Market Analysis

Crude Oil

- Crude prices remained bullish through out the weak due to weaker USD and inventory number, US rig data, though second half of the week the market sentiments focused on Hurricane Harvey, which brought additional bullish dimension.

- The crude and gasoline prices went up on Friday as Hurricane Harvey was heading directly for the coast of Texas between Houston and Corpus Christi, where many oil refineries are located.

- Market will follow the after impact of Hurricane Harvey as timing of resumption of operations of refineries will have an impact on crude prices

- Brent price closed at $52.41, increased by 1.45% from Monday, whereas WTI closed at $48.51, rose by 1.06% from Monday price of $47.87/BBL.

- OPEC in it next meeting scheduled for 22nd September 2017 will evaluate all the options including production cuts and extension of production cut.

- There is need for effective compliance on OPEC production cut as so far OPEC production cut has been ineffective due to rising production from US, Libya and Nigeria along with news of non compliance from UAE and KSA.

- EIA Weekly report reported a draw of 3.3 million barrels with stock at 463.2 million barrel on 18th August 2017; against a market expectation of 3.5 million barrels.

- Gasoline inventories at 229.9 million barrel reported on 18th August 2017, inventory decreased by 1.2 million barrels on week on week basis.

- Baker Hughes rig count reported a decrease of 4 oil rigs, with total standing at 759, whereas gas rig decrease by 2 and now at 180, with total number of rigs at 940.

- US production jumped by 26,000 BPD to over 9.528 million BPD from last week and increase of 980,000 BPD on Year on Year basis.

Natural Gas

- Henry Hub prices closed at $2.89/MMBTU, down by 3.36% from Monday primarily due to Hurricane Harvey, as short term demand is expected to grow as next week is expected to be warm in US.

- Beyond one week there is a bearish trend due to weather outlook, however post Hurricane Harvey impact need to be assessed first.

- EIA showed domestic supplies of natural gas rose remained the same as previous week, averaging 78.7 BCFD, whereas demand increased 4% compared to last week with residential and commercial sector increased by 5% and export to Mexico by 2%.

- Working gas in storage was 3,125 BCF as of Friday, August 18th 2017, an increase of 43 BCF from previous week and expectations were of 45 BCF increase. Stocks were 223 BCF less than last year at this time and 45 BCF above the five-year average. At 3,125 BCF, total working gas is within the five-year historical range.

- September Natural Gas futures settled at $2.896/MMBTU, whereas $2.925/MMBTU for October delivery on Friday, depicting neutral dimension of NG price movement before winter season.

- NBP UK turned bullish from Monday as NBP UK system opened extremely short due to Norwegian outage along with stable crude prices and lower nomination from LNG terminals.

- Nomination from South Hook terminal reduced as there is no LNG vessel arrival expectation for next two week plus weather remained on the warmer side.

- Power generation remained weak this week from wind however expected to rise next week.

- NBP UK day ahead prices closed 44.8120 Pence/Therm (equivalent $$5.49/MMBTU) on Friday, increased by 3.87% from last Friday of 43.1432 Pence/Therm.

- NBP UK curve market for October and November closed at 44.4300 Pence/Therm & 47.6900 Pence/Therm (equivalent of $5.72/MMBTU & $6.14/MMBTU), putting bullish trend on prices.

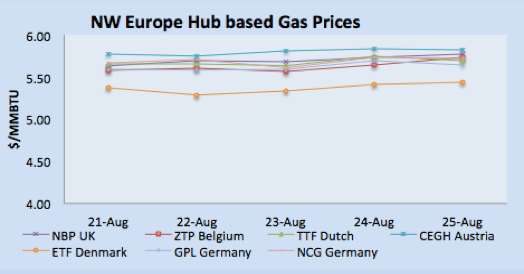

- Dutch & French price remained stable throughout the week as start of the week there were lower Russian flow due to Kondratki maintenance along with lower wind power availability and issue with French Nuclear utility. Weather is also attributing to demand to high temperature.

- Gas Prices in Iberian Peninsula remained stable due to hot weather, however supply is adequate.

