Market Analysis

Crude Oil

- Crude oil gained strength during the week, after displaying a poor run last week, with Brent jumped by 4.93% from last Friday and closed at $47.92 whereas WTI closed at 46.04/BBL an increase by $0.38/BBL.

- Supply fundamental remained the same as last week, however Crude gained primarily on weak dollar, traders covering the short position plus optimism about Chinese demand as PMI increased to 51.7 for June.

- Baker Hughes rig count for the first time in 24 weeks reported a marginal decline to 940 from 941, which is basically a decline of Oil rigs by 2 and now stands at 756 whereas gas rigs increased by 1 and now stands at 184.

- EIA Weekly report recorded an inventory increase of 0.10 million barrels with stock at 509.2 million barrel on 23rd June 2017 while market was expecting a 2.5 million barrel draw.

- Gasoline inventories at 241.0 million barrel, recorded a draw of 0.9 million barrel.

- Libyan production reaches 1 million barrels per day, which is also contributing to OPEC production cut in effectiveness.

- All majors financial institutions have revised the oil price forecast, with BOA cut the forecast substantially for 2017, and now$50 for Brent and $47 for WTI, Goldman slashes the three months oil price forecast by $7.50/BBL, with WTI now at$47.50/BBL

- However crude oil fundamental remains week on supply glut, till the time OPEC and US converge into something substantial, production cuts will not be effective.

Natural Gas

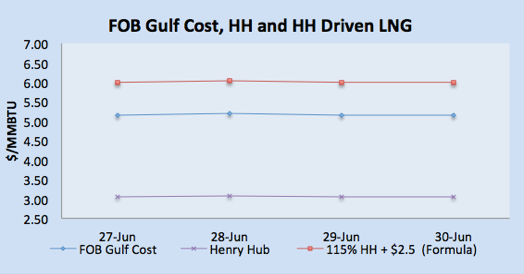

- Henry Hub prices jumped 4.78% from last Friday to $3.03/MMBTU and remained stable throughout the week and closed at $3.04/MMBTU on Friday.

- Henry Hub prices strength came in the earlier part of the week on warmer weather outlook for next ten days, however weather dimension has been incorporated into the prices for couple of weeks now.

- Henry Hub prices got support from EIA reports on Thursday as inventory rose less than expected.

- S. natural gas stocks increased by 46 BCF for the week ending June 23rd versus market expectation of 52 BCF increase.

- Working gas in storage was 2,816 BCF as of Friday, June 23rd stocks were 319 BCF less than last year at this time and 181 BCF above the five-year average of 2,816 BCF. At 2,816 BCF, total working gas is within the five-year historical range.

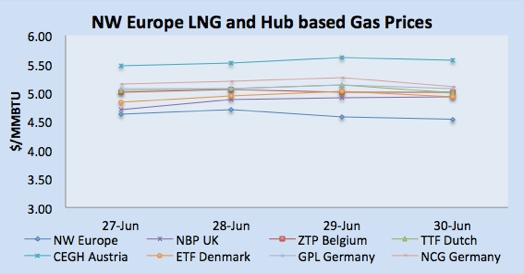

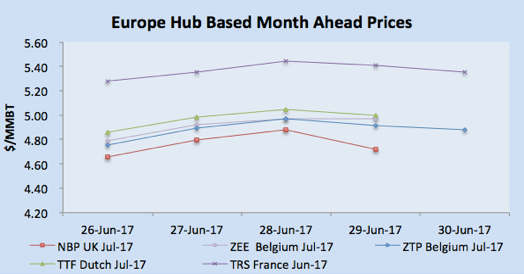

- NBP UK kept on moving north and closed at 37.94 Pence/Therm (equivalent $4.93/MMBTU) due to cooler weather and rising crude oil prices.

- NBP UK prices also got the support due to unplanned outages at Norwegian Gas SEGAL pipeline and resumption of IUK Interconnector pipeline after the annual maintenance shut down.

- Dutch and French gas prices remained strong till Thursday due to Norwegian outage, cooler temperature and rising oil prices, however prices settled down on Friday due to resumption SEGAL and IUK pipeline plus expectation of numerous LNG cargoes arriving in UK.

