Market Analysis

Crude Oil

- Crude oil price close on Friday at $49.95/BBL and decrease by 4.48%.

- Crude started strong on gasoline stocks and memorial day long weekend and supported further during the week on bullish data of EIA inventories which as strong drawdown of 6.43 million barrel in Crude inventories & 1.7 million barrel on gasoline inventory.

- However, Wednesday Crude Oil price sank 3% to settle at $50.31/BBL primarily due to increase in Libyan and Nigerian output, as both countries are exempt from production cut. Libyan’s oil production reached to 827,000 BPD now.

- Further blow to crude prices came from US pulling out from Paris Climate accord and strong oil production from US. As per BHI, the oil rig count rose 733, 11 this week and natural gas increased by 8, which total counts of 916.

Natural Gas

- Natural Gas in US kept moving north and closed at $3.00/MMBTU, a decrease of 4.76%.

- The downward movement is initially due to cooler than expected weather forecast across United States.

- The bearish sentiments got support from weekly EIA natural gas inventories data, which depicted an increase in working gas by 81 BCF from the previous week, highest weekly build up since June 2016.

- Record amount of natural gas approximately 8.0 BCF from Marcellus and Utica shale is available to US market and further dampening the price sentiments.

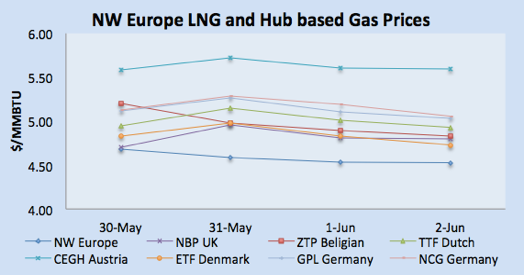

- NBP UK moved downward and closed at the equivalent of $4.79/MMBTU due to weaker demand as temperature forecast is warmer than seasonal normal plus resumption of Norwegian gas supply.

- Dutch and French prices also moved downward on the same premise of weather forecast along with falling oil prices and healthy supplies from Norwegian and Russian pipeline gas supplies. TTF closed at the equivalent of $4.93/MMBTU and TRS France at $5.20/MMBTU on Friday.

Currency

- Dollar remained stable to weak during the week and closed on seven month low primarily on data depicting slow US job growth.

- US economy added 138,000 jobs far lower than the expected number of 185,000 jobd with unemployment rate fell to 4.3%, lowest in 16 years.

- UD DXY was at 96.67 down by 0.55% on Friday.

- Euro rose to 1.1280, up by 0.30% by Friday evening the increase is primarily bad performance of US $.

- GBP closed at 1.2887, up by 0.03%, as polls indicated that Conservative Party hold a marginal lead over Labour party ahead of election on June 8.

Weather

- European weather is remained warmer than seasonal normal and expected to follow the same pattern across Europe for next week.

- Cooler temperature in Argentina and Brazil, with temperature range for Argentina is 15oC and Brazil around 30oC .

- Mexico will be around 23 oC-27oC by Friday and expected to remain in the same range during next week.

- Middle east is now in summer season with Egypt 35oC plus degrees, Kuwait City is between 40oC -45oC, and Dubai temperature around 38oC -41oC .

- Indian Subcontinent: Pakistan & India around 35oC – 45oC, and will be in the same range next week.

- Summer season in North East Asia, with temperature around 27oC -32oC in Taiwan, 28oC in Korea, China 25 oC-35oC, and Japan is around 29oC.

- South East Asia already in hot weather with temperature in low 30oC.

- USA Weather: Overall cold weather with temperature ranging between 25oC-30oC.

LNG

- Overall LNG market is weak on over supply and subdued demand.

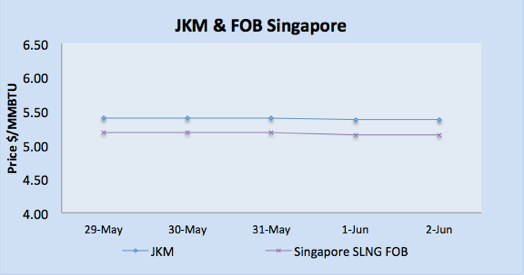

- Asian LNG price kept lower this week on supply glut specially Gorgon LNG train 1 back online. JKM closed at $5.40/MMBTU.