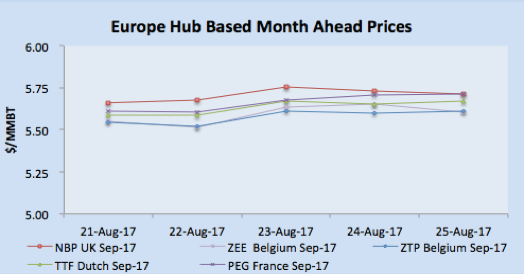

- TTF closed at €16.38/MWH (equivalent of $5.70/MMBTU), PEG Nord France closed at €16.38/MWH ($5.70/MMBTU), and Spanish at €16.60/MWH ($5.78/MMBTU) on Friday.

- In the curve market TTF October closed at €16.29/MWH ($5.67/MMBTU) and November at €16.87/MWH ($5.87/MMBTU), PEG Nord at €16.55/MWH ($5.76/MMBTU) & €17.29/MWH ($6.02/MMBTU) and Spanish for Month Ahead €17.90/MWH ($6.14/MMBTU)..

Currency

- USD remained weak from the start of week following Friday news of Steve Banon and bearish factors overwhelming bullish trend through out the week, the bearish factors have been US internal political tension and uncertainty, weak US economic data, and bullish factor was expectation of rate hike news from Fed.

- US President warned that he is willing to shut down the government in order to get the funding for US-Mexico wall, along with statement pertaining to termination of NAFTA treaty with Canada and Mexico.

- US economic data was disappointing on housing sector, decrease by 6.8% on orders for durable goods, housing sector sales fell in July and number of weekly unemployment assistance rose 234,000 less than expectation of 238,000.

- Fed Chair Janet Yellen offered no insight on third rate hike for the third time, as market was expecting a third hike.

- The S. dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, fell to 92.64.

- USD decline has supported all the major currencies specially Euro and GBP.

- Euro/USD remained in the range of 1.1812-1.1880, and closed at 1.1880 on Friday before the speech by ECB President Mario Draghi.

- Euro further gained strength after ECB President statement on global economy firming up and trading at 1.1924 at the time of writing this report.

- GBP/USD closed at 1.2885; primarily on weaker USD.

- UK data along with Bank of England rate hike uncertainty.

- USD/JPY fell to 109.25314 on Friday as weaker USD has given support to Japanese Yen.

- AUD/USD closed at 0.79286, stronger against USD on Friday due to weaker USD, however Reserve Bank of Australia has been watching the market closely as they don’t want excessive strength on AUD.

- Chinese Yuan increased and closed at 6.65029 on Friday.

Weather

- UK & Belgium remained around 19-28oC and expected to hot around 28oC, however cooled down to low 20s by the end of the week.

- Netherland weather remained between 20-25oC, and expected to be warmer before cooling down on Friday to 20o

- France remained warm this week with temperature around 25oC, and expected to be warmer next week around 28-32o

- Hot weather in Spain & Portugal with temperature around 30-37oC and expected to be cooler next week around 25o

- Temperature in Argentina remained around 16-12oC, and expected to be the same for the next week.

- Brazil remained hot with temperature around 30oC, and expected to remain around the same range next week.

- Mexico is getting warm with temperature around 22-26oC and expected to remain same next week.

- Middle East region summer season in full swing with Egypt around 35oC, Kuwait and Dubai around 45-50oC, will relatively less warmer but still in peak summer season.

- Indian Subcontinent in in monsoon season with temperature in Pakistan and India around 30-35oC, and expected to remain same next week.

- Temperature eased a bit but still hot in North East Asia, with temperature around 34-36oC in Taiwan, 28-30oC in Korea, China 28-33oC, and Japan is around 30-35o Weather expected to remain same for Korea and Taiwan, whereas a bit easing in Japan and China.

- South East Asia already in hot weather, Thailand around 32oC, Indonesia and Malaysia around 35oC, and will remain same next week.

- USA Weather: Overall weather is remained warm, with South West, South East, Mid West and Pacific region in hot peak summer.

- US weather from 1st week of September 2017 will be cooler than normal.

LNG

- LNG prices in Asian market remained bearish through out the week for October delivery, as demand is subdued as weather eased a bit in Japan and China.

- Till September cargoes are booked and market is expecting further softening in Asian market and buyers from Korea, Japan, Taiwan and China are on the sidelines evaluating the market.

