Market Analysis

Crude Oil

- Crude oil gained strength in the first two days of the week primarily on US dollar strength and firmer than expected data from China’s PMI Index.

- However crude prices afterwards moved south based upon concerned about over supply situation, with OPEC production cut ineffectiveness depicted by 0.28 million BPD during June 2017.

- High compliance by Gulf producers Saudi Arabia and Kuwait helped keep OPEC’s adherence with its supply curbs at a historically high 92 percent in June, compared with 95% in May.

- Increased output from Libya and Nigeria is major bearish factor hovering on crude prices.

- Brent price shed 5.98% from Monday and closed at $46.71/BBL, whereas WTI closed at $44.23/BBL on Friday.

- Prices remained bearish on Friday on news from Russia, who is opposing any further production cut however there are reports that OPEC would consider putting a cap on Nigerian and Libyan output.

- Baker Hughes rig count reported an increase of 7 oils rigs, raising it to 763, whereas gas rig increase by 5, with total number of rigs at 952.

- EIA Weekly report reported a draw of 6.3 million barrels with stock at 502.9 million barrel on 30th June, with market expectations were of 2.5 million barrels draw.

- Gasoline inventories at 237.3 million barrel reported on 30th June 2017, recorded a draw of 3.7 million barrel.

- My assessment is crude oil price will remain under pressure due to over supplied condition and ineffectiveness of OPEC production cut.

Natural Gas

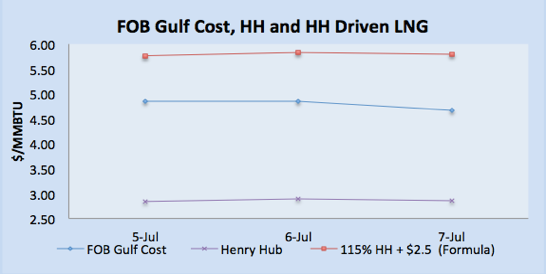

- Henry Hub prices declined 5.79% from last Friday and closed at $2.86/MMBTU on Friday.

- Weaker prices are primarily on the weather outlook, which is suggesting normal temperature and still there is not a big demand for airconditioning in the coming week.

- S. natural gas stocks increased by 72 BCF for the week ending June 30th versus market expectation of 63 BCF increase.

- Working gas in storage was 2,888 BCF as of Friday, June 30 Stocks were 285 BCF less than last year at this time and 187 BCF above the five-year average. At 2,888 BCF, total working gas is within the five-year historical range.

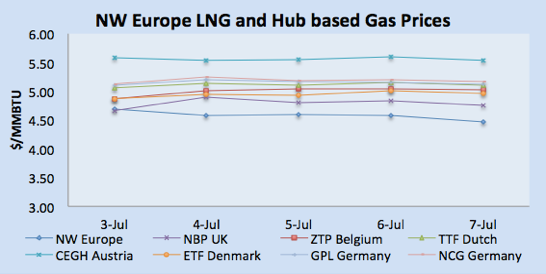

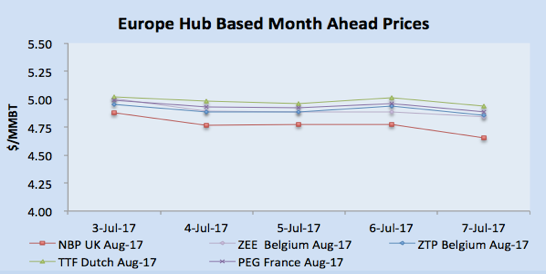

- NBP UK kept on moving south and closed at 36.96 Pence/Therm (equivalent $4.76/MMBTU) due to healthy flows in NBP system and pleasant weather in the beginning of the week along with cooler weather forecast for next week.

- Dutch and French gas prices remained stable due to warm weather and SEGAL pipeline outage still putting pressure on the system.

- However Norwegian and Russian flows are normal in the continental system keeping the prices in control.

- TTF closed at €15.26/MWH (equivalent of $5.10/MMBTU) and PEG Nord France closed at €15.00/MWH ($5.01/MMBTU) on Friday.

Currency

- Throughout the week USD remained volatile with DXY on Monday opened at 95.65 and closed at 95.80 on Friday.

- The volatility is attributed to weaker US private employers job data, which was lower than market expectations, weaker UK manufacturing activity data and strong US payroll reports from non farm sector.

