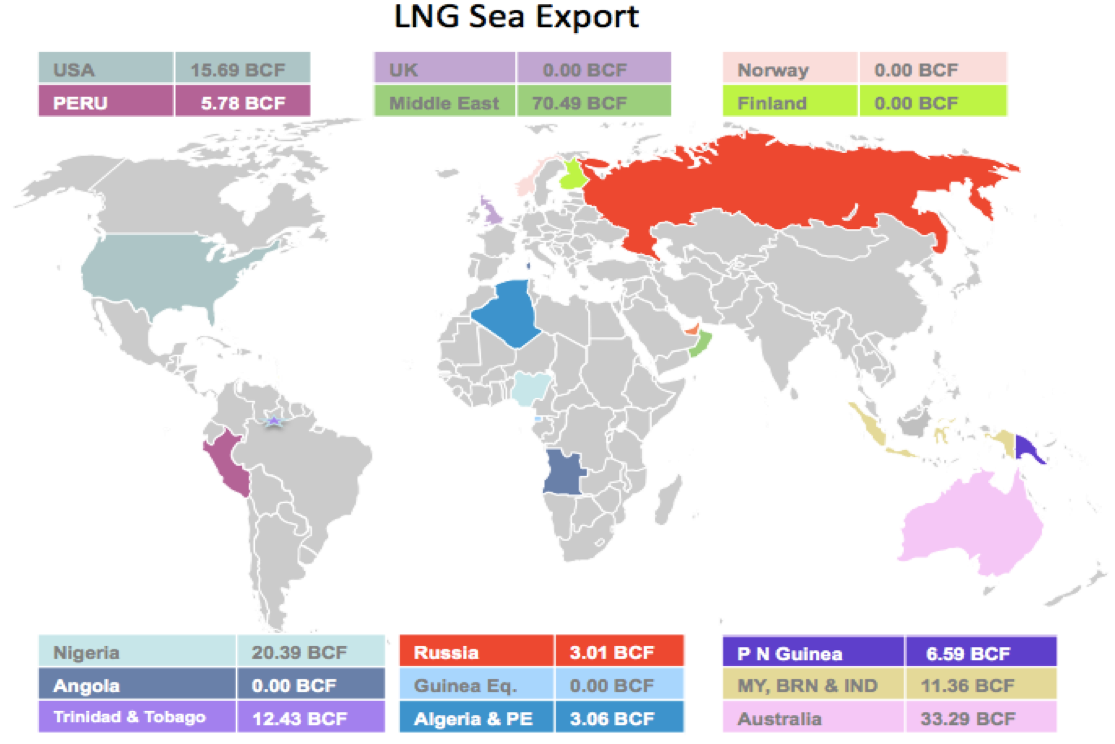

- This week 57 vessels carrying 3.57 million tons (182.09 BCF) loaded from various supply centers, decrease by 0.58 million tons from last week.

- Six vessels carrying 20.39 BCF departed from Nigerian port for European and Asian locations, one destined for Egypt.

- Algeria loaded two vessels carrying 3.06 BCF for Spain.

- Pont Fortin, Trinidad & Tobago loaded four vessels with 12.4 BCF.

- Four vessels loaded this week from Sabine Pass, USA with 115.69 BCF destined for South America and European ports.

- Two vessels loaded from Brunei with a load of 4.34 BCF.

- One vessel departed from Russia carrying 3.01 BCF for China.

- 10 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China, and Singapore carrying 33.29 BCF.

- Middle Eastern terminals at Das Island (UAE), Qalhat (Oman) and Ras Lafan (Qatar) loaded 21 vessels carrying 61.87 BCF for Asian destinations. Three vessels destined for Indian & Pakistani ports carrying 8.95 BCF.

