If you are interested in crude oil as an investor, an analyst or a consumer there is no shortage of conflicting opinions out there. For industry outsiders it is even worse – crude oil price outlook is a puzzle with multiple pieces that are impossible to put together.

We are going to run out of oil! No we are not. Alternate energy is going to completely replace fossil fuels when it comes to power generation in coming year! Not going to happen in the next forty years. Electric and hybrid vehicles are going to kill the petrochemical industry by reducing demand for petrol and diesel down to zero! Wrong again. The contradiction and conflicts are endless. Lets see if we can find answers to some of these questions and chart a path of clarity through them.

There are three primary schools of thoughts when it comes to predicting the future price of crude oil.

- Prices are going higher. Oil prices are at a historical low because of a market glut. They are likely to move up when the glut clears up. The supply glut started building up in 2014 and has had no significant reduction in the last three years. The glut is likely to disappear in the next two years as demand for crude oil consumption comes back. Oil is likely to go up and back to higher levels (US$ 80 – US$110) as we move forward in time towards 2025-2030.

- Prices are going lower. Oil prices are at a historical low because of a market glut. The glut is not going anywhere because the growth in demand for crude oil has slowed down significantly. Demand is not likely to come back anytime soon because of structural reasons. Some factors are linked to supply side shocks. Others are linked to rationalization of demand on account of better efficiency and technology improvements. Oil is likely to head back to the $20 – $30 level when the market realizes that the new equilibrium is significantly lower.

- Prices have found a new equilibrium. Oil prices have found a new stable price level in the mid $40. They are likely to hover around this range for the near future. $40 is now the new benchmark.

Which one of these views is right? What are these structural reasons markets refer to? What is the likely future of crude oil and how will that impact the global economy?

The two primary schools of thoughts originate from two different groups of stake holders. The oil prices are likely to go high school is directly or indirectly linked to groups that benefit from higher oil prices. Oil producing nations and large production, exploration and distribution companies would like to see prices drift higher and their default thinking and opinions reflect that. The natural optimism of business that whatever we are doing is rational and in the collective best interest of the industry.

Similarly the low price school of thought is driven by industry shorts and technologists. Same rationale as the first group – default group think. The reality is somewhere in between.

The EIA Annual Energy Outlook (AEO) report

One way of drilling down to the actual signal embedded in all the analysis floating around the world is to look at two of the largest markets on the demand side. US and China. If we can build a better model of supply in demand in these two markets the remaining pieces of the puzzle will fall in place.

Fortunately for us EIA – the US government agency (Energy Information Administration) produces a great deal of data and public analysis on supply, consumption and inventory trends within energy markets. In this series of posts we want to look closely at some of the EIA work and see if we can use it as a foundation to build our own models.

To a student of oil opinions don’t matter. Methodologies do. EIA produces an Annual Energy Outlook (AEO) report every year that updates their base case for long and short term oil price forecasts. The most recent report was published on 5th January 2017 and remains unaffected by biases introduced by the transition of power in the US from the Democratic to the Republican party.

While the report is limited to US energy trends, the approach used is quite instructive and can be applied to global trends or other specific regional markets such as China, India and Western Europe. Even without extending the approach to other markets, remember that US is the largest global consumer of energy products as well as the one with the deepest financial markets where these products trade. In 2008 it was the pressure wave created by the same financial markets that first took prices to $147 a barrel and then brought them down to US$ 33 a barrel.

Our interest is in the following specific questions given the coverage we have been seeing in recent years on the impact of technology on crude oil.

- What impact would better fuel efficiency, Plugin Electrical Vehicles (PEV), Hybrids and improving fuel cell technology have on future oil demand? This question can be answered by breaking down consumption and growth within the logistics and transportation sector. The primary consumption of this sector is petrol or gasoline (motor gas), diesel, jet fuel and lubricants.

- What impact would a switch to natural gas and alternate energy sources (renewables) have on oil consumption within power generation? Power generation from a petrochemical point of view is essentially fuel oil.

- Do the same technologies also impact usage of fuel oil by residential and commercial customers? Heating solutions and platforms at residential and commercial real estate use fuel oil.

- How is industrial consumption of crude oil likely to change over the next few years?

