Market Analysis

Crude Oil

- Crude oil resumed the bullish tone on Monday and remained strong till Wednesday and then corrected a bit, and overall prices remained stable, however, long term outlook still is very fragile.

- Oil price drivers this week have been EIA inventory number, USD strength, Rig data and OPEC oil production horizon.

- Brent price closed at $52.42, slight correction from last Friday closing price of $52.52/BBL, whereas WTI closed at $49.58 in comparison with last Friday price of $49.71/BBL.

- EIA Weekly report reported a draw of 1.53 million barrels with stock at 481.9 million barrel on 28th July 2017; with market expectations were of 2.8 million barrels draw.

- Gasoline inventories at 227.7 million barrel reported on 28th July 2017, recorded a draw of 2.5 million barrel as compared to last week draw of 1 million barrels.

- USD strength also underpinned crude price as USD has been performing against all the currencies.

- Recent news on OPEC may not be complying with production targets, this is a major point to be discussed during OPEC next meeting in Abu Dhabi, focusing on boosting compliance on production cut, which will set the price tone for next week.

- Baker Hughes rig count reported a decrease of 1 oil rig, with total standing at 765, whereas gas rig increase by 3 and now at 189, with a total number of rigs at 954.

- The slowing in the increase of rigs numbers has generated a speculative expectation of oil rigs has peaked out, this phenomenon is needed to be monitored closely in coming days.

- In my opinion, OPEC Production cut compliance along with US rig numbers needs to be monitored closely in coming days, as these two parameters will decide the long term crude price.

Natural Gas

- Henry Hub prices closed at $2.77/MMBTU, down by 5.81% from last week.

- Henry Hub bearish tone is attributed to weather forecast along with supply demand situation.

- Weather is expected to be cooler than normal throughout the USA except for Mid West and Pacific.

- According to EIA, US dry natural gas production rose to 74.29 BCFD in May 2017, and this a 10 month high production number, whereas monthly US natural gas consumption has fallen by 0.92 BCFD and recorded at 62.6 BCFD in May 2017.

- S. natural gas stocks increased by 17 BCF for the week ending July 21st versus market expectation of 24 BCF increase, due to mild spring and summer temperatures in US.

- Working gas in storage was 3,010 BCF as of Friday, July 28th 2017, an increase of 20 BCF from the previous week. Stocks were 279 BCF less than last year at this time and 87 BCF above the five-year average. At 3,010 BCF, total working gas is within the five-year historical range.

- NBP UK remained volatile through out the week due to outages, inflow of LNG and gas along with crude oil prices.

- During the week, the NBP system was short on occasions primarily due to maintenance at Vesterled, Bacton Seal terminal and Kollsnes outage, which pushed the prices up.

- However higher Norwegian and LNG supply kept the price in control, as LNG vessel Al-Khuwair unloaded on 3rd August and another vessel is expected to berthed on 7th August 2017.

- NBP UK day ahead prices closed 38.4380 Pence/Therm (equivalent $$5.02/MMBTU) on Friday.

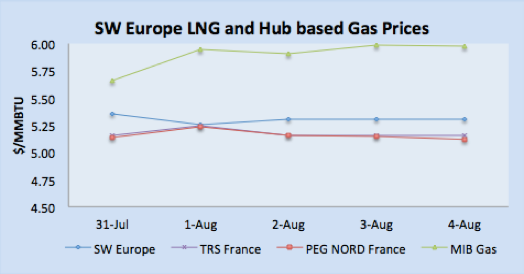

- Dutch and French gas prices remained weak as the weather is expected to be a bit cooler in the coming week along with increased gas inflows and LNG vessels arrivals.

- Russian inflows have increased along with Norwegian gas flow in the continental gas system.

- 13 LNG cargoes expected to unload in France throughout August has boosted supply outlook.

- TTF closed at €14.97/MWH (equivalent of $5.17/MMBTU) and PEG Nord France closed at €14.81/MWH ($5.12/MMBTU) on Friday.

Currency

- USD gained strength on Friday based on positive economic news, originating from job creation data and tax reforms.

