Market Analysis

Crude Oil

- Crude prices remained bearish till Wednesday on over supplied situation, however gained momentum from Thursday on strong demand number, US rig data, weaker USD and traders attempt to cover short positions.

- Brent price closed at $52.88, increased by 1.50% from last Friday closing price of $52.10/BBL, whereas WTI closed at $48.51, rose by 1.93% from Monday price of $47.59/BBL.

- OPEC production cut has been proving ineffective as out of 1.72 million B/D pledged production cut by OPEC, 1.61 million B/D is nullified by production increase from US, Nigeria and Libya.

- There have been comments across crude oil landscape urging OPEC for further deeper production cuts for longer term and strict compliance.

- EIA Weekly report reported a draw of 8.9 million barrels with stock at 466.5 million barrel on 11th August 2017; a much larger draw then market expectation, pushing the inventories to the lowest level since January 2016.

- Gasoline inventories at 231.1 million barrel reported on 11th August 2017, same as last week number.

- Baker Hughes rig count reported a decrease of 5 oil rigs, with total standing at 763, whereas gas rig increased by 1 and now at 182, with one rig increase as miscellaneous, with total number of rigs at 946.

- US production jumped by 79,000 BPD to over 9.5 million bpd last week, its highest level since July 2015.

- In my opinion, current price hike is based upon short-term perspective as summer driving season is nearing end in North America plus over increasing supply from US, Nigeria and Libya will keep pressure on prices to remain bearish.

Natural Gas

- Henry Hub prices closed at $2.93/MMBTU, down by 1.68% from last Friday.

- Bullish tone is attributed to long supply situation prevailing.

- Weather is going to be warm all across USA for the next week, and weather component already incorporated in the demand.

- EIA showed domestic supplies of natural gas rose by 28 BCF for the week ending August 4 against market expectation of 37 BCF.

- Working gas in storage was 3,082 BCF as of Friday, August 11th 2017, an increase of 53 BCF from previous week. Stocks were 254 BCF less than last year at this time and 55 BCF above the five-year average. At 3,082 BCF, total working gas is within the five-year historical range.

- September Natural Gas futures settled at $2.885, whereas $2.921/MMBTU for October delivery on Friday, putting the prices in backwardation.

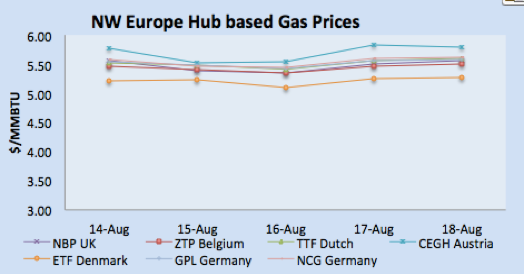

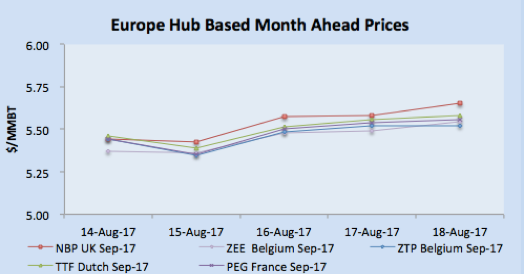

- NBP UK turned bullish from Thursday due to supply issue from Norwegian gas field along with news of warmer weather next week and volatile crude prices.

- An LNG Cargo is expected to discharge into the UK this week, with delivery expected on 19th August.

- Renewable from wind and Solar is expected to be stable for the coming week.

- NBP UK day ahead prices closed 43.1432 Pence/Therm (equivalent $$5.55/MMBTU) on Friday, increased by 1.64% from last Friday of 42.4490 Pence/Therm.

- NBP UK curve market for October and November closed at 44.1500 Pence/Therm & 47.1200 Pence/Therm (equivalent of $5.68/MMBTU & $6.06/MMBTU), highlighting winter price focus now.