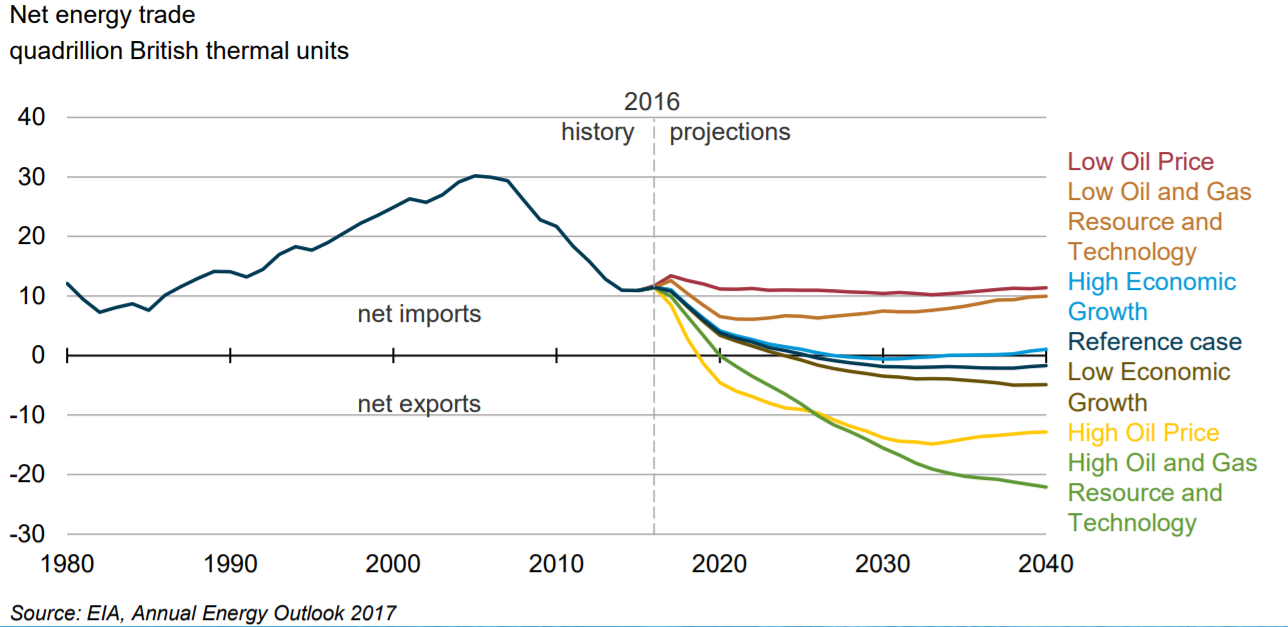

A better understanding of US needs can help shape our opinion with respect to what the future holds for oil prices. The EIA AEO report breaks down oil price forecast by breaking down oil consumption by sectors. It further analyzes this data by reviewing consumption and growth under a collection of scenarios. The first one is what is called the reference case. A most likely base case created by extending the current trends in technology, resources, demand and growth. The reference case is supplemented by 6 other cases.

- High availability of oil and gas resources and technology improvement within the industry

- High economic growth

- High oil prices

- Low oil prices

- Low economic growth

- Low availability of oil and gas resources and low technology improvement.

The 2017 EIA AEO report does not bode well for future oil demand. Under the 7 scenarios including the reference case there are only two scenarios where US does not end up as a net exporter of energy products. The transition happens as early as 2020. So even if the supply glut that has been casting a dark shadow on prices since 2014 clears up, a much bigger glut is likely to hit the market within the next 24 months as supply and demand curves within the US market shift. An initial read of the report suggests a mostly negative outlook when it comes to the future of oil prices.

A number of factors have been driving this outlook. To better understand where oil is going we have to understand how crude oil is used and what consumption looks like. Oil consumption is broken down into four primary uses.

- Logistics and transportation – (gasoline, petrol and diesel for roads. Jet fuel for airlines)

- Power generation – fuel oil or natural gas for power plants

- Buildings (residential and commercial) and Heating – Heating or fuel oil

- Industrial usage – crude as well as refined downstream products.

We review the AEO report in the series of posts that follow and take a deeper look at:

- Projected growth in Electric, Hybrid and battery powered vehicles. What are these numbers likely to be as a percentage of global automobile vehicle pool? What would be the impact of these figures on consumption? The projected numbers for electric and hybrid vehicles max out at about 10% of total motor vehicle pool. So we are not looking at a significant share of the market. However higher fuel efficiency within conventional vehicles does have a significant impact on total consumption.

- Expected growth in demand in the logistics and transportation sector. Projected figure are stable or with minimal growth. The only component with consistent positive growth is the airline industry.

- The expected transition in power generation from fossil fuels to renewable sources and the likely reduction in industrial consumption of petrochemical products. Industrial consumption is likely to head south and alternate and renewable sources will represent a larger source of the future power generation fuel mix. But we won’t see deprecation of existing technologies till about 2060.

- The collective impact of these trends on global demand and the likelihood of the supply side glut increasing in size rather than decreasing over the next 3 – 10 years. In the next 20 years total increase in demand and consumption is likely to remain under 100 million barrels per day of crude oil under a number of the projected scenarios in the AEO report. The current demand is at 96 million barrels per day of crude oil.

Hang in to your seat belts it is going to be an interesting ride.