- Japanese inventories are full due to mild winter and cargoes are secured to June & July.

- Overall demand is mostly covered and demand is expected from European region, where prices are high.

- RWE received it first cargo from Qatar under the long term supply agreement of 1.1 MTPA via Q Flex Al Kharana at GATE Terminal Rotterdam, where RWE has long term contract.

- Tender for one cargo for mid June loading is issue from Gorgon, whereas supply tenders are still not closed from Angola and Nigeria.

- European markets specially Spanish market is still offering better netback in comparison with Asian spot markets.

- European gas hub prices remained stable with NBP UK closed on $4.79/MMBTU, TTF at $4.93/MMBTU after reaching the peak of $5.14/MMBTU and pries remained in high $5.00 level in Spanish market.

- France and Spain are still better market for US cargoes in term of netbacks in comparison with Asian and NW Europeans markets.

- At current LNG price level, Nigerian and Angola producers will get better netback than US producer due to freight economics.

- Spring weather with the expectation of few degrees lower in the coming week will put pressure on European gas prices.

- Future prices at different European hub remain stable with no interest beyond July contracts, Q3 and winter contracts are getting interest in NBP and TTF.

- Though not openly but North Easter Asian customers are reviewing long term LNG contract conditions specially from Middle East, this certainly means LNG is maturing into a commodity with much more liquidity.

- Polish Minister believe that US LNG can reduce dominance on GAZPROM dominance as Poland is ready to receive it first LNG cargo from Cheniere by mid June 2017.

- MOU has been signed between Indian Gujrat Gas Company and Petronet for gas marketing and LCNG, which means LNG in road tankers to CNG stations.

- Eni will be developing a floating LNG liquefaction facility with estimated cost of USD 8 billion off the coast of Mozambique, the project will have production capacity of 3.4 MTPA and is expected to commission in 2022.

- Saudi Arabia also planning to enter into LNG business through considering Yamal LNG and Artic basin in partnership with Russia.

- Besides China, Japan is also keen in securing LNG cargoes from US through signing agreement during US Energy Secretary visit to Tokyo. Japanese companies are already keen in expanding LNG trade business specially the spot trade.

- More LNG supply from Australia as Gorgon LNG Train 1 resumed production ahead of time, the train has an outage in Mid May and expected to be online in a month time. Train 1 and 2 has combine production capacity of 10.4 MTPA.

- Poland has initiated a survey for a pipeline project, which can allow Poland to import 10 BCM of gas from Norway. Poland intend to replace all its gas procurement in 2022, once its long term gas supply deal with Gazprom expires.