- Dutch price remained stable while French gas prices remained range bound on weather and crude oil prices. French gas prices also bearish on adequate supply plus two in coming LNG vessel by end of August 2017.

- Gas Prices in Iberian Peninsula remained stable due to hot weather, however supply is adequate.

- TTF closed at €16.27/MWH (equivalent of $5.61/MMBTU), PEG Nord France closed at €15.93/MWH ($5.49/MMBTU), and Spanish at €16.40/MWH ($5.65/MMBTU) on Friday.

- In the future market TTF October closed at €16.29/MWH ($5.61/MMBTU) and November at €16.85/MWH ($5.81/MMBTU), however major trading is witnessed in TTF versus any other price marker in European market.

Currency

- USD remained volatile with bearish factor dominating over bullish factor, this week bullish factors are US consumer sentiment index and labor data, whereas bearish factors US political drama, Fed meeting news and terror attack in Spain.

- Preliminary reading of consumer sentiment index data for August has strengthened confidence on US economy. The index rose to 97.6 in August against expectation to reach at 94 from 93.4 reading in July.

- S. Department of Labor reported on Thursday that the number of people who filed for unemployment assistance in the U.S. last week fell more than expected.

- Eight CEOs left business advisory councils in a protest over President Trump remarks on weekend violence in Virginia, plus firing of Whitehouse Chief Strategist, Steve Banon.

- Investors remained cautious following a terrorist attack in Spain.

- Minutes of Fed July policy meeting released on Wednesday depicted that there is still division among the members over the need to raise interest rates.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, fell to 93.42 on Friday.

- EUR/USD rose to $1.1759, as ECB’s July policy meeting showing officials warned that the recent surge in the euro could hamper the central bank’s efforts to get inflation closer to its target of below, but close to, 2%.

- GBP/USD closed at 1.2872; primarily on weak UK data along with Bank of England rate hike uncertainty.

- USD/JPY fell to 109.19, as US-North Korea tension is causing investor to focus more on Japanese Yen as safe haven currency.

- AUD/USD remained closed at 0.79275, stronger against USD on Friday due to weaker USD.

- Chinese Yuan fell to 6.67 on Friday.

Weather

- UK, Belgium and Netherland remained around 20oC and expected to be in the range of 20-25oC next week with some showers.

- France remained cooler around 20-25 oC, and expected to remain same next week.

- Hot weather in Spain & Portugal, temperature touched 40oC in Spain before cooling down to 30oC and Portugal remained between 30-35oC, Spain will be around 35oC whereas Portugal will be between 26-32oC in the coming week.

- Temperature in Argentina remained around between 16-18oC, and expected to be in the same range next week.

- Brazil remained hot with temperature around 25-30oC, and expected to remain hot next week.

- Mexico is getting warm with temperature around 25-30oC and expected to remain warm next week.

- Middle East region summer season in full swing with Egypt around 35oC, Kuwait 45oC plus, and UAE temperature reached 45oC and will remain the same next week.

- Indian Subcontinent in in monsoon season with temperature in Pakistan and India around 35oC, same weather profile for next week.

- Temperature remained hot in North East Asia, with temperature around 38oC in Taiwan, around 35oC in Korea, China 35oC, and Japan is around 30-32oC, weather is expected to cool down by couple of degrees but still hot weather prevailing in North East Asia.

- South East Asia already in hot weather, Thailand around 35oC, Indonesia and Malaysia ranging between 32oC, and will remain same next week.

- USA Weather: Overall weather is remained warm, overall its summer season and weather has entered into summer temperature profile.

LNG

- LNG prices in Asian market remained steady, as weather component already built in and end users have already replenished for their requirement till September.

- Asian markets are now focusing on October delivery with Japanese apetitie reduced due to weather cooling down a bit.

- Supply situation in the region is long as cargoes availability from Malaysia, Indonesia, Angola, Nigeria along with Wheatsone from Australia.