| Departure Date | Vessel Name | Capacity (CBM) | Loading Port | Discharge Port | ETA Discharge Port | LNG (BCF) |

| 11-Jun-17 | BRITISH RUBY | 155,000 | Bonny, Nigeria | Dafeng, China | 15-Jul-17 | 3.20 |

| 13-Jun-17 | COOL RUNNER | 160,000 | Bonny, Nigeria | Atlantic Ocean | 21-Jun-17 | 3.30 |

| 13-Jun-17 | GASLOG GREECE | 174,000 | Bonny, Nigeria | Not Known | 08-Jul-17 | 3.59 |

| 13-Jun-17 | COOL RUNNER | 160,000 | Bonny, Nigeria | Atlantic Ocean | 21-Jun-17 | 3.30 |

| 15-Jun-17 | LNG BONNY II | 177,000 | Bonny, Nigeria | Asia | 18-Jun-17 | 3.65 |

| 16-Jun-17 | BW GDF SUEZ PARIS | 162,524 | Bonny, Nigeria | Sokhna, Egypt | 06-Jul-17 | 3.35 |

| 11-Jun-17 | CHEIKH EL MOKRANI | 73,990 | Skikda, Algeria | Barcelona, Spain | 13-Jun-17 | 1.53 |

| 16-Jun-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | Fos Sur Mer, France | 18-Jun-17 | 1.53 |

| 11-Jun-17 | BILBAO KNUTSEN | 135,049 | Pampa Melchorita, Peru | Atlantic Basin | 25-Jun-17 | 2.79 |

| 15-Jun-17 | METHANE NILE EAGLE | 145,000 | Pampa Melchorita, Peru | London, UK | 21-Jun-17 | 2.99 |

| 12-Jun-17 | BW GDF SUEZ EVERETT | 138,028 | Point Fortin, Trinidad | North Atlantic | 2.85 | |

| 11-Jun-17 | MARAN GAS AGAMEMNON | 174,000 | Point Fortin, Trinidad | Pacific Ocean | 28-Jun-17 | 3.59 |

| 14-Jun-17 | GASLOG SEATTLE | 154,948 | Point Fortin, Trinidad | Mediterrian | 30-Jun-17 | 3.20 |

| 16-Jun-17 | CASTILLO DE VILLALBA | 135,420 | Point Fortin, Trinidad | 2.79 | ||

| 12-Jun-17 | CREOLE SPIRIT | 173,400 | Sabine Pass, USA | 3.58 | ||

| 11-Jun-17 | TORBEN SPIRIT | 235,000 | Sabine Pass, USA | Atlantic Basin | 15-Jun-17 | 4.85 |

| 15-Jun-17 | HYUNDAI PRINCEPIA | 178,602 | Sabine Pass, USA | Cristobal, Panama | 20-Jun-17 | 3.68 |

| 14-Jun-17 | CASTILLO DE SANTISTEBAN | 173,673 | Sabine Pass, USA | Cristobal, Panama | 18-Jun-17 | 3.58 |

| 16-Jun-17 | SURYA AKI | 50,600 | Bintulu, Malaysia | Hiroshima,Japan | 22-Jun-17 | 1.04 |

| 11-Jun-17 | GOLAR MAZO | 135,000 | Bontang, Indonesia | Not Known | 20-Jun-17 | 2.79 |

| 16-Jun-17 | GASLOG SINGAPORE | 154,948 | Bontang, Indonesia | Pacific Basin | 3.20 | |

| 13-Jun-17 | GIGIRA LAITEBO | 173,870 | Lese, Papua New Guinea | Yeosu, Korea | 22-Jun-17 | 3.59 |

| 15-Jun-17 | PACIFIC ARCADIA | 145,400 | Lese, Papua New Guinea | Chiba, Japan | 29-Jun-17 | 3.00 |

| 15-Jun-17 | GRAND MEREYA | 145,964 | Prigorodnoye, Russia | Jiangyn, China | 21-Jun-17 | 3.01 |

| 12-Jun-17 | ABADI | 135,269 | Sieria Oil Terminal, Brunei | Oita, Japan | 19-Jun-17 | 2.79 |

| 13-Jun-17 | BELANAK | 75,000 | Sieria Oil Terminal, Brunei | 1.55 | ||

| 13-Jun-17 | NORTHWEST SANDERLING | 125,452 | Dampier, Australia | Pacific Ocean | 28-Jun-17 | 2.59 |

| 11-Jun-17 | LNG EBISU | 147,546 | Dampier, Australia | Himeji, Japan | 24-Jun-17 | 3.04 |

| 13-Jun-17 | LNG KOLT | 210,000 | Dampier, Australia | Pyeongtaek, Korea | 24-Jun-17 | 4.33 |

| 15-Jun-17 | WOODSIDE ROGERS | 159,800 | Dampier, Australia | Pacific Basin | 27-Jun-17 | 3.30 |