|

|

|

|

|

LNG Merchant Activity

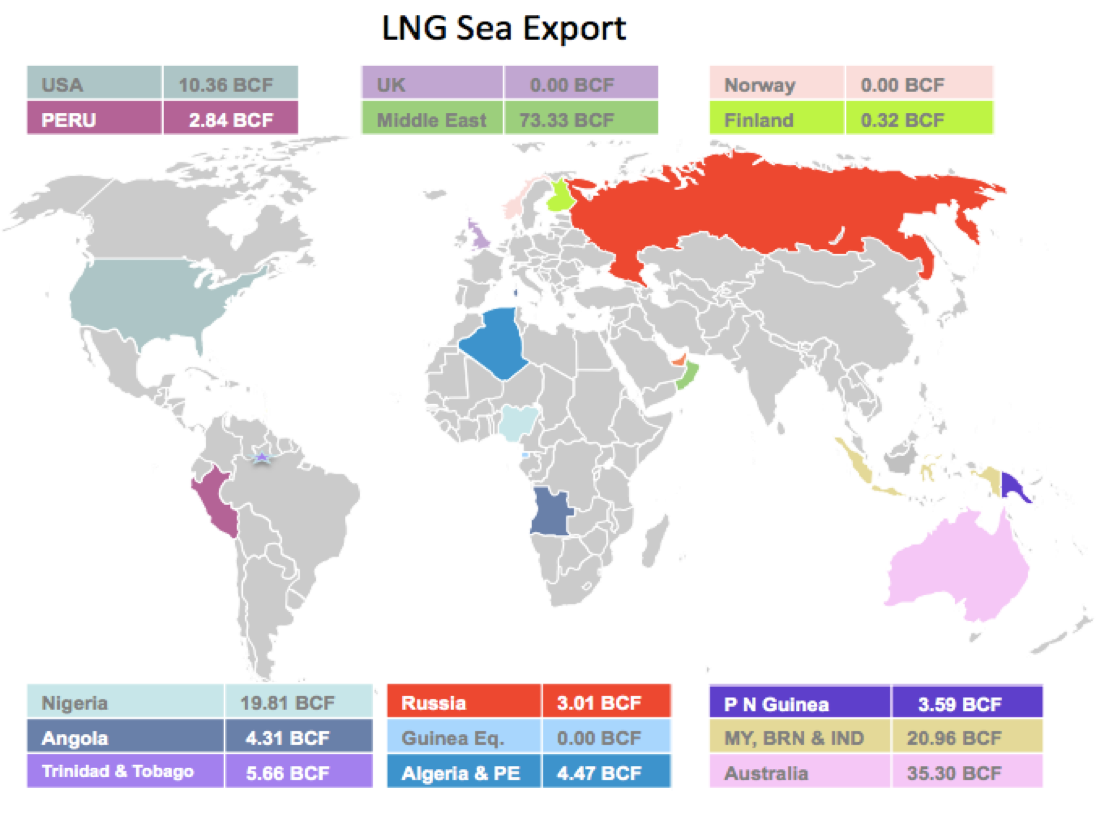

- This week 99 vessels carrying 61 million tons (183.95 BCF) loaded from various supply centres. An decrease of 0.62 million tons from last week.

- Six vessels carrying 19.81 BCF departed from Nigerian port for European locations. Four are destined for Spain & France.

- Algeria loaded one vessel carrying 1.53 BCF for Frances, whereas two vessels for European destinations, whereas one vessel loaded from Angola carrying 4.31 BCF.

- PNG loaded one vessel, Spirit of Hela, carrying 3.59 BCF for China.

- Pont Fortin, Trinidad & Tobago loaded two vessels with 5.66 BCF.

- 3 vessels loaded this week from Sabine Pass, USA with 10.36, one vessel is heading for Sines, Portugal.

- One vessel loaded from Brunei with load of 3.20 BCF.

- One vessel departed from Russia carrying 3.01 BCF.

- 11 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Singapore carrying 35.30 BCF.

- Middle Eastern terminals at Das Island (UAE) and Ras Lafan (Qatar) loaded 22 vessels carrying 67.76 BCF for Asian destinations. Three vessels destined for Indian ports carrying 10.42 BCF.

| Departure Date | Vessel Name | Capacity (CBM) | Loading Port | Discharge Port | ETA Discharge Port | LNG (BCF) |

| 2-Jun-17 | BRITISH SAPPHIRE | 155,000 | Bonny, Nigeria | Europe | 12-Jun-17 | 3.20 |

| 30-May-17 | CORCOVADO LNG | 159,800 | Bonny, Nigeria | Not Known | 17-Jun-17 | 3.30 |

| 31-May-17 | LNG BORNO | 149,600 | Bonny, Nigeria | Cartagena, Spain | 27-Jun-17 | 3.09 |

| 30-May-17 | LNG KANO | 148,565 | Bonny, Nigeria | Fos Sur Mer, France | 3.07 | |

| 28-May-17 | LNG LAGOS II | 177,000 | Bonny, Nigeria | Montoir, France | 17-Jun-17 | 3.65 |

| 27-May-17 | LNG PORT HARCOURT II | 170,000 | Bonny, Nigeria | Kuwait City, Kuwait | 18-Jun-17 | 3.51 |