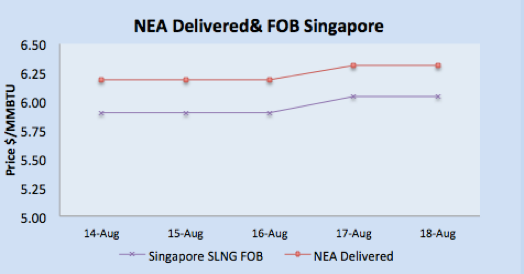

- Asian prices were heard to close on Friday with JKM $6.250/MMBTU, SLNG NEA Delivered at $6.310/MMBTU and FOB Singapore at $6.040/MMBTU,

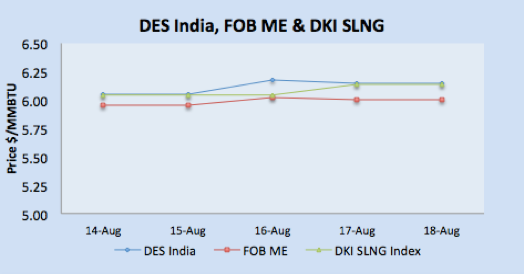

- Price level in Indian and Middle Eastern market remained in-syn with Asian prices with DES India at $6.150/MMBTU level whereas Middle Eastern at $6.00/MMBTU on FOB level.

- JKM Future curve market closed at $6.25/MMBTU for October, $6.60/MMBTU for November and $6.95/MMBTU for December, moved a bit down from last week.

- Demand for imported LNG in European markets is low, due to ample pipelined gas supply plus arrival and expected arrival of LNG vessels.

- Imported LNG offers in North West Europe were heard around 96% of NBP October future price around $5.45/MMBTU level. NBP UK closed at equivalent prices level of $5.68/MMBTU and TTF at $5.61/MMBTU for October delivery.

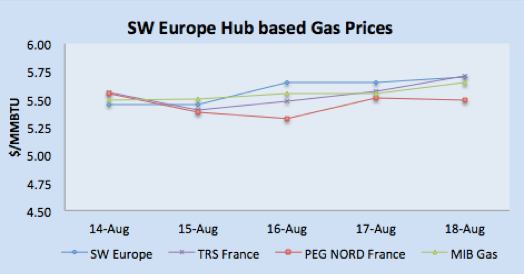

- South Western gas prices were steady during the weak as due to weather, and prices were around $5.70/MMBTU level, based upon October future curve closing at €46/MWH ($5.70/MMBTU) for PEG Nord.

- Price remained steady for Spain and Portugal during the weak for Day Ahead market and MIBGAS closed at €16.40/MWH ($5.65/MMBTU) on Friday.

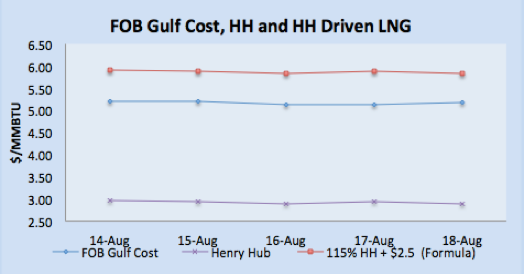

- Current Asian prices base upon October future prices converts into $5.15-$5.20/MMBTU for US producers, along with same netback for European prices, as based upon freight cost Golf Cost FOB price for October delivery comes around $5.20/MMBTU level for UK, France and Spanish region.

- Demand is expected to be increasing by 10% on Year on Year basis in China, as per report from National Energy Administration. This year’s total consumption stands at 230 BCM.

- It was reported that Pakistan is focusing on African LNG producers for LNG supply, this needs to be looked at closely as based upon freight economics and supply adequacy, Qatar is the most economical choice for Pakistan, India and Bangladesh.

- PETRONAS & Mitsui are focusing on Indian market, with PETRONAS keen on buying a stake in Ennore LNG import terminal whereas Mitsui eyeing to secure 11% stake in Swan Energy’s FSRU project in Gujrat.