- The U.S. economy created 209,000 jobs in July, handily beating the consensus estimate for the creation of 183,000 jobs.

- National Economic Council Director was quoted that US administration is working on a tax plan, which will bring corporate profits back to US.

- The S. DXY dollar index, which measures the greenback’s strength against a trade-weighted basket of six major currencies, rose to 93.50 on Friday in comparison with last Friday level of 93.34.

- The rise in the dollar weighed heavily on sterling and euro, as both currencies gave back recent gains against the greenback.

- GBP/USD fell by 0.76% to $1.3039, a day after the Bank of England left interest rates unchanged.

- GBP dropped more than 200 pips from Thursday on BOE keeping interest at a record low and cutting its forecast for growth and wages.

- EUR/USD lost 0.97% to $1.1754 while EUR/GBP fell to 0.9017, down 0.19%. The bearish tone of Euro is primarily on USD strength.

Weather

- UK, Belgium, and Netherland remained around 22oC and expected to be less than 22oC due to cloud cover and showers.

- France remained warm this week with the temperature around 28oC, however, expected to be around 24oC due to expected showers and cloud cover in the coming week.

- Hot weather in Spain & Portugal with the temperature around 28-30oC and expected to remain the same next week.

- Temperature in Argentina remained around 15oC, and expected to be cold around 15oC in the coming week.

- Brazil remained hot with the temperature around 25-30oC, and expected to remain hot next week.

- Mexico is getting warm with the temperature around 225-30oC and expected to remain warm next week.

- Middle East region summer season in full swing with Egypt around 40oC, Kuwait touched 50oC, and UAE temperature reached 45oC and will remain the same next week.

- Indian Subcontinent is in monsoon season with temperature in Pakistan and India around 35oC, same weather profile for next week. Weather profile doesn’t have any major impact on gas prices in India and Pakistan, as there is substantial demand supply gap.

- Temperature remained hot in North East Asia, with the temperature around 36oC in Taiwan, 35oC in Korea, China 350oC, and Japan is around 30oC, expected to be a bit warmer in the coming week.

- South East Asia already in hot weather, Thailand around 35oC, Indonesia and Malaysia ranging between 32oC, and will remain same next week.

- USA Weather: Overall weather is remained warm, with Mid West and Pacific region in hot peak summer. Next week other than Mid West and Pacific, weather is forecasted to be a bit cooler than this week

LNG

- Asian market closed on Friday with JKM at $6.0000/MMBTU, FOB Singapore $5.6030/MMBTU, SLNG DKI at $5.7320/MMBTU for September delivery.

- Bullish price trend is attributed to more than season limit hot weather in Japan, Taiwan, and Korea, which has resulted in power sector gas consumption along with abrupt production issue.

- JKM future for September is trading at $5.780/MMBTU, putting the market in backwardation, whereas October delivery is traded $6.200/MMBTU.

- Asian prices remained bullish, as there is demand emerged from South Korea and Taiwan, as KOGAS and SKE&S are seeking number of cargoes, along with Taiwan CPC, all focused o covering summer demand due to warm weather across North East Asia.

- Prices also got support as Atlantic LNG shut down its complex due to a leakage problem, one train is still down.

- India buy tender from GSPC and IOC were heard to be closed at $5.75-$5.80/MMBTU level, putting more pressure on DES level prices in the region.

- Demand for imported LNG in European markets is low, due to ample pipelined gas supply plus arrival and expected arrival of LNG vessels.

- Imported LNG offers in North West Europe were at par with NBP UK prices and around 20 cents discount to TTF. NBP UK closed at equivalent prices level of $5.02/MMBTU and TTF at $5.17/MMBTU.

- South Western gas prices remained high due to hot temperatures, and imported LNG pries were heard at equivalent of TTF plus 10 cents on $/MMBTU basis.