- GBP/USD fell to $1.2885, down 0.66%, after a data on Friday showed manufacturing activity in May undershot expectations, declining 0.2% against economists’ forecasts of a 0.5% increase.

- EUR/USD bounced off session lows to $1.1405, down 0.16%. The single currency has remained bullish, after the minutes from European Central Bank’s previous meeting, revealed that policymakers had discussed removing the central bank’s long-standing pledge to expand or extend its bond-purchase program.

Weather

- Summer in Europe with UK and Belgium remained warm, however next week forecast is around 22 oC due to rain. Netherland weather is also expected to be around 22oC next week from 24oC this week. Spain, France and Portugal remained hot this week and expected to remain hot next week.

- Temperature in Argentina remained around 13-16oC and expected to remain same in the coming week. Brazil remained around 20-25oC and expected to be remained around 24oC next week.

- Mexico will be around 23oC in the coming week same as this week

- Middle East region summer season in full swing with Egypt around 40oC, Kuwait touched 50oC, and UAE temperature reached 45o and will remain the same next week.

- Indian Subcontinent in hot summer season: with temperature around 35-40oC in Pakistan and India around 35o Same weather profile for the next week.

- Summer season in North East Asia, with temperature around 33-35oC in Taiwan, 30-33oC in Korea, China 35oC, and Japan is around 30oC for next week.

- South East Asia already in hot weather, Thailand around 35oC, Indonesia and Malaysia ranging between 32-35oC, and will remain same next week.

- USA Weather: Overall weather is hot with 30 oC and weather forecast remain same for next week.

LNG

- Demand in Asia is still weak as inventories are high in Korea, Taiwan and Japan. Focused is shifting on September deliveries and demand for August delivery is very thin.

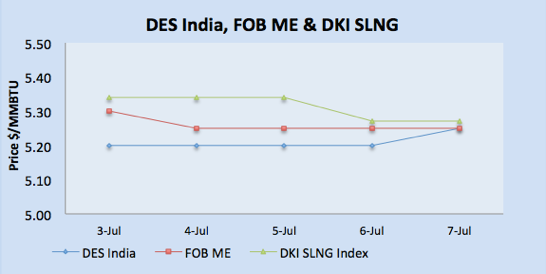

- Asian market closed on Friday with JKM at $5.40/MMBTU, FOB Singapore $5.184/MMBTU, SLNG DKI at $5.271/MMBTU. Demand focus now shifting towards winter now.

- JKM future for August is trading at $5.445/MMBTU whereas September delivery is traded $5.550/MMBTU, pushing in prices in contango.

- Indian demand also fading due to a good monsoon rainfall, which has resulted in reduced power demand along with Dabhol terminal not accessible during monsoon.

- Indian customer still on the side lines, expecting prices to further go down before they enter the market for September delivery.

- Indian prices closed on Friday within a ranges of $5.25-$5.27/MMBTU level

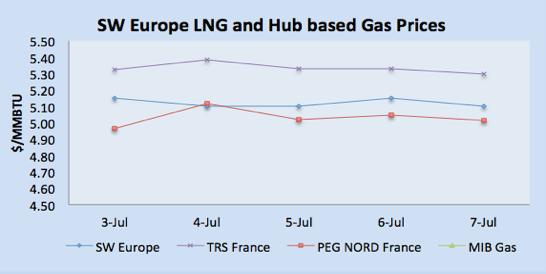

- Demand witnessed in Europe for Spain and Portugal as warm weather and uncertainty about renewable power generation in the region.

- European gas hub prices remain range bound till Thursday before closing weak on Friday due to warmer weather and stable pipeline operations, NW Europe price heard at $0.25/MMBTU discount on NBP prices. SW Europe prices remained high due to demand from Spain and Portugal and traded at TTF Gas prices level.

- US producers netback price based upon Spain gas prices is around $5.10/MMBTU, whereas for Mexico US based producers netback is around $5.30/MMBTU. Algerian LNG netback for Spain is around $5.30/MMBU whereas for France its $4.85/MMBTU.

- Major buyers from Japan, Korea, China and Taiwan are sitting with high inventories.

- Overall market sentiments are week as Korea lifted the temporary shutdown on coal power generation.

- Poland is focusing on diversifying the natural gas imports and hoping US LNG can be a potential supply source.