- Supply side is long with cargoes available from Australia, Russia, Angola and Nigeria.

- Market is expecting additional demand post monsoon from India after opening of Dabhol terminal.

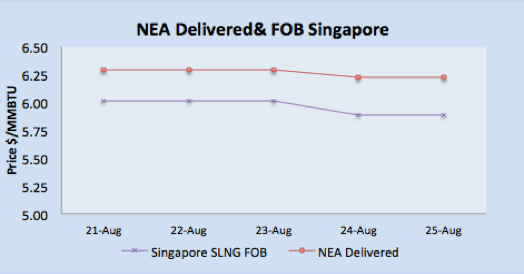

- Asian prices were heard to close on Friday with JKM $6.050/MMBTU, SLNG NEA Delivered at $6.222/MMBTU and FOB Singapore at $5.885/MMBTU.

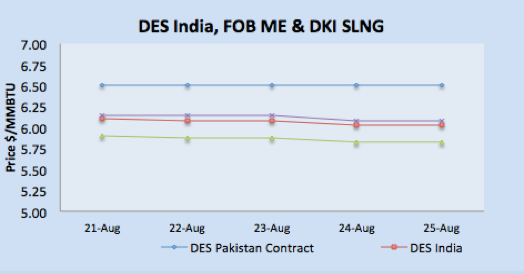

- Price level in Indian and Middle Eastern market remained in-sync with Asian prices with DES India around $6.03/MMBTU level whereas Middle Eastern at $5.80/MMBTU on FOB level.

- JKM Future curve market closed at $6.110/MMBTU for October, $6.575/MMBTU for November and $7.00/MMBTU for December, moved a bit down from last week and curve market suggesting that prices will regain in the winter season.

- Demand for imported LNG in European markets is low as weather is easing a bit and ample supply from regular imported LNG volumes along with pipeline gas from Russia and Norway.

- For UK market due to adequate supply of pipeline gas, prices seems to be 25 cents discount from NBP UK and TTF day ahead price.

- October European gas hub prices for North West Europe remain subdued and closed at Pence 44.43/Therm ($5.72/MMBTU) for NBP UK, whereas TTF closed at €16.29/MWH ($5.67/MMBTU), suggesting bearish trend for October prices in North West Europe.

- Winter gas prices curve market is bullish suggesting upward trend after October when market participant start considering November delivery cargoes.

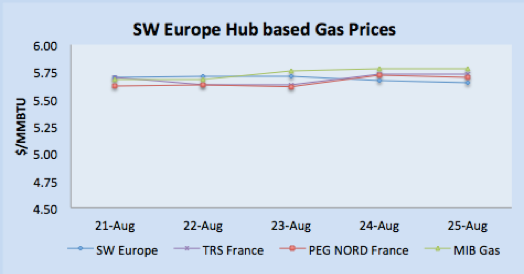

- South Western gas prices were steady during the weak as due to warm weather, and prices were around $5.70/MMBTU level.

- Price remained steady for Spain and Portugal during the week for Day Ahead market and MIBGAS closed at €16.60/MWH ($5.78/MMBTU) on Friday.

- South West Europe curve market for November closed at €17.29/MWH ($6.02/MMBTU), suggesting winter price bullish trend.

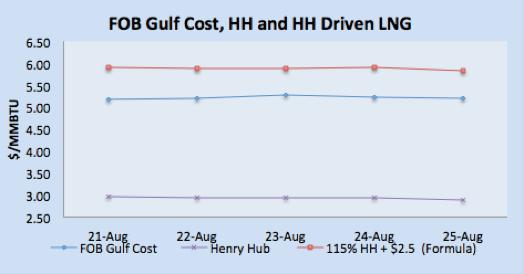

- Current Asian prices base upon October future prices converts into $4.95/MMBTU for US producers, whereas for European destination based upon TTF October price, comes around $5.15-5.20/MMBTU for US producers, so for the month of October there is an arbitrage window for US producers for European destinations.

- South Korea’s S-Oil Corp signed a long-term LNG supply contract with Malaysia’s Petronas for 15 years starting 2018 for 700,000 TPA.

- China LNG imports doubled for the month of July on Year on Year basis to 3.13 million tones and for the first seven month Chinese LNG import stands at 19 million tons, an increase by 45% from last year.