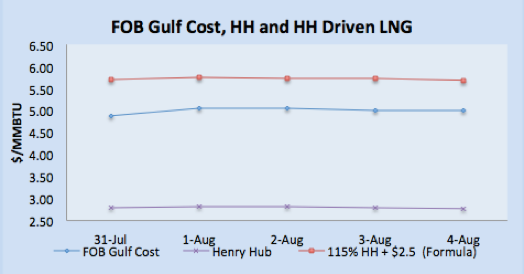

- For Iberian gas market, the target price from the buyer are TTF forward price for September, which closed at equivalent of $5.18/MMBTU on Friday. However, TTF plus 25 cents will be an acceptable price for suppliers, as it will attract US, West Africa, Norway and Trinidad cargoes.

- Based upon TTF plus 25 cents will translate into $4.98/MMBTU for US producer on FOB basis.

- Iberian gas prices still attractive for suppliers, as with re-gas cost (assumed) of $0.25-0.35/MMBTU, DES price workable to be around $5.35-$5.45/MMBTU, as Gas Hub prices closed at €17.30/MWH (equivalent of $5.98/MMBTU) on Friday.

- US producers will focus on European market beside South American market as TTF plus 20 cents are still a better market than Asian destination.

- Jordan has re-exported 560,000 m³ of LNG (about 340mn m³ of pipeline gas) to Egypt in the last four months. Meanwhile, BW Singapore, BW LNG’s first FSRU that is operating in Egypt, has reached a new milestone of 100 ship-to-ship (STS) transfers.

- Indian State run gas company GAIL India has started the work to complete Kochi-Manglore gas pipeline. This project will ensure an increase in LNG import at Petronet LNG import terminal at Kochi.

- Thailand’s Energy Policy and Planning Office allowed state-owned Electricity Generating Authority of Thailand to procure 1.5 million tons of LNG/year from next year.

- Supply side news are: Chevron’s Wheatstone LNG project start date is set to be September 2017.

- Russian’s Sakhalin project is expected to offer several cargoes for October loading, Cheniere Energy’s Sabine Pass liquefaction plant appears to have its fourth line operational as higher feedstock are flowing in. Angola and Peru are offering August and September loading cargoes.

- South Asia is emerging as a substantial LNG demand region and expected to keep on growing. India, Pakistan, and Bangladesh are stepping up and by 2025 regional demand side is expected to be around 80 MTPA.

- Pakistan is planning to have two more LNG terminal plus Bangladesh is eyeing for 17.5 MTPA by setting up two more terminal and India to grow to 50 MTPA market.

- Korea Fair Trade Commission (KFTC) is examining the illegality of the destination clauses of LNG import contracts between South Korean gas companies and exporters such as Qatar.

- Overall LNG market bullish trend is due to hot weather in Nort East Asia, which has changed the sentiments, looking at supply situation, LNG upward trend may be softening and winter procurement season will take over in 4Q 2017.