- CFE Mexico issued a tender for three cargoes delivery in September, however market is still long and the tender may not have any impact on the price.

- Qatar plans to enhance LNG production through its North field, this new project ill increase Qatar LNG production capacity from 77 million tons to 100 million tons by 2025.

- Qatar expansion plan will initiate a new price war in Asian market, and put hurdles for any green field project. US and Australian suppliers will face stiff competition in Qatar’s target markets.

- Hungary signed a deal with Gazprom for the supply of natural gas via pipeline by end 2019 for the supply of 8 BCM/Year (5.92 MTPA), almost equivalent to Hungary total consumption.

- Enter the plunge pool: Russian officials pour cold water on prospects for further cuts, saying it would “send the wrong message”

- CFE Energia, the fuel subsidiary of Mexican state-run utility CFE, will auction 62.3 million cubic metres per day out of 99 million cubic meter capacity across four cross-border pipelines transporting gas from the United States.

- Freeport LNG has filed an application with FERC to expand the plant with a fourth 5.1 MTPA train, that could begin operations as early as 2022, with this the total production capacity will reach 20 MTPA.

- Bangladesh is ready for importing LNG from its first FSRU based terminal, which has been given favourable tax measures by waiving off taxes on plant machinery imports. Bangladesh currently facing 700 MMSCFD of gas shortage and this terminal will deliver 500 MMSCFD with estimated re-gas & port cost of $0.59/MMBTU.

- RasGas and Petrobangla still negotiating long term LNG deal for 2.5 MTPA, the deal is expected to be finalized in August 2017.

- Pakistan and Russian signed a JV deal for the development of oil and gas sector, the deal is inked between Pakistan Oil and Gas Development Company Limited (OGDCL) and Gazprom of Russian via a MOU.

- Department of Industry, Innovation and Sciences, Australia has revised LNG export number by 3.8 million tons from 67.6 million tons to 63.8 million tons due to delay in Inpex’s Ichthys LNG project.

- My assessment on LNG market is, that price will remain weak due to over supply situation, sub-dued crude prices, US opting out from Paris climate agreement and weaker coal prices.

|

|

|

|

|

|

LNG Merchant Activity

- This week 65 vessels carrying 3.99 million tons (203.56 BCF) loaded from various supply centres, an increase of 0.71 million tons from last week.

- Resumption of loading from NWS and Russian terminal, after outage of last week.

- 19 vessels carrying 1.28 millions tons, approximately 32% of this week volume have been dispatched from Ras Laffan, Qatar.

- 4 vessels left for Indian ports while one left for Port Qasim Port, Pakistan, total volume dispatched 14.64 BCF(0.28 million ton) this week.

- Six vessels carrying 18.31 BCF departed from Nigerian port for European, South American and Asian locations

- Algeria loaded one vessel carrying 1.54 BCF for Italy.

- Pont Fortin, Trinidad & Tobago loaded three vessels with 9.15 BCF.

- Two vessels loaded this week from Sabine Pass, USA with 9.15 BCF, with one destined for Korea.

- Two vessels loaded from Brunei with load of 4.75 BCF.

- 14 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China, Korea and Singapore carrying 44.56

- Middle Eastern terminals at Das Island (UAE), Qalhat (Oman) and Ras Laffan (Qatar) loaded 23 vessels carrying 77.10 BCF for Asian and European destinations.

| Departure Date | Vessel Name | Capacity(CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 4-Jul-17 | LNG KANO | 148,565 | Bonny, Nigeria | Spain | 14-Jul-17 | 3.07 |

| 1-Jul-17 | LNG ADAMAWA | 142,656 | Bonny, Nigeria | Spain | 11-Jul-17 | 2.94 |

| 6-Jul-17 | LNG CROSS RIVER | 142,656 | Bonny, Nigeria | West Africa | 2.94 | |

| 2-Jul-17 | LNG LOKOJA | 148,471 | Bonny, Nigeria | France | 12-Jul-17 | 3.06 |

| 7-Jul-17 | GOLAR KELVIN | 162,000 | Bonny, Nigeria | Not Known | 28-Jul-17 | 3.34 |

| 7-Jul-17 | LNG RIVER ORASHI | 142,988 | Bonny, Nigeria | Not Known | 2.95 | |

| 5-Jul-17 | MARAN GAS AMPHIPOLIS | 173,400 | Punta Europa | Atlantic Region | 11-Jul-17 | 3.58 |