| 16-Jun-17 | PACIFIC ENLIGHTEN | 147,800 | Dampier, Australia | Oita, Japan | 26-Jun-17 | 3.05 |

| 16-Jun-17 | WOODSIDE CHANEY | 174,000 | Dampier, Australia | Pacific Basin | 03-Jul-17 | 3.59 |

| 14-Jun-17 | ALTO ACRUX | 147,978 | Darwin, Australia | Kisarazu, Japan | 19-Jun-17 | 3.05 |

| 13-Jun-17 | MARAN GAS ACHILLES | 174,000 | Gladstone, Australia | Not Known | 24-Jun-17 | 3.59 |

| 12-Jun-17 | LNG SATURN | 153,000 | Gladstone, Australia | Qindago, China | 22-Jun-17 | 3.16 |

| 15-Jun-17 | CESI GLADSTONE | 174,000 | Gladstone, Australia | Beihei, China | 26-Jun-17 | 3.59 |

| 13-Jun-17 | MUBARAZ | 135,000 | Das, UAE | Kawasaki, Japan | 01-Jul-17 | 2.79 |

| 16-Jun-17 | GHASHA | 137,100 | Das, UAE | Tokyo, Japan | 04-Jul-17 | 2.83 |

| 16-Jun-17 | IBRA LNG | 145,951 | Qalhat, Oman | Abu Dhabi, UAE | 17-Jul-17 | 3.01 |

| 11-Jun-17 | AL AAMRIYA | 206,958 | Ras Laffan, Qatar | Barcelona, Spain | 16-Jul-17 | 4.27 |

| 11-Jun-17 | ASEEM | 154,948 | Ras Laffan, Qatar | Dahej, India | 14-Jun-17 | 3.20 |

| 13-Jun-17 | DISHA | 136,026 | Ras Laffan, Qatar | Dahej, India | 21-Jun-17 | 2.81 |

| 12-Jun-17 | MILAHA RAS LAFFAN | 136,199 | Ras Laffan, Qatar | Far East | 26-Jun-17 | 2.81 |

| 16-Jun-17 | DUHAIL | 210,100 | Ras Laffan, Qatar | Incheon, Korea | 01-Jul-17 | 4.33 |

| 16-Jun-17 | MARAN GAS ASCLEPIUS | 142,906 | Ras Laffan, Qatar | Indian Ocean | 20-Jun-17 | 2.95 |

| 13-Jun-17 | AL SHAMAL | 213,536 | Ras Laffan, Qatar | MinaAhmadi, Kuwait | 17-Jun-17 | 4.41 |

| 12-Jun-17 | AL NUAMAN | 205,981 | Ras Laffan, Qatar | Not Known | 4.25 | |

| 12-Jun-17 | UMM BAB | 143,708 | Ras Laffan, Qatar | Not Known | 21-Jun-17 | 2.96 |

| 16-Jun-17 | HL RAS LAFFAN | 185,000 | Ras Laffan, Qatar | Pyeongtaek, Korea | 01-Jul-17 | 3.82 |

| 12-Jun-17 | ZEKREET | 178,200 | Ras Laffan, Qatar | Singapore | 21-Jun-17 | 3.68 |

| 11-Jun-17 | DOHA | 135,200 | Ras Laffan, Qatar | Singapore | 20-Jun-17 | 2.79 |

| 15-Jun-17 | AL ZUBARAH | 135,510 | Ras Laffan, Qatar | Singapore | 26-Jun-17 | 2.80 |

| 11-Jun-17 | WILPRIDE | 156,007 | Ras Laffan, Qatar | Suez Canal | 18-Jun-17 | 3.22 |

| 15-Jun-17 | MURWAB | 205,971 | Ras Laffan, Qatar | Suez Canal | 28-Jun-17 | 4.25 |

| 15-Jun-17 | AL DAAYEN | 148,853 | Ras Laffan, Qatar | Suez Canal, Egypt | 25-Jun-17 | 3.07 |

| 16-Jun-17 | TAITAR NO.1 | 154,948 | Ras Laffan, Qatar | Taichung, Taiwan | 30-Jun-17 | 3.20 |

| 14-Jun-17 | AL AREESH | 148,786 | Ras Laffan, Qatar | 22-Jun-17 | 3.07 |