Author’s Comments

- Current hike in Brent pricing will induced some pressure on spot prices as buyers with flexibility on reducing long term contract will focus more SPOT prices, so crude price rally may put some bullish pressure on LNG prices in short term.

- Looking at European hub future price for November onward for NBP UK, TTF, PEG Nord and Iberian Peninsula along with Asian prices, seems like prices will remain subdued in October and will start climbing for November delivery as winter procurement will start.

- Short term prices, looking at resumption of supply along with weather profile and Brent price trend, it seems like prices will be steady to bearish in the coming week.

|

|

|

|

|

|

LNG Merchant Activity

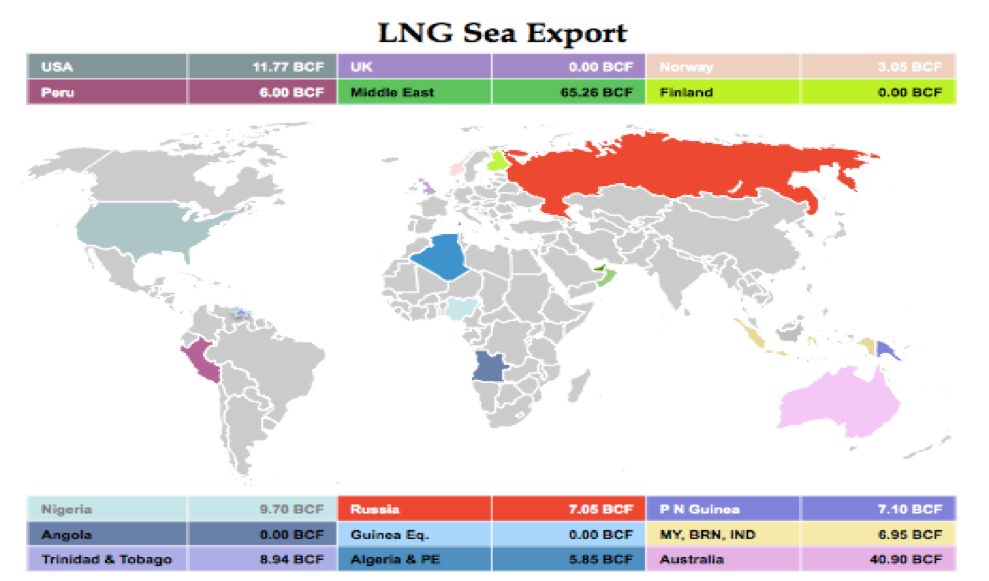

- 54 vessels carrying 3.38 million tons (172.59 BCF) loaded from various supply centres, a decrease by 0.35 million tons from last week.

- Primarily decrease in the quantities is from Qatar, Nigeria, US, Indonesia & Norway in comparison from last week.

- Still no loading from Angola this week.

- 47 vessels carrying 3.38 million tons, have been dispatched from Ras Laffan, Qatar so far in the month of August, this represent 30% of total global trade on Month to date basis.

- 3 vessels left for Indian ports with 10.29 BCF.

- Three vessels carrying 9.70 BCF departed from Nigerian port, one for European destination.

- Algeria loaded two vessels carrying 3.06 BCF for Italy and Spain.

- Pont Fortin, Trinidad & Tobago loaded three vessels with 8.94 BCF, two cargoes destined for European destinations.

- Two vessel loaded from Brunei with load of 4.34 BCF.

- Thirteen vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Korea carrying 40.90 BCF.