| 31-May-17 | SPIRIT OF HELA | 173,800 | Lese, Papua New Guinea | Qindago, China | 11-Jun-17 | 3.59 |

| 2-Jun-17 | METHANE HEATHER SALLY | 142,702 | Punta Europa | Not Known | 2.94 | |

| 30-May-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | Fos Sur Mer, France | 31-May-17 | 1.53 |

| 30-May-17 | MARAN GAS PERICLES | 209,000 | Soyo, Angola | Not Known | 4.31 | |

| 30-May-17 | HISPANIA SPIRIT | 137,814 | Pampa Melchorita, Peru | Not Known | 24-Jun-17 | 2.84 |

| 27-May-17 | BRITISH INNOVATOR | 136,135 | Point Fortin, Trinidad | Atlantic Ocean | 07-Jun-17 | 2.81 |

| 2-Jun-17 | BW GDF SUEZ EVERETT | 138,028 | Point Fortin, Trinidad | Not Known | 2.85 | |

| 2-Jun-17 | GASLOG SHANGHAI | 154,948 | Sabine Pass, USA | South America | 31-May-17 | 3.20 |

| 30-May-17 | RIBERA DEL DUERO KNUTSEN | 173,400 | Sabine Pass, USA | Sines, Portugal | 13-Jun-17 | 3.58 |

| 27-May-17 | STENA CRYSTAL SKY | 173611 | Sabine Pass, USA | Not Known | 28-Jun-17 | 3.58 |

| 30-May-17 | HYUNDAI GREENPIA | 125000 | Bintulu, Malaysia | Pyeongtaek, Korea | 05-Jun-17 | 2.58 |

| 28-May-17 | BELANAK | 75,000 | Bontang, Indonesia | Oita, Japan | 06-Jun-17 | 1.55 |

| 28-May-17 | DWIPUTRA | 127,386 | Bontang, Indonesia | Oita, Japan | 08-Jun-17 | 2.63 |

| 2-Jun-17 | EKAPUTRA 1 | 136,400 | Bontang, Indonesia | Sakaisenboku, Japan | 09-Jun-17 | 2.81 |

| 30-May-17 | GOLAR MAZO | 135,000 | Bontang, Indonesia | Not Known | 03-Jun-17 | 2.79 |

| 28-May-17 | LNG AQUARIUS | 126,750 | Bontang, Indonesia | Indonesia | 09-Jun-17 | 2.61 |

| 28-May-17 | EXCEL | 135,344 | MIGAS LNG BATU, Indonesia | Chiba, Japan | 03-Jun-17 | 2.79 |

| 27-May-17 | GRAND MEREYA | 145,964 | Prigorodnoye, Russia | Yumgan, Taiwan | 02-Jun-17 | 3.01 |

| 2-Jun-17 | AMANI | 155,000 | Sseria Oil Terminal, Brunei | Indian Ocean | 3.20 | |

| 1-Jun-17 | ASIA ENDEAVOUR | 154,948 | Dampier, Australia | Not Known | 3.20 | |

| 30-May-17 | ENERGY FRONTIER | 144,596 | Dampier, Australia | Shimizu, Japan | 08-Jun-17 | 2.98 |

| 27-May-17 | STENA CLEAR SKY | 173,593 | Dampier, Australia | Himeji, Japan | 06_june-2017 | 3.58 |

| 1-Jun-17 | WOODSIDE GOODE | 159,800 | Dampier, Australia | Pacific Ocean | 01-Jun-17 | 3.30 |

| 1-Jun-17 | ENERGY ADVANCE | 144,590 | Darwin, Australia | Yokohama, Japan | 11-Jun-17 | 2.98 |

| 30-May-17 | BW PAVILION LEEARA | 161,880 | Gladstone, Australia | Qindago, China | 09-Jun-17 | 3.34 |

| 28-May-17 | MARAN GAS ROXANA | 173,400 | Gladstone, Australia | Not Known | 07-Jun-17 | 3.58 |