- TTF closed at €14.95/MWH (equivalent of $5.00/MMBTU) and PEG Nord France closed at €14.99/MWH ($5.01/MMBTU) on Friday.

Currency

- Throughout the week USD was week due to mixed US economic data outlook, plus positive economic data from Europe and political anxiety.

- On Thursday dollar index was95.60, eight months low, however on Friday the dollar got the strength after the release of US consumer data depicting optimism about economic outlook.

- US GDP rose a revised annual 1.4% in Q1, reported by Bureau of Economic Analysis, with unemployment claims still at historically low, depicting strength in labor market.

- EURO remained strong against USD through out the week and crossed 1.14 level and closed at 1.1412 on Friday.

- Euro strength attributed on weaker dollar along with positive economic data from Euro zone.

- Euro Zone Economic data: HICP inflation fell back to 1.3%, consumer spending increased in May for France, German retail sales remained strong in May along with UK Q1 GDP remained unchanged at 0.2%.

- GBP/USD closed high at 1.2995 on Friday, strength in GBP is primarily due to BOE news on removal monetary stimulus.

Weather

- Temperature remained pleasant in UK, Belgium & Netherland, and expected to be a bit warm by next week, Spain in summers and expected to be warmer next week. Germany remained around 25oC and expected to remain the same in the coming week. France is expected to be warm in the coming week whereas Portugal is expected to be around 25-27oC in the coming week.

- Temperature in Argentina remained around 15-20oC and expected to remain same in the coming week. Brazil remained around 25oC and expected to be hot next week with 30oC plus.

- Mexico will be around 23oC in the coming week same as this week

- Middle East region summer season in full swing with Egypt around 38oC, Kuwait touched 50oC, and UAE temperature reached 45o

- Indian Subcontinent in hot summer season: with temperature around 35oC in Pakistan and India for next week. India and Pakistan remained relatively cooler due to Monsoon rains.

- Summer season in North East Asia, with temperature around 33oC plus in Taiwan, 28-30oC in Korea, China 35oC, and Japan is around 30oC for next week.

- South East Asia already in hot weather with temperature in low 30o

- USA Weather: Overall weather is hot with 30oC with exception of NorthEast & Great Plains still cold.

LNG

- Asian LNG prices remained stable due to production outages in Asian supply centres of Australia, Russia and Thailand.

- Russia Sakhalin-2 is out till mid July due to annual maintenance shutdown while NWS was hit by a gas outage on 24th

- However the impact on prices has been minimal, as inventories in Japan and Korea remain full.

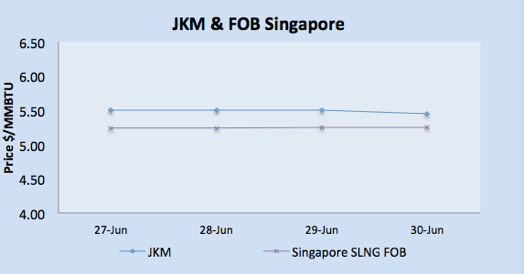

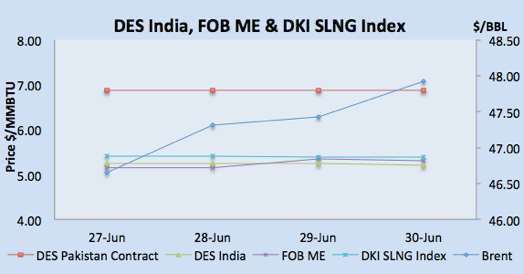

- Asian market closed on Friday with JKM at $5.45/MMBTU, FOB Singapore $5.244/MMBTU, SLNG DKI at $5.383/MMBTU. Demand focus now shifting towards winter now.

- Higher prices in Europe also gave support to Asian market this week, however outlook remained week.

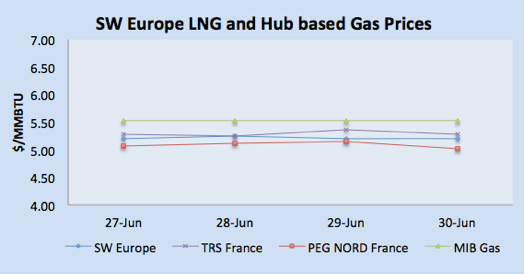

- European gas hub prices were table to strong this week due to pipeline issues, rising oil prices and weather with TTF at $5.00/MMBTU, France at equivalent of $5.01/MMBTU and Spanish market in high $5.50/MMBTU level.