- One cargoes left for France with 3.05 BCF from Norway

- Middle Eastern terminal at Das Island (UAE) loaded two vessels carrying 5.90 BCF for Kuwait and North East Asia.

| Departure Date | Vessel Name | Capacity(CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 13-Aug-17 | GOLAR SNOW | 160,000 | Bonny, Nigeria | Not Known | 3.30 | |

| 17-Aug-17 | METHANE MICKIE HARPER | 167,400 | Bonny, Nigeria | Not Known | 09-Sep-17 | 3.45 |

| 18-Aug-17 | LNG BENUE | 142,988 | Bonny, Nigeria | Portugal | 26-Aug-17 | 2.95 |

| 14-Aug-17 | BILBAO KNUTSEN | 135,049 | Punta Europa, Africa | Atlantic Basin | 20-Jul-17 | 2.79 |

| 16-Aug-16 | CHEIKH BOUAMAMA | 74,425 | Skikda, Algeria | France | 18-Aug-17 | 1.54 |

| 15-Aug-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | Italy | 16-Aug-17 | 1.53 |

| 16-Aug-17 | GASLOG SHANGHAI | 154,948 | Pampa Melchorita, Peru | 3.20 | ||

| 17-Aug-17 | METHANE PRINCESS | 136,086 | Pampa Melchorita, Peru | Not Known | 18-Aug-17 | 2.81 |

| 16-Aug-17 | MARAN GAS LINDOS | 159,800 | Point Fortin, Trinidad | 04-Sep-17 | 3.30 | |

| 17-Aug-17 | BRITISH MERCHANT | 138,517 | Point Fortin, Trinidad | Gibraltar | 05-Sep-17 | 2.86 |

| 14-Aug-17 | IBERICA KNUTSEN | 135,230 | Point Fortin, Trinidad | Spain | 24-Aug-17 | 2.79 |

| 17-Aug-17 | GOLAR SEAL | 160,000 | Sabine Pass, USA | Not Known | 3.30 | |

| 13-Aug-17 | HYUNDAI PRINCEPIA | 178,602 | Sabine Pass, USA | Panama | 17-Aug-17 | 3.68 |

| 16-Aug-16 | GASLOG GLASGOW | 232,000 | Sabine Pass, USA | Singapore | 21-Aug-17 | 4.79 |

| 16-Aug-17 | LNG AQUARIUS | 126,750 | Bontang, Indonesia | Indonesia | 19-Aug-17 | 2.61 |

| 17-Aug-17 | PAPUA | 172,000 | Lese, Papua New Guinea | Korea | 26-Aug-17 | 3.55 |

| 14-Aug-17 | KUMUL | 172,000 | Lese, Papua New Guinea | Taiwan | 22-Aug-17 | 3.55 |

| 14-Aug-17 | ENERGY PROGRESS | 195,000 | Prigorodnoye, Russia | Italy | 10-Jul-17 | 4.02 |

| 17-Aug-17 | OB RIVER | 146,791 | Prigorodnoye, Russia | Japan | 29-Aug-17 | 3.03 |

| 16-Aug-16 | ABADI | 135,269 | Sieria Oil Terminal, Brunei | Not Known | 2.79 | |

| 18-Aug-17 | BELANAK | 75,000 | Sieria Oil Terminal, Brunei | Romania | 10-Jul-17 | 1.55 |

| 13-Aug-17 | NORTHWEST SANDPIPER | 125,042 | Dampier, Australia | Japan | 2.58 | |

| 14-Aug-17 | NORTHWEST SWAN | 140,500 | Dampier, Australia | Japan | 24-Aug-17 | 2.90 |

| 17-Aug-17 | ENERGY HORIZON | 177,441 | Dampier, Australia | Japan | 28-Aug-17 | 3.66 |

| 16-Aug-17 | DAPENG SUN | 147,200 | Dampier, Australia | Not Known | 3.04 | |

| 15-Aug-17 | NORTHWEST SANDERLING | 125,452 | Dampier, Australia | Pacific Basin | 22-Aug-17 | 2.59 |

| 18-Aug-17 | FUJI LNG | 144,596 | Dampier, Australia | Pacific Basin | 29-Aug-17 | 2.98 |