| 1-Jun-17 | MARAN GAS ULYSSES | 174,000 | Gladstone, Australia | Pacific Ocean | 13-Jun-17 | 3.59 |

| 1-Jun-17 | SERI BAKTI | 149,886 | Gladstone, Australia | Pacific Ocean | 11-Jun-17 | 3.09 |

| 28-May-17 | SERI BIJAKSANA | 149,822 | Gladstone, Australia | Malaca, Malaysia | 09-Jun-17 | 3.09 |

| 2-Jun-17 | YK SOVEREIGN | 124582 | Gladstone, Australia | Tongyeong, Korea | 13-Jun-17 | 2.57 |

| 27-May-17 | CORAL ENERGY | 15,500 | Pori, Finland | Rotterdam, Netherland | 30-May-17 | 0.32 |

| 31-May-17 | MRAWEH | 135,000 | Das, UAE | Not Known | 19-Jun-17 | 2.79 |

| 27-May-17 | MUBARAZ | 135,000 | Das, UAE | West Africa | Not Known | 2.79 |

| 28-May-17 | AL DEEBE | 142,795 | Ras Laffan, Qatar | Taichung, Taiwan | 12-Jun-17 | 2.95 |

| 27-May-17 | AL GHASHAMIYA | 211,855 | Ras Laffan, Qatar | Shuaiba City, Kuwait | 29-May-17 | 4.37 |

| 30-May-17 | AL JASRA | 135,855 | Ras Laffan, Qatar | Yokkachi, Japan | 19-Jun-17 | 2.80 |

| 27-May-17 | AL KHARSAAH | 211885 | Ras Laffan, Qatar | Egypt | 03-Jun-17 | 4.37 |

| 29-May-17 | AL RUWAIS | 205,994 | Ras Laffan, Qatar | Egypt | 06-Jun-17 | 4.25 |

| 2-Jun-17 | AL THAKHIRA | 143,517 | Ras Laffan, Qatar | Jeddah, KSA | 11-Jun-17 | 2.96 |

| 30-May-17 | AL UTOURIYA | 211,879 | Ras Laffan, Qatar | Cochin, India | 04-Jun-17 | 4.37 |

| 1-Jun-17 | AL WAKRAH | 134624 | Ras Laffan, Qatar | Not Known | 2.78 | |

| 2-Jun-17 | ASEEM | 154,948 | Ras Laffan, Qatar | Dahej, India | 6-Jun-17 | 3.20 |

| 1-Jun-17 | DOHA | 135,200 | Ras Laffan, Qatar | Mataphut, Thailand | 2.79 | |

| 28-May-17 | EJNAN | 143,815 | Ras Laffan, Qatar | Egypt | 04-Jun-17 | 2.97 |

| 29-May-17 | FRAIHA | 205,950 | Ras Laffan, Qatar | Not Known | 4.25 | |

| 1-Jun-17 | GOLAR CELSIUS | 160,000 | Ras Laffan, Qatar | Not Known | 10-Jun-17 | 3.30 |

| 30-May-17 | GOLAR GLACIER | 162,500 | Ras Laffan, Qatar | Not Known | 3.35 | |

| 28-May-17 | MARAN GAS ASCLEPIUS | 142,906 | Ras Laffan, Qatar | Soroosh, Iran | 31-May-17 | 2.95 |

| 30-May-17 | RAAHI | 138,077 | Ras Laffan, Qatar | Dahej, India | 02-Jun-17 | 2.85 |

| 28-May-17 | SK SUMMIT | 135,933 | Ras Laffan, Qatar | Incheon, Korea | 12-Jun-17 | 2.80 |

| 1-Jun-17 | UMM AL AMAD | 206,958 | Ras Laffan, Qatar | Not Known | 4.27 | |

| 1-Jun-17 | UMM BAB | 143,708 | Ras Laffan, Qatar | Port Qasim, Pakistan | 05-Jun-17 | 2.96 |

| 1-Jun-17 | WILFORCE | 155,900 | Ras Laffan, Qatar | Egypt | 06-Jun-17 | 3.22 |