Author’s Comments

- Short term LNG prices will remain bearish for Asian and Atlantic market as there is lack of appetite from Asian market and European market are well supplied, therefore prices are expected to be bearish in the next week.

- For long term outlook, European hub curve prices are defining the direction for winter prices and will open up the arbitrage opportunity for next two month before winter season, as prices are bearish in Asian market.

- LNG Prices based upon Brent formula are less preferred choice for Asian buyers if it is compared with spot prices. Brent prices bullish trend is impacting European Hub gas prices, which may impact LNG prices in European market as one of the contributing factor.

|

|

|

|

|

|

LNG Merchant Activity

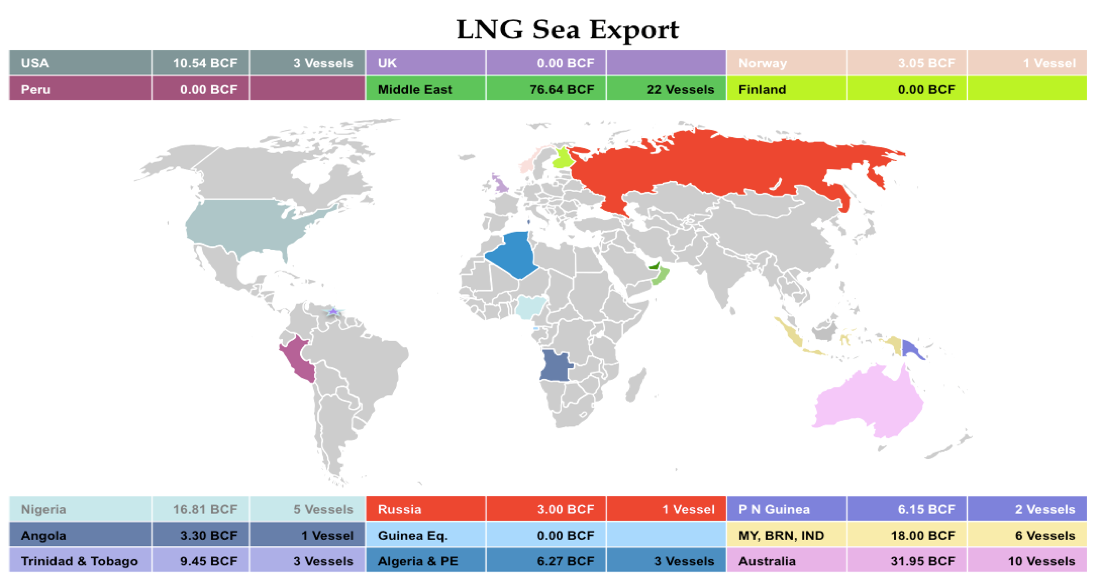

- 57 vessels carrying 3.63 million tons (185.06 BCF) loaded from various supply centres, an increase by 0.25 million tons from last week.

- Primarily increase in the quantities is from Qatar, Nigeria, Angola and Indonesia in comparison from last week, whereas this week there are fewer cargoes departed from Peru, Russia and Australia.

- 68 vessels carrying 4.80 million tons, have been dispatched from Ras Laffan, Qatar so far in the month of August, this represent 36% of total global trade on Month to date basis.

- 3 vessels left for Indian ports with 10.03 BCF and one vessel carrying 2.95 BCF for Pakistan from Qatar.

- Five vessels carrying 16.81 BCF departed from Nigerian port, two for European destination and one for India.

- Algeria loaded two vessels carrying 3.06 BCF for Italy and Spain.

- Pont Fortin, Trinidad & Tobago loaded three vessels with 9.45 BCF, two cargoes destined for South Americas and one for European destination.

- Two vessels loaded from Brunei with load of 6.24 BCF.

- Ten vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China and Korea carrying 31.95 BCF.

- One cargoes left for Denmark with 3.05 BCF from Norway.