- US producers netback price based upon Spain gas prices is around $5.10/MMBTU, whereas for Mexico US based producers netback is around $5.30/MMBTU.

- Demand in India is also slowing down due to good monsoon season.

- Over supply situation is pushing LNG industry liberalization, Japan Fair Trade Commission has given a ruling, which makes the destination and inability to re-sell clause void.

- Lithuania inked a deal with Cheniere for the supply of LNG at Klaipeda LNG terminal, this deal will reduce Lithuania reliance on Gazprom or perhaps starting of LNG turf war.

- India has joined the race of developing a natural gas trading hub, with Indian demand growing and potential India can be a bunkering and small scale LNG hub for the region with highest number of CNG vehicles and in effective distribution network.

- US focusing ion signing another long-term deal for LNG supply to India, this deal along with China deal should be evaluated as commercially both the countries in term of business are not effective for US LNG as of today.

- However India is trying to re-negotiating its existing agreement with Cheniere due to price unattractiveness, India has managed to re-negotiate its long term LNG supply contract with RasGas in past.

- Kogas has signed an MOU with ExxonMobil and Energy Transfer for cooperation in U.S. LNG projects, while SK Group signed an MOU with GE to jointly develop U.S. shale fields

- Kogas has signed another MOU with Sempra Energy and Australia’s Woodside for the development of the proposed Port Arthur LNG project.

- Shell’s Prelude FLNG vessel has left South Korea yard for deployment off Australia’s northwest coast where it will extract and process gas from the Prelude and Concerto fields. The commissioning is expected within a year.

|

|

|

|

|

|

LNG Merchant Activity

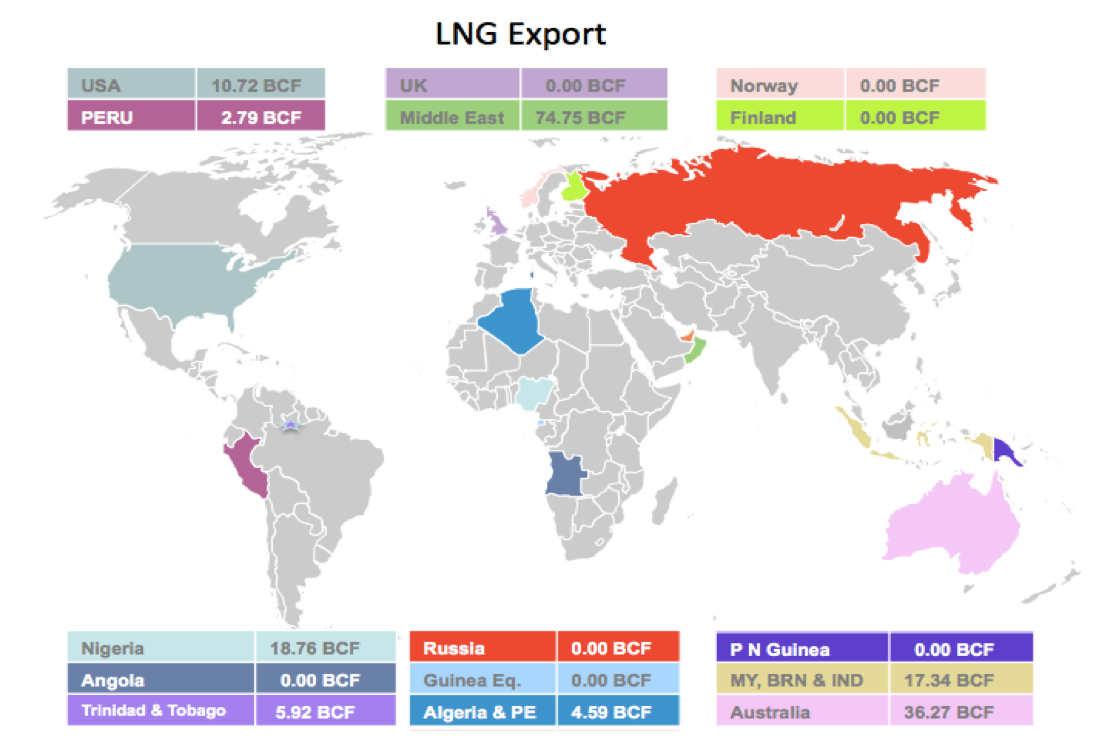

- This week 52 vessels carrying 3.28 million tons (167.20 BCF) loaded from various supply centres, decreased by 0.46 million tons from last week.