|

|

|

|

|

|

LNG Merchant Activity

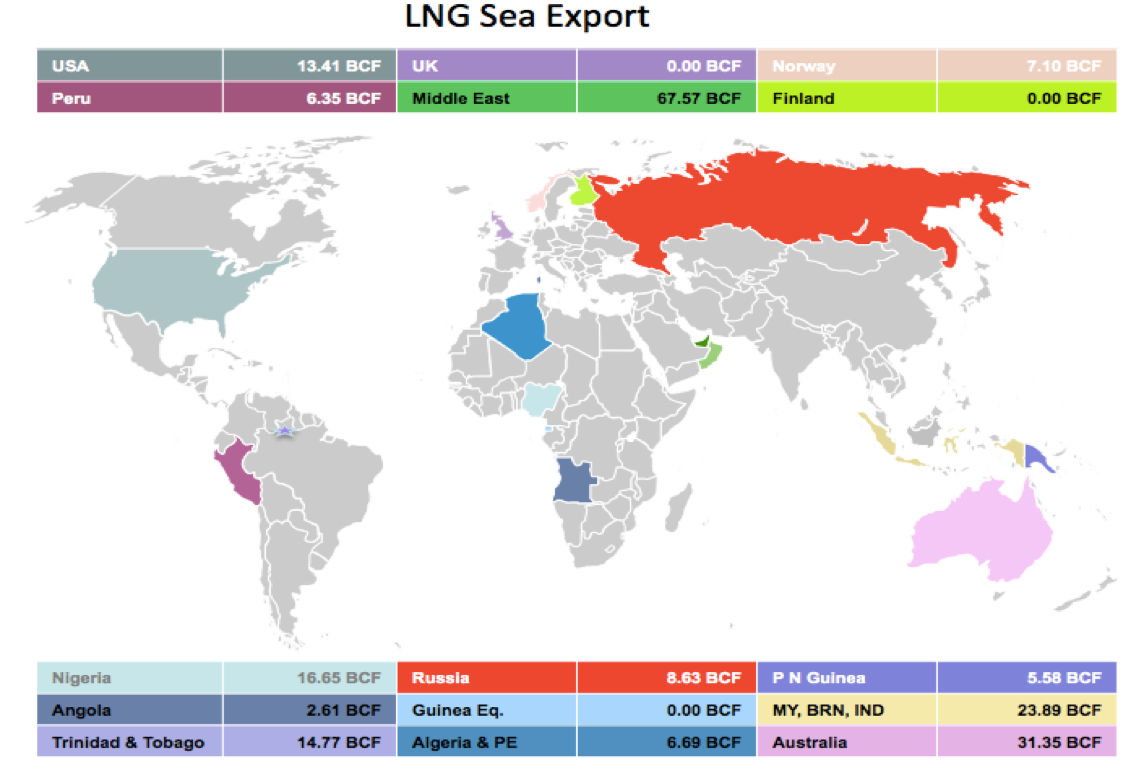

- From Sunday 16th July till 21st July 2017, 41 vessels carrying 2.61 million tons (133.23 BCF) loaded from various supply centres

- 15 vessels carrying 1.13 millions tons, have been dispatched from Ras Laffan, Qatar.

- 3 vessels left for Indian ports while one left for Port Qasim Port, Pakistan, total volume dispatched 13.25 BCF.

- Four vessels carrying 12.36 BCF departed from Nigerian port for European, South American and Asian locations

- Algeria loaded one vessel carrying 1.53 BCF for France.

- Pont Fortin, Trinidad & Tobago loaded two vessels with 5.99 BCF.

- One vessel loaded from Brunei with load of 3.20 BCF.

- 6 vessels left from Australian export terminals of Dampier, Darwin and Gladstone ports for Japan, China, Korea and Singapore carrying 17.89

- One cargo left for France with 3.05 BCF from Norway.

- Middle Eastern terminals at Das Island (UAE), Qalhat (Oman) and Ras Laffan (Qatar) loaded 17 vessels carrying 63.55 BCF for Asian and European destinations.

| Departure Date | Vessel Name | Capacity(CBM) | Loading Port | Discharge Country | ETA Discharge Port | LNG (BCF) |

| 29-Jul-17 | LA MANCHA KNUTSEN | 176,300 | Bonny, Nigeria | Egypt | 21-Aug-17 | 3.64 |

| 30-Jul-17 | WILPRIDE | 156,007 | Bonny, Nigeria | Europe | 26-Aug-17 | 3.22 |

| 3-Aug-17 | LNG LAGOS II | 177,000 | Bonny, Nigeria | Europe | 18-Aug-17 | 3.65 |

| 2-Aug-17 | SOLARIS | 154,948 | Bonny, Nigeria | Japan | 20-Aug-17 | 3.20 |

| 31-Jul-17 | LNG RIVER NIGER | 142,656 | Bonny, Nigeria | Mexico | 20-Aug-17 | 2.94 |

| 2-Aug-17 | TRIPUTRA | 30,800 | Punta Europa | Atlantic Basin | 13-Aug-17 | 0.64 |

| 3-Aug-17 | MARIB SPIRIT | 163,280 | Punta Europa | Not Known | 14-Aug-17 | 3.37 |

| 4-Aug-17 | HANJIN PYEONGTAEK | 130,366 | Skikda, Algeria | France | 03-Aug-17 | 2.69 |

| 1-Aug-17 | LNG AQUARIUS | 126,750 | Soyo, Angola | Brazil | 12-Aug-17 | 2.61 |

| 30-Jul-17 | MARAN GAS DELPHI | 159,800 | Pampa Melchorita, Peru | Not Known | 30-Jul-17 | 3.30 |