| 2-Jul-17 | METHANE LYDON VOLNEY | 145,000 | Punta Europa | Not Known | 14-Jul-17 | 2.99 |

| 6-Jul-17 | CHEIKH BOUAMAMA | 74,425 | Skikda, Algeria | Italy | 10-Jul-17 | 1.54 |

| 3-Jul-17 | GOLAR FROST | 160,000 | Soyo, Angola | Not Known | 20-Jul-17 | 3.30 |

| 3-Jul-17 | MARAN GAS EFESSOS | 159,800 | Pampa Melchorita, Peru | Europe | 01-Sep-17 | 3.30 |

| 5-Jul-17 | CATALUNYA SPIRIT | 135,423 | Point Fortin, Trinidad | China | 09-Jul-17 | 2.79 |

| 3-Jul-17 | SCF MELAMPUS | 170,200 | Point Fortin, Trinidad | Not Known | 12-Jul-17 | 3.51 |

| 6-Jul-17 | BW GDF SUEZ EVERETT | 138,028 | Point Fortin, Trinidad | Not Known | 12-Jul-17 | 2.85 |

| 3-Jul-17 | SM SEAHAWK | 207,000 | Sabine Pass, USA | Korea | 31-Jul-17 | 4.27 |

| 4-Jul-17 | MARAN GAS SPARTA | 162,000 | Sabine Pass, USA | Atlantic Basin | 3.34 | |

| 6-Jul-17 | COOL EXPLORER | 160,000 | Bintulu, Malaysia | Not Known | 15-Jul-17 | 3.30 |

| 2-Jul-17 | LNG PORTOVENERE | 65,272 | Bontang, Indonesia | China | 07-Jul-17 | 1.35 |

| 4-Jul-17 | SURYA AKI | 50,600 | Bontang, Indonesia | Japan | 11-Jul-17 | 1.04 |

| 3-Jul-17 | Golar Mazo | 135,000 | Bontang, Indonesia | Taiwan | 08-Jul-17 | 2.79 |

| 2-Jul-17 | PAPUA | 172,000 | Lese, Papua New Guinea | Japan | 10-Jul-17 | 3.55 |

| 6-Jul-17 | GRACE DAHLIA | 177,425 | Lese, Papua New Guinea | Japan | 14-Jul-17 | 3.66 |

| 1-Jul-17 | EXCEL | 135,344 | MIGAS LNG BATU, Indonesia | Indonesia | 2.79 | |

| 5-Jul-17 | CYGNUS PASSAGE | 145,400 | Prigorodnoye, Russia | Japan | 09-Jul-17 | 3.00 |

| 2-Jul-17 | OB RIVER | 146,791 | Prigorodnoye, Russia | Not Known | 3.03 | |

| 1-Jul-17 | AMANI | 155,000 | Sieria Oil Terminal, Brunei | Japan | 08-Jul-17 | 3.20 |

| 6-Jul-17 | BEBATIK | 75,056 | Sieria Oil Terminal, Brunei | Not Known | 1.55 | |

| 5-Jul-17 | DAPENG MOON | 147,200 | Dampier, Australia | China | 14-Jul-17 | 3.04 |

| 1-Jul-17 | LNG FLORA | 125,637 | Dampier, Australia | Japan | 12-Jul-17 | 2.59 |

| 6-Jul-17 | PACIFIC ENLIGHTEN | 147,800 | Dampier, Australia | Japan | 16-Jul-17 | 3.05 |

| 4-Jul-17 | SERI ANGGUN | 145,100 | Dampier, Australia | Japan | 15-Jul-17 | 2.99 |

| 2-Jul-17 | LNG DREAM | 147,326 | Dampier, Australia | Japan | 13-Jul-17 | 3.04 |

| 7-Jul-17 | LNG EBISU | 147,546 | Dampier, Australia | Japan | 24-Jul-17 | 3.04 |

| 3-Jul-17 | WOODSIDE GOODE | 159,800 | Dampier, Australia | Singapore | 08-Jully-2017 | 3.30 |

| 3-Jul-17 | NORTHWEST STORMPETREL | 125,525 | Dampier, Australia | Not Known | 2.59 | |

| 2-Jul-17 | ENERGY ADVANCE | 144,590 | Darwin, Australia | Japan | 12-Jul-17 | 2.98 |