- NWS and Russian terminal didn’t load any cargo due to outage at Shaklin and NWS.

- 90 vessels carrying 6.28 millions tons, approximately 40% of total June volumes have been dispatched from Ras Laffan, Qatar.

- 15 vessels dispatched for Indian ports accounts for 48.41 BCF.

- Six vessels carrying 18.76 BCF departed from Nigerian port for European, South American and Asian locations with one destined for India.

- Algeria loaded three vessels carrying 4.59 BCF for Spain and France.

- Pont Fortin, Trinidad & Tobago loaded two vessels with 5.92 BCF.

- Three vessels loaded this week from Sabine Pass, USA with 10.72 BCF, with one destined for Mexico.

- One vessel loaded from Brunei with load of 3.20 BCF.

- 10 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China, Korea, India and Singapore carrying 32.54 BCF.

- Middle Eastern terminals at Das Island (UAE) and Ras Laffan (Qatar) loaded 21 vessels carrying 74.55 BCF for Asian destinations.

| Departure Date | Vessel Name | Capacity (CBM) | Loading Port | Discharge Country | LNG (BCF) |

| 26-Jun-17 | LNG OYO | 142,988 | Bonny, Nigeria | Argentina | 2.95 |

| 25-Jun-17 | ADAM LNG | 162,000 | Bonny, Nigeria | India | 3.34 |

| 25-Jun-17 | LNG ADAMAWA | 142,656 | Bonny, Nigeria | Not Confirmed | 2.94 |

| 30-Jun-17 | LNG LOKOJA | 148,471 | Bonny, Nigeria | Not Confirmed | 3.06 |

| 27-Jun-17 | LNG BENUE | 142,988 | Bonny, Nigeria | Spain | 2.95 |

| 29-Jun-17 | LNG FINIMA II | 170,000 | Bonny, Nigeria | Turkey | 3.51 |

| 28-Jun-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | France | 1.53 |

| 27-Jun-17 | CHEIKH BOUAMAMA | 74,425 | Skikda, Algeria | Spain | 1.54 |

| 25-Jun-17 | CHEIKH EL MOKRANI | 73,990 | Skikda, Algeria | Spain | 1.53 |

| 30-Jun-17 | SESTAO KNUTSEN | 135,357 | Pampa Melchorita, Peru | Not Confirmed | 2.79 |

| 28-Jun-17 | GALLINA | 135,269 | Point Fortin, Trinidad | Not Confirmed | 2.79 |

| 29-Jun-17 | BRITISH DIAMOND | 151,883 | Point Fortin, Trinidad | Not Confirmed | 3.13 |

| 27-Jun-17 | MARAN GAS HECTOR | 197,580 | Sabine Pass, USA | Mexico | 4.08 |

| 25-Jun-17 | MARAN GAS MYSTRAS | 159,800 | Sabine Pass, USA | Not Confirmed | 3.30 |

| 29-Jun-17 | CLEAN OCEAN | 162,000 | Sabine Pass, USA | Not Confirmed | 3.34 |

| 28-Jun-17 | PUTERI MUTIARA SATU | 134,861 | Bintulu, Malaysia | Japan | 2.78 |

| 30-Jun-17 | HYUNDAI GREENPIA | 125,000 | Bintulu, Malaysia | Not Confirmed | 2.58 |

| 24-Jun-17 | SENSHU MARU | 125,835 | Bontang, Indonesia | Japan | 2.60 |

| 29-Jun-17 | EKAPUTRA 1 | 136,400 | Bontang, Indonesia | Japan | 2.81 |

| 28-Jun-17 | MARIB SPIRIT | 163,280 | Bontang, Indonesia | Not Confirmed | 3.37 |