| 29-Jul-17 | PACIFIC ENLIGHTEN | 147,800 | Pampa Melchorita, Peru | Not Known | 3.05 | |

| 1-Aug-17 | NORTHWEST SHEARWATER | 125,660 | Point Fortin, Trinidad | China | 07-Aug-17 | 2.59 |

| 4-Aug-17 | ENERGY NAVIGATOR | 147,558 | Point Fortin, Trinidad | Not Known | 21-Aug-17 | 3.04 |

| 3-Aug-17 | LNG DREAM | 147,326 | Point Fortin, Trinidad | Not Known | 3.04 | |

| 2-Aug-17 | DAPENG STAR | 147200 | Point Fortin, Trinidad | Not Known | 3.04 | |

| 1-Aug-17 | ALTO ACRUX | 147,978 | Point Fortin, Trinidad | Pacific Basin | 08-Aug-17 | 3.05 |

| 2-Aug-17 | GHASHA | 137,100 | Sabine Pass, USA | 05-Aug-17 | 2.83 | |

| 2-Aug-17 | LNG FUKUROKUJU | 164,700 | Sabine Pass, USA | Egypt | 27-Aug-17 | 3.40 |

| 4-Aug-17 | CESI GLADSTONE | 174,000 | Sabine Pass, USA | Korea | 29-Aug-17 | 3.59 |

| 30-Jul-17 | GASLOG GREECE | 174,000 | Sabine Pass, USA | Mediterian | 05-Aug-17 | 3.59 |

| 4-Aug-17 | GIGIRA LAITEBO | 173,870 | Bontang, Indonesia | Indonesia | 06-Aug-17 | 3.59 |

| 1-Aug-17 | PACIFIC ARCADIA | 145,400 | Bontang, Indonesia | Japan | 10-Aug-17 | 3.00 |

| 1-Aug-17 | ARCTIC PRINCESS | 147,835 | Bontang, Indonesia | Korea | 10-Aug-17 | 3.05 |

| 29-Jul-17 | CHRISTOPHE DE MARGERIE | 237000 | Bontang, Indonesia | Not Known | 4.89 | |

| 2-Aug-17 | GEMMATA | 135,269 | Lese, Papua New Guinea | China | 13-Aug-17 | 2.79 |

| 4-Aug-17 | GALLINA | 135,269 | Lese, Papua New Guinea | Japan | 10-Aug-17 | 2.79 |

| 1-Aug-17 | CASTILLO DE VILLALBA | 135,420 | Prigorodnoye, Russia | Japan | 05-Aug-17 | 2.79 |

| 30-Jul-17 | METHANE LYDON VOLNEY | 145,000 | Prigorodnoye, Russia | Japan | 05-Aug-17 | 2.99 |

| 2-Aug-17 | BW GDF SUEZ EVERETT | 138,028 | Prigorodnoye, Russia | Not Known | 2.85 | |

| 4-Aug-17 | BRITISH SAPPHIRE | 155,000 | Sieria Oil Terminal, Brunei | Malaysia | 3.20 | |

| 29-Jul-17 | BRITISH DIAMOND | 151,883 | Sieria Oil Terminal, Brunei | Not Known | 3.13 | |

| 30-Jul-17 | OB RIVER | 146,791 | Sieria Oil Terminal, Brunei | Not Known | 28-Jul-17 | 3.03 |

| 1-Aug-17 | ENERGY PROGRESS | 144,596 | Dampier, Australia | Japan | 10-Aug-17 | 2.98 |

| 4-Aug-17 | AMUR RIVER | 146,748 | Dampier, Australia | Japan | 06-Aug-17 | 3.03 |

| 29-Jul-17 | METHANE ALISON VICTORIA | 145,000 | Dampier, Australia | Japan | 12-Aug-17 | 2.99 |

| 2-Aug-17 | MADRID SPIRIT | 135,425 | Dampier, Australia | Japan | 13-Aug-17 | 2.79 |

| 1-Aug-17 | COOL VOYAGER | 160,000 | Dampier, Australia | Japan | 17-Aug-17 | 3.30 |