- Middle Eastern terminal at Qalhat (Oman) loaded one vessel carrying 3.00 BCF for Japan.

| Departure Date | Vessel Name | Capacity(CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 21-Aug-17 | GASLOG SKAGEN | 154,948 | Bonny, Nigeria | Atlantic Basin | 3.20 | |

| 23-Aug-17 | LNG PORT HARCOURT II | 170,000 | Bonny, Nigeria | Europe | 06-Sep-17 | 3.51 |

| 25-Aug-17 | LNG BONNY II | 177,000 | Bonny, Nigeria | India | 16-Sep-17 | 3.65 |

| 19-Aug-17 | LNG ABUJA II | 170,000 | Bonny, Nigeria | Not Known | 10-Sep-17 | 3.51 |

| 22-Aug-17 | LNG ENUGU | 142,988 | Bonny, Nigeria | Not Known | 2.95 | |

| 23-Aug-17 | WILFORCE | 155,900 | Punta Europa, Africa | Not Known | 3.22 | |

| 24-Aug-17 | GLOBAL ENERGY | 74,130 | Skikda, Algeria | France | 26-Aug-17 | 1.53 |

| 20-Aug-17 | CHEIKH EL MOKRANI | 73,990 | Skikda, Algeria | Italy | 22-Aug-17 | 1.53 |

| 24-Aug-17 | LOBITO | 154,948 | Soyo, Angola | Not Known | 02-Sep-17 | 3.20 |

| 23-Aug-17 | COOL RUNNER | 160,000 | Point Fortin, Trinidad | Atlantic Basin | 29-Aug-17 | 3.30 |

| 21-Aug-17 | BW GDF SUEZ EVERETT | 138,028 | Point Fortin, Trinidad | Puerto Rico | 24-Aug-17 | 2.85 |

| 25-Aug-17 | MARAN GAS EFESSOS | 159,800 | Point Fortin, Trinidad | USA | 09-Sep-17 | 3.30 |

| 22-Aug-17 | CASTILLO DE SANTISTEBAN | 173,673 | Sabine Pass, USA | Atlantic Basin | 11-Sep-17 | 3.58 |

| 24-Aug-17 | MERIDIAN SPIRIT | 163,285 | Sabine Pass, USA | Colombia | 31-Aug-17 | 3.37 |

| 21-Aug-17 | MARAN GAS AGAMEMNON | 174,000 | Sabine Pass, USA | Indian Ocean | 17-Sep-17 | 3.59 |

| 24-Aug-17 | SERI ALAM | 145,572 | Bintulu, Malaysia | Japan | 02-Sep-17 | 3.00 |

| 20-Aug-17 | STENA CRYSTAL SKY | 173,611 | Bontang, Indonesia | China | 3.58 | |

| 24-Aug-17 | SENSHU MARU | 125,835 | Bontang, Indonesia | Not Known | 2.60 | |

| 20-Aug-17 | LNG JUPITER | 152,880 | Lese, Papua New Guinea | Japan | 30-Aug-17 | 3.15 |

| 23-Aug-17 | PACIFIC ARCADIA | 145,400 | Lese, Papua New Guinea | Japan | 02-Sep-17 | 3.00 |

| 21-Aug-17 | HYUNDAI UTOPIA | 125,182 | MIGAS LNG BATU, Indonesia | Korea | 28-Aug-17 | 2.58 |

| 20-Aug-17 | CYGNUS PASSAGE | 145,400 | Prigorodnoye, Russia | Japan | 28-Aug-17 | 3.00 |

| 20-Aug-17 | AMALI | 147,228 | Sieria Oil Terminal, Brunei | Not Known | 3.04 | |

| 23-Aug-17 | AMANI | 155,000 | Sieria Oil Terminal, Brunei | Not Known | 3.20 | |

| 20-Aug-17 | PACIFIC ENLIGHTEN | 147,800 | Dampier, Australia | Japan | 29-Aug-17 | 3.05 |

| 23-Aug-17 | ENERGY CONFIDENCE | 152,880 | Dampier, Australia | Japan | 03-Sep-17 | 3.15 |

| 25-Aug-17 | SERI ANGGUN | 145,100 | Dampier, Australia | Japan | 05-Sep-17 | 2.99 |

| 21-Aug-17 | DAPENG STAR | 147,200 | Dampier, Australia | Not Known | 28-Aug-17 | 3.04 |

| 24-Aug-17 | WOODSIDE CHANEY | 174,000 | Dampier, Australia | Pacific Basin | 24-Sep-17 | 3.59 |