| 14-Aug-17 | ENERGY ADVANCE | 144,590 | Darwin, Australia | Japan | 23-Aug-17 | 2.98 |

| 18-Aug-18 | BW PAVILION VANDA | 161,880 | Gladstone, Australia | China | 29-Aug-17 | 3.34 |

| 15-Aug-17 | BW PAVILION LEEARA | 161,880 | Gladstone, Australia | China | 27-Aug-17 | 3.34 |

| 14-Aug-17 | GRACE ACACIA | 146,791 | Gladstone, Australia | China | 24-Aug-17 | 3.03 |

| 18-Aug-17 | YK SOVEREIGN | 124,582 | Gladstone, Australia | Korea | 27-Aug-17 | 2.57 |

| 14-Aug-17 | MARAN GAS PERICLES | 209,000 | Gladstone, Australia | Not Known | 24-Aug-17 | 4.31 |

| 18-Aug-18 | MARAN GAS ROXANA | 173,400 | Gladstone, Australia | Not Known | 3.58 | |

| 16-Aug-17 | ARCTIC LADY | 147,835 | Melokya, Norway | France | 28-Aug-17 | 3.05 |

| 17-Aug-17 | LNG PIONEER | 138,000 | Das, UAE | Not Known | 2.85 | |

| 16-Aug-17 | SALALAH LNG | 148,174 | Qalhat, Oman | Kuwait | 22-Aug-17 | 3.06 |

| 18-Aug-17 | CADIZ KNUTSEN | 135,240 | Ras Laffan, Qatar | Argentina | 10-Sep-17 | 2.79 |

| 18-Aug-17 | AL RUWAIS | 205,994 | Ras Laffan, Qatar | China | 31-Aug-17 | 4.25 |

| 16-Aug-17 | MURWAB | 205,971 | Ras Laffan, Qatar | India | 21-Aug-17 | 4.25 |

| 15-Aug-17 | RAAHI | 138,077 | Ras Laffan, Qatar | India | 18-Aug-17 | 2.85 |

| 18-Aug-17 | ASEEM | 154,948 | Ras Laffan, Qatar | India | 22-Aug-17 | 3.20 |

| 14-Aug-17 | AL WAJBAH | 134,562 | Ras Laffan, Qatar | Japan | 29-Aug-17 | 2.78 |

| 15-Aug-17 | AL DAFNA | 261,988 | Ras Laffan, Qatar | Japan | 29-Aug-17 | 5.41 |

| 17-Aug-17 | AL WAKRAH | 134,624 | Ras Laffan, Qatar | Japan | 01-Sep-17 | 2.78 |

| 14-Aug-17 | SK STELLAR | 135,540 | Ras Laffan, Qatar | Korea | 29-Aug-17 | 2.80 |

| 16-Aug-17 | HYUNDAI TECHNOPIA | 134,524 | Ras Laffan, Qatar | Korea | 01-Sep-17 | 2.78 |

| 16-Aug-17 | AL AREESH | 148,786 | Ras Laffan, Qatar | Mediterian | 28-Aug-17 | 3.07 |

| 14-Aug-17 | UMM BAB | 143,708 | Ras Laffan, Qatar | Not Known | 27-Aug-17 | 2.96 |

| 13-Aug-17 | AL SHAMAL | 213,536 | Ras Laffan, Qatar | Not Known | 28-Aug-17 | 4.41 |

| 13-Aug-17 | MARAN GAS APOLLONIA | 164,000 | Ras Laffan, Qatar | Not Known | 6-Sep-17 | 3.38 |

| 15-Aug-17 | AAMIRA | 260,912 | Ras Laffan, Qatar | Not Known | 01-Sep-17 | 5.38 |

| 14-Aug-17 | TAITAR NO.2 | 144,627 | Ras Laffan, Qatar | Taiwan | 28-Aug-17 | 2.98 |

| 16-Aug-17 | GOLAR ICE | 160,000 | Ras Laffan, Qatar | Not Known | 3.30 |