| 1-Aug-17 | HYUNDAI AQUAPIA | 134,400 | Dampier, Australia | Not Known | 09-Aug-17 | 2.77 |

| 31-Jul-17 | AL KHATTIYA | 205,993 | Darwin, Australia | Japan | 10-Aug-17 | 4.25 |

| 1-Aug-17 | YENISEI RIVER | 154,880 | Gladstone, Australia | Japan | 18-Aug-17 | 3.20 |

| 2-Aug-17 | GALICIA SPIRIT | 137,814 | Gladstone, Australia | Japan | 14-Aug-17 | 2.84 |

| 31-Jul-17 | LENA RIVER | 154880 | Gladstone, Australia | Not Known | 13-Aug-17 | 3.20 |

| 2-Aug-17 | ONAIZA | 205,963 | Melokya, Norway | Spain | 08-Aug-17 | 4.25 |

| 29-Jul-17 | RAAHI | 138,077 | Melokya, Norway | Thailand | 16-Aug-17 | 2.85 |

| 2-Aug-17 | DISHA | 136,026 | Das, UAE | Japan | 17-Aug-17 | 2.81 |

| 2-Aug-17 | ASEEM | 154,948 | Qalhat, Oman | Atlantic Basin | 3.20 | |

| 1-Aug-17 | MARAN GAS ASCLEPIUS | 142,906 | Qalhat, Oman | Korea | 16-Aug-17 | 2.95 |

| 1-Aug-17 | AL SAFLIYA | 210,100 | Ras Laffan, Qatar | 4.33 | ||

| 3-Aug-17 | AL SAFLIYA | 210,100 | Ras Laffan, Qatar | Argentina | 02-Aug-17 | 4.33 |

| 30-Jul-17 | SK SUPREME | 136,320 | Ras Laffan, Qatar | Egypt | 14-Aug-17 | 2.81 |

| 3-Aug-17 | HYUNDAI COSMOPIA | 134,308 | Ras Laffan, Qatar | Egypt | 07-Aug-17 | 2.77 |

| 30-Jul-17 | AL KHARAITIYAT | 211,986 | Ras Laffan, Qatar | Far East | 4.37 | |

| 29-Jul-17 | AL MARROUNA | 149,539 | Ras Laffan, Qatar | India | 03-Aug-17 | 3.09 |

| 30-Jul-17 | AL BIDDA | 135,466 | Ras Laffan, Qatar | India | 6-Aug-17 | 2.79 |

| 3-Aug-17 | BROOG | 136,359 | Ras Laffan, Qatar | India | 05-Aug-17 | 2.81 |

| 30-Jul-17 | TAITAR NO.3 | 144,627 | Ras Laffan, Qatar | Indian Ocean | 04-Aug-17 | 2.98 |

| 31-Jul-17 | BARCELONA KNUTSEN | 173,400 | Ras Laffan, Qatar | Japan | 20-Aug-17 | 3.58 |

| 4-Aug-17 | LNG JUROJIN | 155,300 | Ras Laffan, Qatar | Japan | 20-Aug-17 | 3.20 |

| 1-Aug-17 | SM EAGLE | 202,519 | Ras Laffan, Qatar | Korea | 15-Aug-17 | 4.18 |

| 2-Aug-17 | TORBEN SPIRIT | 235,000 | Ras Laffan, Qatar | Korea | 19-Aug-17 | 4.85 |

| 3-Aug-17 | AMANI | 155,000 | Ras Laffan, Qatar | Mediterian | 3.20 | |

| 30-Jul-17 | BELANAK | 75,000 | Ras Laffan, Qatar | Mediterian | 06-Aug-17 | 1.55 |

| 4-Aug-17 | AMALI | 147,228 | Ras Laffan, Qatar | Not Known | 09-Aug-17 | 3.04 |

| 2-Aug-17 | GLOBAL ENERGY | 74,130 | Ras Laffan, Qatar | Singapore | 13-Aug-17 | 1.53 |

| 3-Aug-17 | MALANJE | 154,948 | Ras Laffan, Qatar | Taiwan | 13-Aug-17 | 3.20 |