| 21-Aug-17 | ALTO ACRUX | 147,978 | Darwin, Australia | Japan | 10-Sep-17 | 3.05 |

| 21-Aug-17 | TANGGUH JAYA | 154,948 | Gladstone, Australia | China | 31-Aug-17 | 3.20 |

| 25-Aug-17 | GASLOG GREECE | 174,000 | Gladstone, Australia | China | 04-Sep-17 | 3.59 |

| 21-Aug-17 | PALU LNG | 159,800 | Gladstone, Australia | Pacific Basin | 31-Aug-17 | 3.30 |

| 21-Aug-17 | METHANE RITA ANDREA | 145,000 | Gladstone, Australia | Pacific Basin | 30-Aug-17 | 2.99 |

| 22-Aug-17 | ARCTIC PRINCESS | 147,835 | Melokya, Norway | Denmark | 26-Aug-17 | 3.05 |

| 24-Aug-17 | NIZWA LNG | 145,469 | Qalhat, Oman | Japan | 08-Sep-17 | 3.00 |

| 21-Aug-17 | ENERGY ATLANTIC | 132,588 | Ras Laffan, Qatar | Argentina | 14-Sep-17 | 2.74 |

| 20-Aug-17 | HOEGH GIANT | 229,000 | Ras Laffan, Qatar | Argentina | 13-Sep-17 | 4.72 |

| 21-Aug-17 | GALICIA SPIRIT | 137,814 | Ras Laffan, Qatar | Egypt | 29-Aug-17 | 2.84 |

| 23-Aug-17 | BU SAMRA | 260,928 | Ras Laffan, Qatar | Far East | 09-Sep-17 | 5.38 |

| 25-Aug-17 | MARAN GAS ALEXANDRIA | 164,000 | Ras Laffan, Qatar | Gibraltar | 3.38 | |

| 19-Aug-17 | DISHA | 136,026 | Ras Laffan, Qatar | India | 23-Aug-17 | 2.81 |

| 23-Aug-17 | RAAHI | 138,077 | Ras Laffan, Qatar | India | 27-Aug-17 | 2.85 |

| 25-Aug-17 | AL SAHLA | 211,842 | Ras Laffan, Qatar | India | 29-Aug-17 | 4.37 |

| 25-Aug-17 | ZEKREET | 178,200 | Ras Laffan, Qatar | Japan | 10-Sep-17 | 3.68 |

| 22-Aug-17 | HL RAS LAFFAN | 185,000 | Ras Laffan, Qatar | Korea | 06-Sep-17 | 3.82 |

| 20-Aug-17 | AL AREESH | 148,786 | Ras Laffan, Qatar | Mediterian | 28-Aug-17 | 3.07 |

| 24-Aug-17 | AL DAAYEN | 148,853 | Ras Laffan, Qatar | Mediterian | 01-Sep-17 | 3.07 |

| 21-Aug-17 | GALICIA SPIRIT | 137,814 | Ras Laffan, Qatar | Not Known | 29-Aug-17 | 2.84 |

| 22-Aug-17 | AL GHARIYA | 205,941 | Ras Laffan, Qatar | Not Known | 4.25 | |

| 25-Aug-17 | AL JASRA | 135,855 | Ras Laffan, Qatar | Not Known | 2.80 | |

| 25-Aug-17 | MARAN GAS MYSTRAS | 159,800 | Ras Laffan, Qatar | Not Known | 1-Sep-17 | 3.30 |

| 24-Aug-17 | AL KHATTIYA | 205,993 | Ras Laffan, Qatar | Not Known | 04-Sep-17 | 4.25 |

| 21-Aug-17 | MARAN GAS ASCLEPIUS | 142,906 | Ras Laffan, Qatar | Pakistan | 24-Aug-17 | 2.95 |

| 22-Aug-17 | SK AUDACE | 234,000 | Ras Laffan, Qatar | Portugal | 20-Sep-17 | 4.83 |

| 22-Aug-17 | DUKHAN | 137,622 | Ras Laffan, Qatar | Spain | 04-Sep-17 | 2.84 |

| 21-Aug-17 | FUWAIRIT | 138,262 | Ras Laffan, Qatar | Taiwan | 2.85 |