| 28-Jun-17 | AMANI | 155,000 | Sieria Oil Terminal, Brunei | Not Confirmed | 3.20 |

| 28-Jun-17 | WOODSIDE DONALDSON | 162,620 | Dampier, Australia | Japan | 3.36 |

| 25-Jun-17 | NORTHWEST SEAEAGLE | 125,541 | Dampier, Australia | Pacific Ocean | 2.59 |

| 29-Jun-17 | FUJI LNG | 144,596 | Dampier, Australia | Pcific Basin | 2.98 |

| 27-Jun-17 | PACIFIC NOTUS | 137,006 | Darwin, Australia | Japan | 2.83 |

| 27-Jun-17 | CESI BEIHAI | 240,000 | Gladstone, Australia | China | 4.95 |

| 25-Jun-17 | BW PAVILION LEEARA | 161,880 | Gladstone, Australia | China | 3.34 |

| 30-Jun-17 | BW PAVILION VANDA | 161,880 | Gladstone, Australia | China | 3.34 |

| 30-Jun-17 | YK SOVEREIGN | 124,582 | Gladstone, Australia | Korea | 2.57 |

| 29-Jun-17 | MARAN GAS ULYSSES | 174,000 | Gladstone, Australia | Pacific Basin | 3.59 |

| 25-Jun-17 | METHANE RITA ANDREA | 145,000 | Gladstone, Australia | Pacific Ocean | 2.99 |

| 27-Jun-17 | ISH | 137,512 | Das, UAE | Japan | 2.84 |

| 28-Jun-17 | HANJIN SUR | 138,333 | Qalhat, Oman | Korea | 2.85 |

| 30-Jun-17 | TEMBEK | 211,885 | Ras Laffan, Qatar | China | 4.37 |

| 29-Jun-17 | EJNAN | 143,815 | Ras Laffan, Qatar | Denmark | 2.97 |

| 30-Jun-17 | LENA RIVER | 154,880 | Ras Laffan, Qatar | Egypt | 3.20 |

| 27-Jun-17 | AL MARROUNA | 149,539 | Ras Laffan, Qatar | Europe | 3.09 |

| 28-Jun-17 | ASEEM | 154,948 | Ras Laffan, Qatar | India | 3.20 |

| 30-Jun-17 | AL KHOR | 135,295 | Ras Laffan, Qatar | Japan | 2.79 |

| 27-Jun-17 | AL UTOURIYA | 211,879 | Ras Laffan, Qatar | Korea | 4.37 |

| 29-Jun-17 | HYUNDAI COSMOPIA | 134,308 | Ras Laffan, Qatar | Korea | 2.77 |

| 25-Jun-17 | SK SUNRISE | 135,505 | Ras Laffan, Qatar | Korea | 2.80 |

| 25-Jun-17 | AL KHARAITIYAT | 211,986 | Ras Laffan, Qatar | Not Confirmed | 4.37 |

| 28-Jun-17 | MARAN GAS PERICLES | 209,000 | Ras Laffan, Qatar | Not Confirmed | 4.31 |

| 29-Jun-17 | AL SHAMAL | 213,536 | Ras Laffan, Qatar | Not Confirmed | 4.41 |

| 25-Jun-17 | BROOG | 136,359 | Ras Laffan, Qatar | Not Confirmed | 2.81 |

| 25-Jun-17 | AL SAFLIYA | 210,100 | Ras Laffan, Qatar | Pacific Basin | 4.33 |

| 29-Jun-17 | AL GHARIYA | 205,941 | Ras Laffan, Qatar | Pacific Region | 4.25 |

| 27-Jun-17 | MARAN GAS ASCLEPIUS | 142,906 | Ras Laffan, Qatar | Pakistan | 2.95 |

| 25-Jun-17 | AL THUMAMA | 216,325 | Ras Laffan, Qatar | Spain | 4.46 |

| 30-Jun-17 | TAITAR NO.3 | 144,627 | Ras Laffan, Qatar | Taiwan | 2.98 |

| 27-Jun-17 | AL HUWAILA | 214,716 | Ras Laffan, Qatar | Thailand | 4.43 |