| 3-Jul-17 | LNG FUKUROKUJU | 164,700 | Gladstone, Australia | Japan | 18-Jul-17 | 3.40 |

| 6-Jul-17 | LNG SATURN | 153,000 | Gladstone, Australia | Japan | 16-Jul-17 | 3.16 |

| 7-Jul-17 | LNG KOLT | 210,000 | Gladstone, Australia | Korea | 18-Jul-17 | 4.33 |

| 2-Jul-17 | METHANE BECKI ANNE | 167,416 | Gladstone, Australia | Not Known | 11-Jul-17 | 3.45 |

| 7-Jul-17 | MARAN GAS ACHILLES | 174,000 | Gladstone, Australia | China | 17-Jul-17 | 3.59 |

| 2-Jul-17 | ARCTIC DISCOVERER | 139,759 | Melokya, Norway | Lithuania | 06-Jul-17 | 2.88 |

| 4-Jul-17 | LNG PIONEER | 138,000 | Das, UAE | Japan | 20-Jul-17 | 2.85 |

| 1-Jul-17 | AL HAMRA | 137,000 | Das, UAE | India | 08-Jul-17 | 2.83 |

| 2-Jul-17 | NIZWA LNG | 145,469 | Qalhat, Oman | Japan | 18-Jul-17 | 3.00 |

| 6-Jul-17 | HANJIN MUSCAT | 138,366 | Qalhat, Oman | Korea | 20-Jul-17 | 2.85 |

| 2-Jul-17 | AL THAKHIRA | 143,517 | Ras Laffan, Qatar | Denmark | 18-Jul-17 | 2.96 |

| 3-Jul-17 | CLEAN HORIZON | 162,000 | Ras Laffan, Qatar | Egypt | 11-Jul-17 | 3.34 |

| 3-Jul-17 | AL SAMRIYA | 258,044 | Ras Laffan, Qatar | Europe | 30-Jul-17 | 5.32 |

| 3-Jul-17 | MEKAINES | 261,137 | Ras Laffan, Qatar | Far East | 25-Jul-17 | 5.39 |

| 6-Jul-17 | AL KARAANA | 205,988 | Ras Laffan, Qatar | Far East | 4.25 | |

| 1-Jul-17 | RAAHI | 138,077 | Ras Laffan, Qatar | India | 04-Jul-17 | 2.85 |

| 4-Jul-17 | DISHA | 136,026 | Ras Laffan, Qatar | India | 08-Jul-17 | 2.81 |

| 7-Jul-17 | ASEEM | 154,948 | Ras Laffan, Qatar | India | 10-Jul-17 | 3.20 |

| 3-Jul-17 | GASLOG SARATOGA | 155,000 | Ras Laffan, Qatar | Indian Basin | 10-Jul-17 | 3.20 |

| 6-Jul-17 | AL RAYYAN | 134,671 | Ras Laffan, Qatar | Japan | 23-Jul-17 | 2.78 |

| 5-Jul-17 | AL JASRA | 135,855 | Ras Laffan, Qatar | Japan | 20-Jul-17 | 2.80 |

| 3-Jul-17 | HYUNDAI ECOPIA | 146,790 | Ras Laffan, Qatar | Korea | 19-Jul-17 | 3.03 |

| 1-Jul-17 | TAITAR NO.3 | 144,627 | Ras Laffan, Qatar | Taiwan | 14-Jul-17 | 2.98 |

| 7-Jul-17 | AL DEEBEL | 142,795 | Ras Laffan, Qatar | Taiwan | 25-Jul-17 | 2.95 |

| 5-Jul-17 | MILAHA QATAR | 145,410 | Ras Laffan, Qatar | Atlantic Basin | 14-Jul-17 | 3.00 |

| 1-Jul-17 | UMM BAB | 143,708 | Ras Laffan, Qatar | Pakistan | 5-Jul-17 | 2.96 |

| 4-Jul-17 | SHAGRA | 261,988 | Ras Laffan, Qatar | Middle East | 5.41 | |

| 7-Jul-17 | GOLAR GLACIER | 162,500 | Ras Laffan, Qatar | Not Known | 3.35 | |

| 5-Jul-17 | AL REKAYYAT | 145,000 | Ras Laffan, Qatar | Not Known | 2.99 |